Caveat Emptor

The Romans are said to have had a warning, brief and to the point as Latin often is, that translates as “Buyer beware!.” It would not be farfetched to believe that the same warning, phrased much the same, existed in Sumerian and other old languages long before Latin became the lingua franca of its time. The warning might even have been brought home, too late, in the time of barter when a hunter traded a wild pig for a new spear only to have it splinter apart on his first practice cast. It has to be in the genes for a seller to bamboozle the buyer.

Leaving that subject for later, of more pressing interest is what is happening on the markets. The invasion of the Ukraine by Russia is now a week old and according to the media the Russian nose is being bloodied by the Ukrainian army. Russian losses are in high numbers and it is made clear that Putin, the new Hitler, has made a big mistake. Irrespective of what happens in the Ukraine though, the consequences of the reaction to the invasion are having a significant if often surprising impact on markets.

That the prices of oil and wheat have skyrocketed is a logical knee-jerk effect, since Russia is a substantial exporter of these two commodities and with sanctions imposed on trade with Russia by most countries aligned with the west, scarcity is ensured and inflation in Europe and the US is being given a boost. Luckily for Germany in particular, winter is almost over, since they are compelled to boycott liquid gas they have been receiving from Russia; which leaves many buildings unheated and food uncooked.

It is to be expected that the demand for gold and silver has increased because of a jump in global uncertainty the past few days. It is also no surprise that the prices of the metals are reacting like molasses on a cold morning; quite sluggish, with hardly perceptible increases. There are, however, indications from long term charts recently shown here and indications of shortages in the silver market that this could change quite soon. So far this is a possibility only discussed in the fringe media, as has been the case for decades now. For the financial MSM the cancel syndrome applies here and it is a topic not to be mentioned.

Investors who are still deeply into Wall Street also ought to heed the warning framed in this week’s title. Some might have bought with eyes wide open, knowing the equity market is being manipulated and hoping to ride on the back of it and make a profit. Many more people have their savings invested, directly or through a fund, hoping for a better return that they can get in a world of near zero interest rates. The risk that they instead will lose a substantial portion of their savings is increasing day by day; despite the efforts to prop up the market.

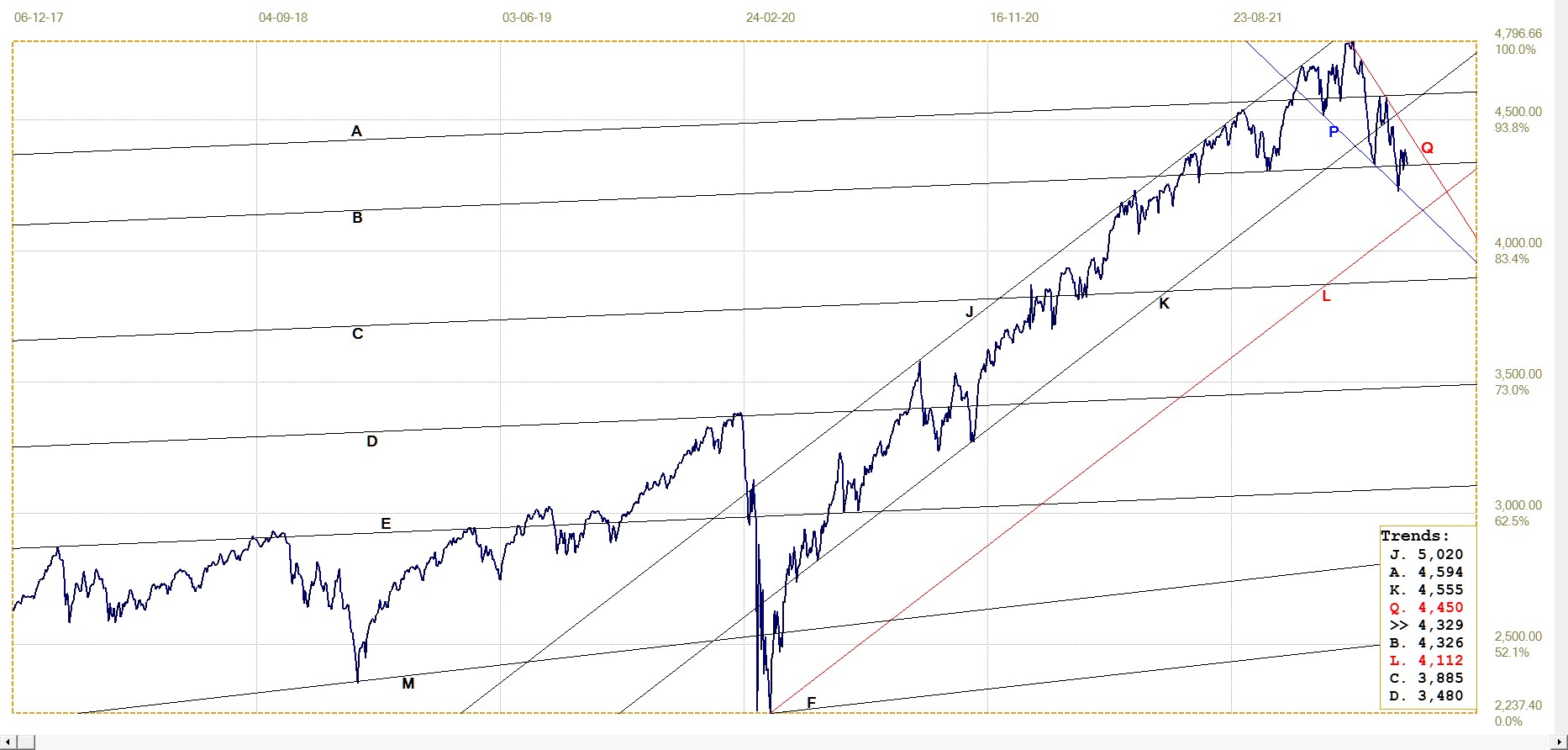

