Blunting The Wall Street Rising Wedge

Last week we saw from a chart of the steep and narrow rising wedge on the S&P500 that Wall Street is teetering on the edge of a cliff. After a weaker close the previous Thursday and Friday, Monday last week started with a BANG out of the blocks in Asia to ensure a positive close for the day. Then after two down days, Wednesday again saw an out of the blocks rally. There was quite a tussle on Wall Street on Friday that finally managed to end with only a minor loss. Is that going to be the “new normal”?

Technically, Wall Street is like that old saying about someone close to death’s door: “One foot already in the grave and the other resting on a banana peel.” The question is how long will the banana peel hold? If nature was left to its course, his foot would slip sooner or later. However, Wall Street has covert benefactors and support which have been working hard for a long time to stop and reverse sudden sell-offs. These have been hard at work the past few weeks.

The charts below are of the DJIA and S&P500 trading on Friday.

(CNN)

They display much the same progression during the day, with the DJIA a little more volatile than the S&P500. This is to be expected since it must be easier to overcome arbitrage between the underlying stocks and the index when there are only 30 of them and not 500. Which in turn implies that manipulation of the Dow30 futures offers an easier way to manipulate all of Wall Street, because of the prevalence of short term arbitrage between the two indices. This difference is also evident in the recovery late on Friday, where the rally in the DJIA managed to outperform the S&P by a wide margin.

Consideration of the market psychology of buyers and sellers in normal markets and compared with more than just recent behaviour on Wall Street has to result in the conclusion that there is an outside force that comes into play when the market tries to go into sell-off. It starts very early in Asia on the futures markets when there is some reason to anticipate a continuation of previous weakness – as bound to be the case tomorrow; again. Readers who are short of the market should consider holding only a minor position after the stock market has closed quite far in the red. Then prudent use of sell limits and stops can cover most eventualities at reduced risk.

As the usual chart later shows, the DJIA peaked and then broke back steeply below support, only to rebound, with the S&P recovering after the dip following the peak and now still moving mostly sideways, simply extending the complex top formation. So, is this going to be the new normal for the near (to medium term?) future?

The Fed and its proxies have deep pockets, both visible as could be seen from QE and covert in the other markets. In principle, this buying could continue until it owns a large share of Wall Street. But what happens when it does run out of the ability to print more money? Not because the pockets are empty, but because these have been zipped shut by one or another circumstance beyond the control of the Fed – should this happen while investors are still eager sellers, a major collapse could result.

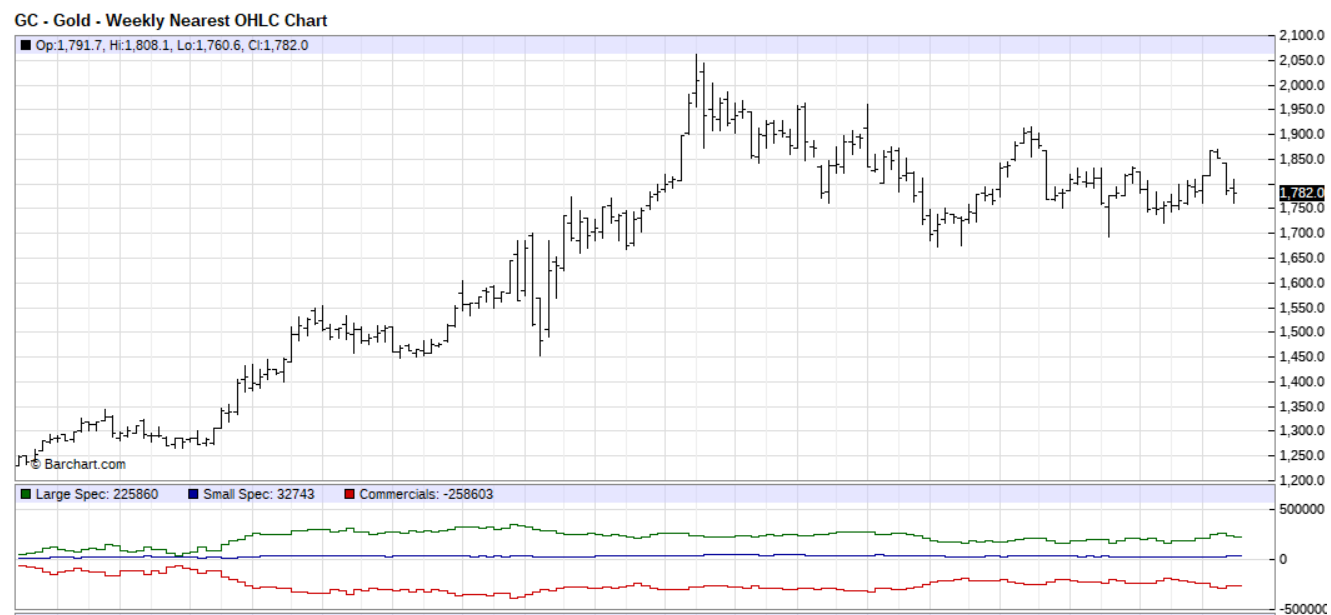

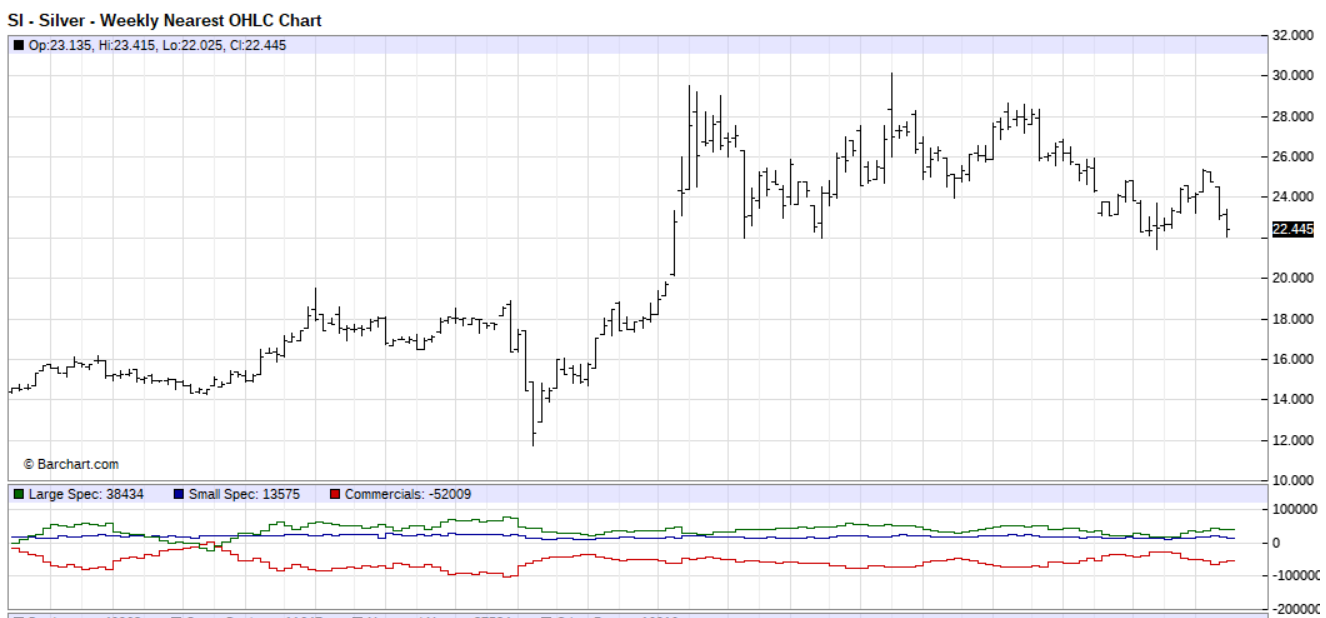

Below are two charts of the CoT for gold and silver, from Barcharts.com as these were on 29 November, last Monday. The two charts are similar in broad features, with the net gold OI of Specs and Commercials showing greater dispersion than silver, because of the larger numbers. Both charts display a narrowing of the spread between the net exposure of the Specs and the Commercials in October, followed by a widening in the gap. Late in November the gap began to narrow marginally, which preceded the steep decline in gold and silver OI during much of last week.

There has been speculation that the sudden decline in OI ought to be read as a sign that the Cartel is near a time where it will release the pressure on the metal prices.

Of course, should there be a time when they will throw in the towel, as we all believe and Stein’s Law confirms, every day that passes brings us closer to that time. The new steep decline in OI with a narrowing spread – if that continues through last week – could be Specs closing non-performing long positions and also some shorts, while the Commercials jettison their longs and reduce their shorts to reduce their overall risk.

Perhaps the overall situation with various markets poised in different directions as well as the uncertainties associated with Covid has convinced the large players to seek out a safer and more neutral position.

That could lead to good news all around!

Some information about Covid is here, here and here for interested readers.

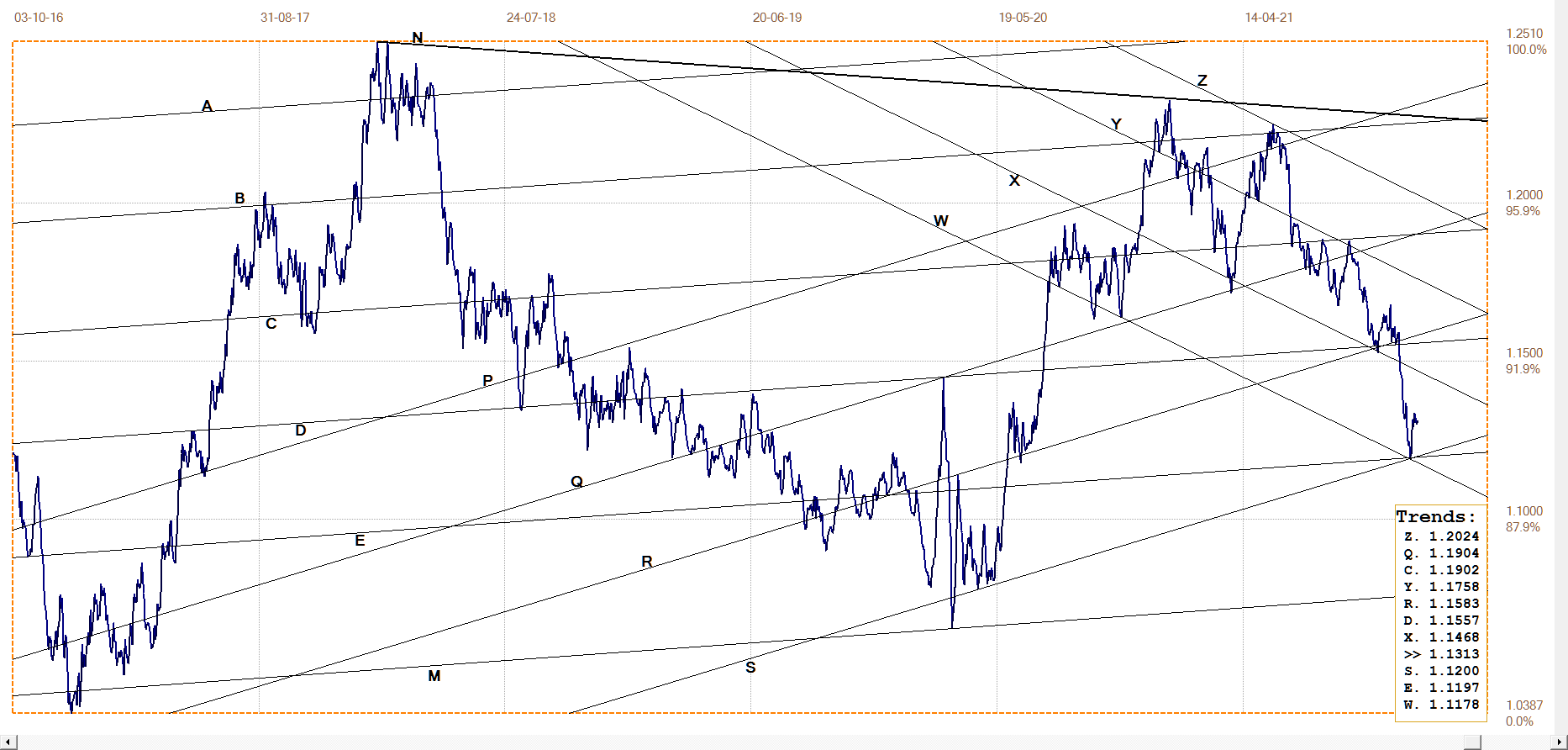

Euro–Dollar

The Euro’s steep rebound off the junction of lines W, E and S soon ran out of steam and turned sideways – or perhaps better put, with Wall Street under pressure, there was a need for a stronger dollar to help boost the market. Like gold and silver, the euro is also ‘collateral damage’ of the steady to firm dollar.

Markets are increasingly inter-connected and when there is a change in one market, a number of different other markets can be expected to react, either to compensate for the initial change or to enhance its effects. It is interesting that in this complex world the chart channel patterns remain surprisingly consistent over time.

While these ripples are limited in extent and duration, the cumulative effect does not present a problem. However, if there are to be a major dislocation in a major market – such as a sustained fall on Wall Street – the resulting avalanche of effects through different markets is bound create havoc.

Euro–dollar, last = $1.1313 (www.investing.com)

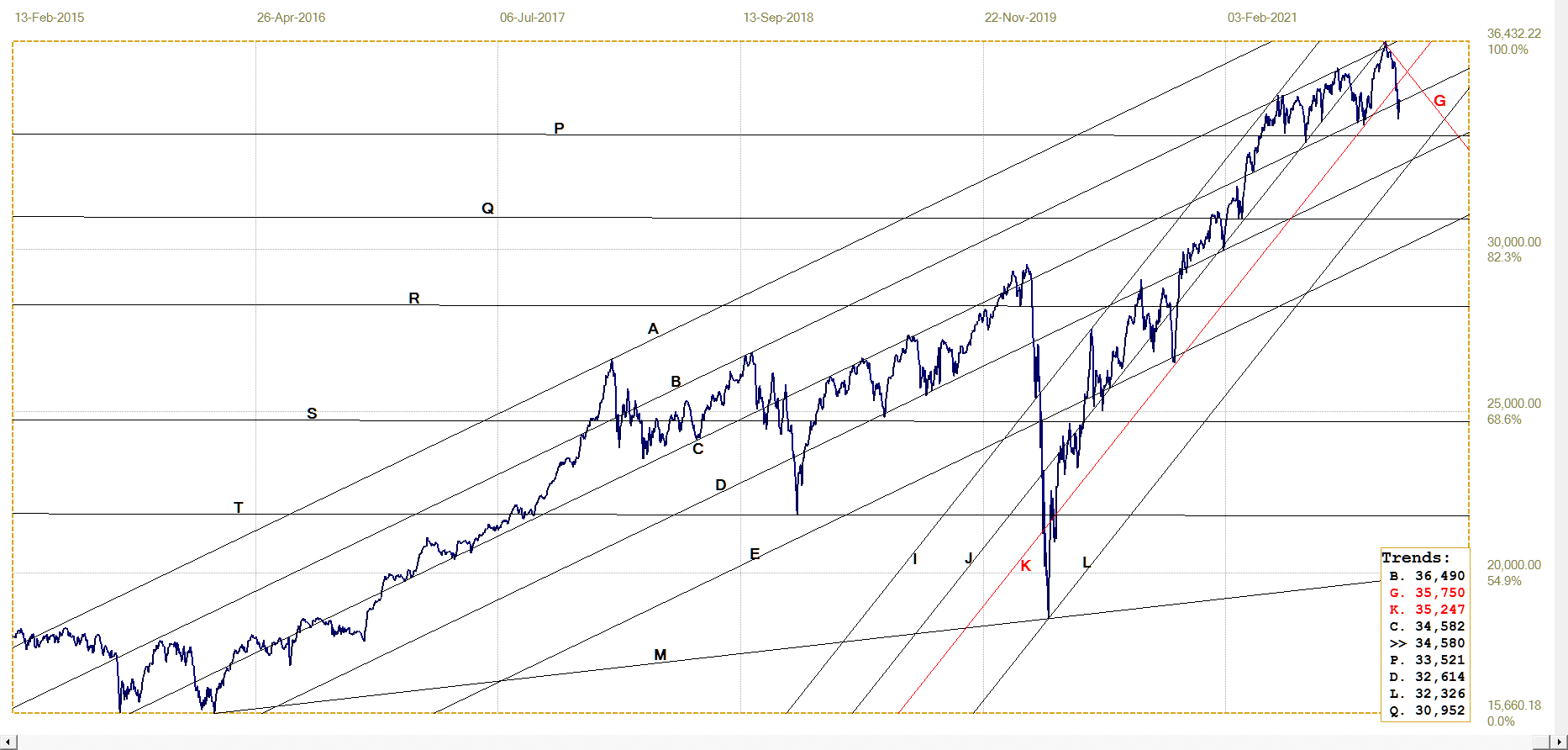

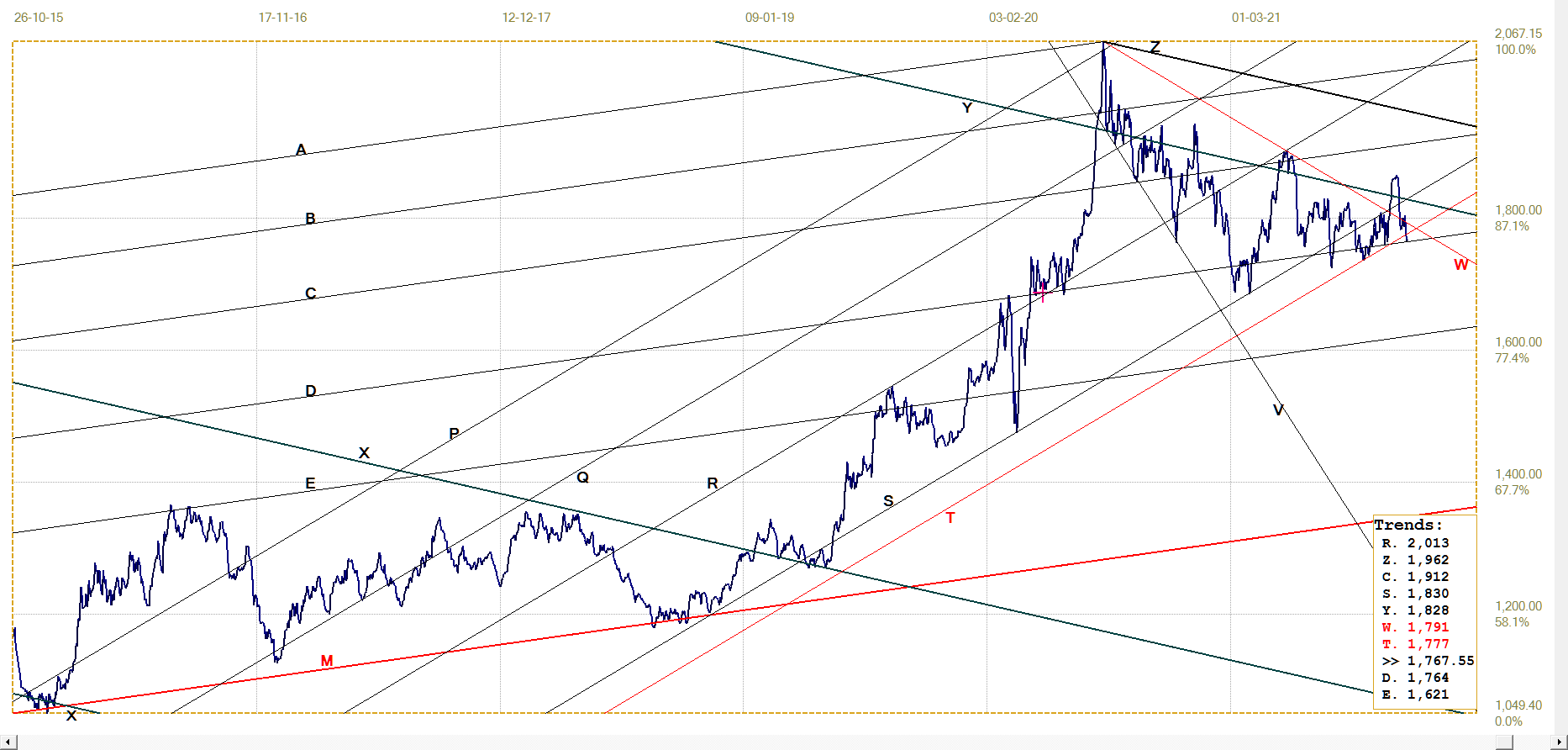

DJIA daily close

DJIA. last = 34580.08 (money.cnn.com)

During last week, there was enough weakness in equities for the DJIA to break below the support of line C, but then managed to correct back to line C and hold at the line. This could be preliminary to breaking higher and continuing mostly sideways or it could become a goodbye kiss on line C, preparatory to extending the new bear trend.

Goodbye kisses more often than not are a simple ‘touch and reverse again’ event, not a touch and hold. This implies that there could be a determined buying effort early this week to keep Wall Street on a relatively even keel, as speculated earlier. A definite reversal lower, starting with significant weakness on Monday, is likely to develop into the kind of sell-off that reaches crisis proportions before the Fed has to step in with bushels of dollars to turn the tide – for example, as in March 2020.

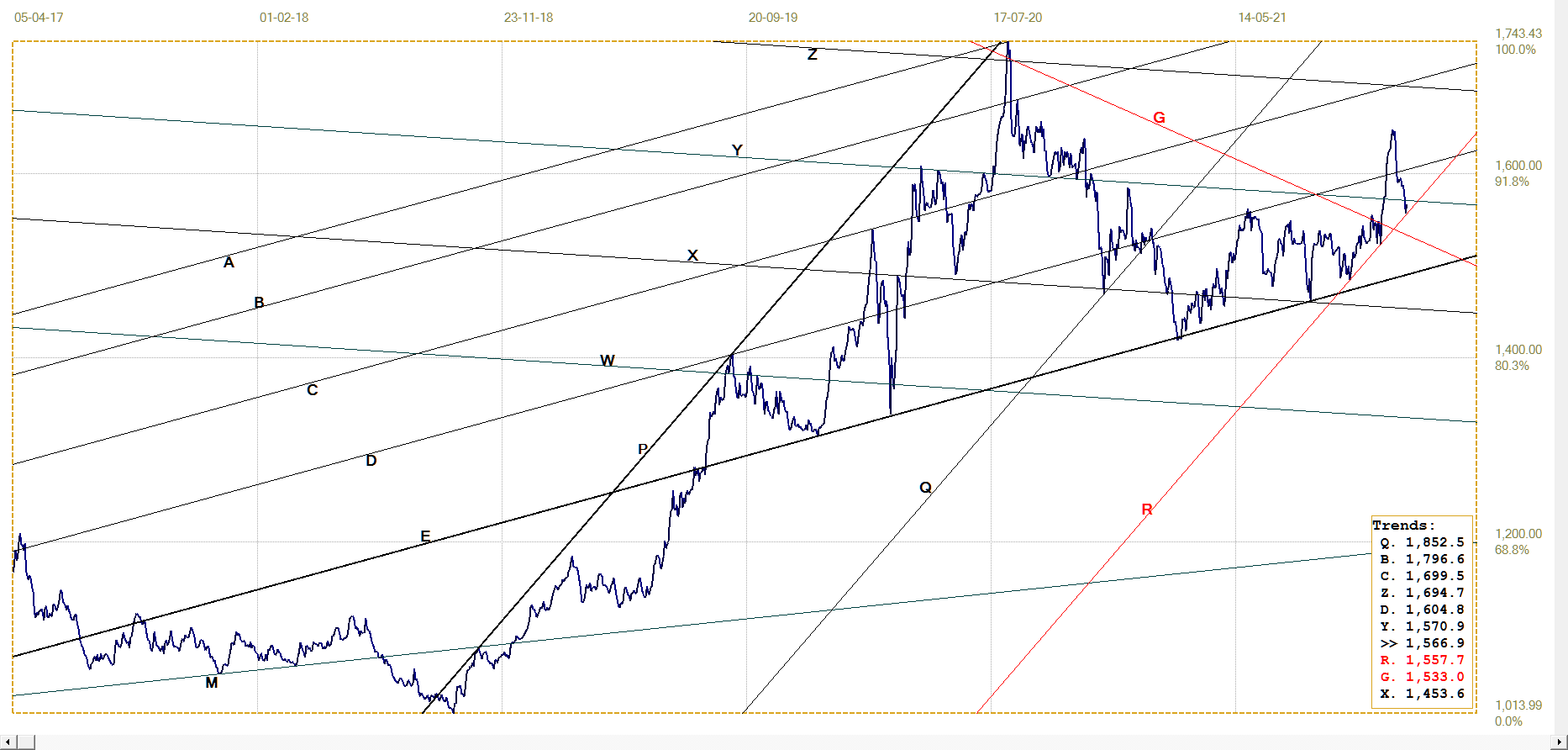

Gold London PM fix – Dollars

Gold price – London PM fix, last = $1767.55 (www.kitco.com)

On Thursday, the price of gold again tested support at line C, to hold there on Friday. It remains to be seen whether the break below bull channel ST is a warning of more weakness to come, or whether it was a temporary ‘false’ break simply to re-affirm the support along line C.

This is quite a critical moment for the future development of the price of gold, since a confirmed break below the main bull channel PQRST as well as the support along line C, would have medium to longer term sideways to bearish consequences.

With November’s month-end and NFP now history, perhaps the odds favour a rebound off line C, to resume the bull trend.

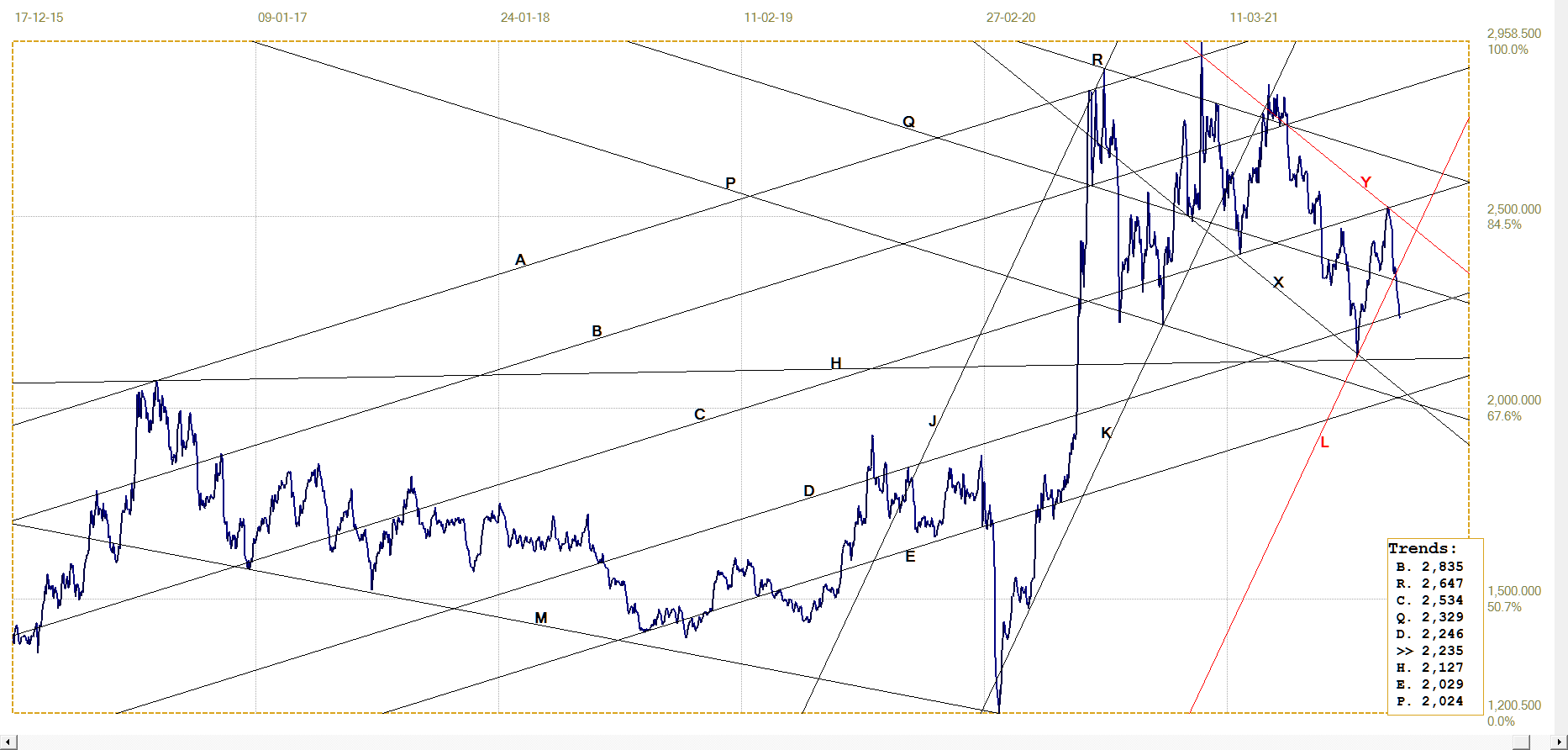

Euro–gold PM fix

The spike top on the chart of the euro price of gold initially held at line Y, but similar to the dollar price of gold the support failed to hold. The break lower ended at the bottom of bull channel PQR, placing it again in a similar position as dollar gold. Now it is up to a tussle between the strength of the dollar gold price and the euro itself to determine whether the support will hold to sustain a bullish bias for the euro price.

Too weak a dollar and/or too strong a euro will result in a bearish break from the channel, unless the dollar price of gold can increase enough to keep the euro price within the channel and, perhaps, breaking back above line Y

Euro gold price – PM fix in Euro. Last = €1566.93 (www.kitco.com)

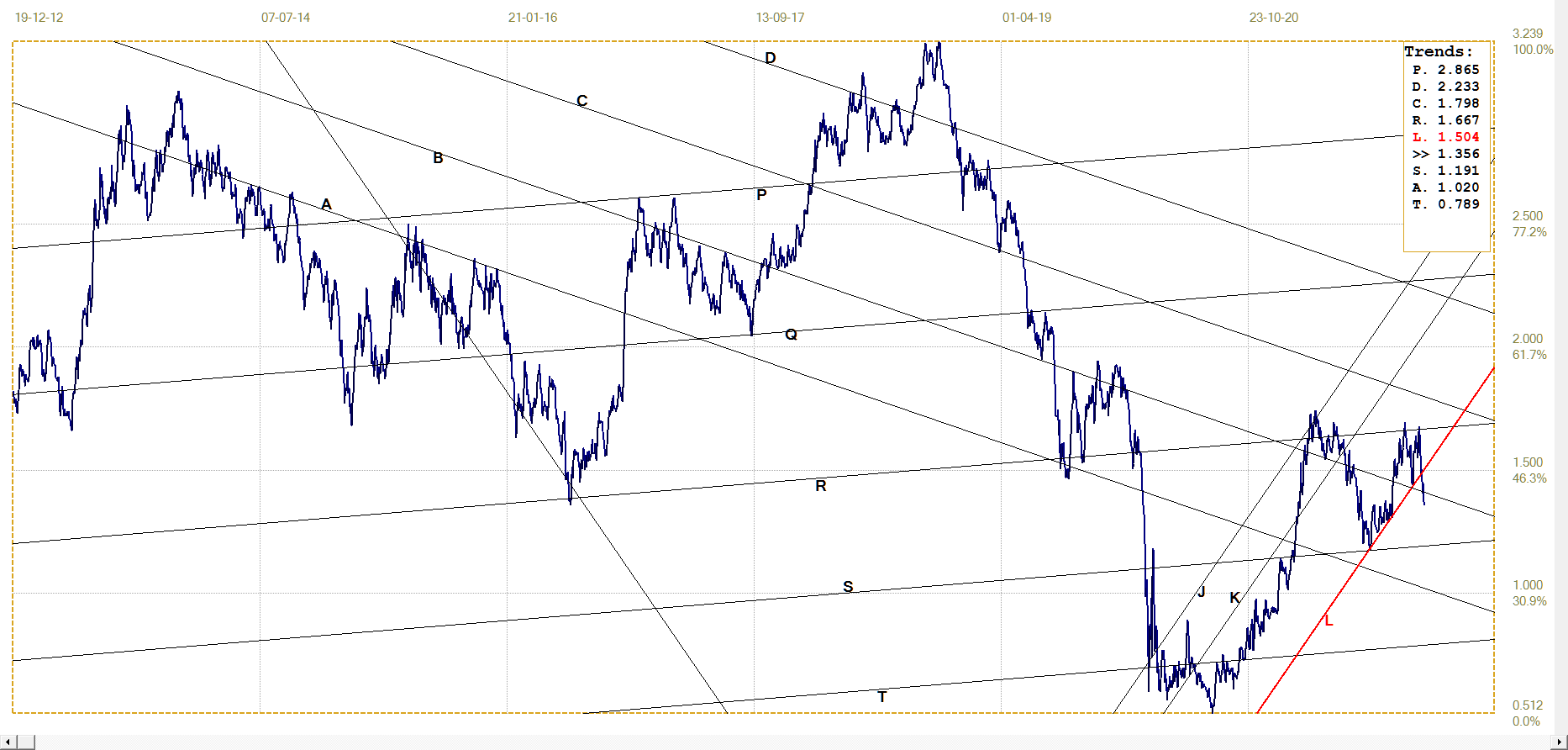

Silver Daily London Fix

The pressure of a Comex month end and the new NFP number, despite the latter being less than expected, took a toll on the price of silver more severe than what had happened to the price of gold. This difference is not anything new, but confirms that silver still presents the greater risk to the financial health of the Banks.

The recent firm support for a spike bottom reversal was at line H at $21.27, more than a dollar below Friday’s London fix, which at least is a positive trend; that is, if the support at line R continues to hold.

Silver daily London fix, last = $22.35 (www.kitco.com)

U.S. 10–year Treasury Note

10–year Treasury note, last = 1.356% (Investing.com )

Previously it was commented that, “Technically, many analysts would view the recent pattern as a flat topped triangle that could be anticipated to break higher above the flat top,” which is not what happened last week. If it had happened, with the yield increasing further, the obvious conclusion would have been the market had accepted the premise that , “inflation is not transitory.”

However, now that Powell himself has discredited that dream, it would appear that we have the classic behaviour pattern of investors switching between the usually counter-cyclical equity and bond markets – speculation that needs to be confirmed. If shown to be valid, this speculation implies that the Fed has to be stocking up on equities as they have earlier, and may still do on bonds. How long before the Fed becomes one of the larger if not largest investor on Wall Street?

*********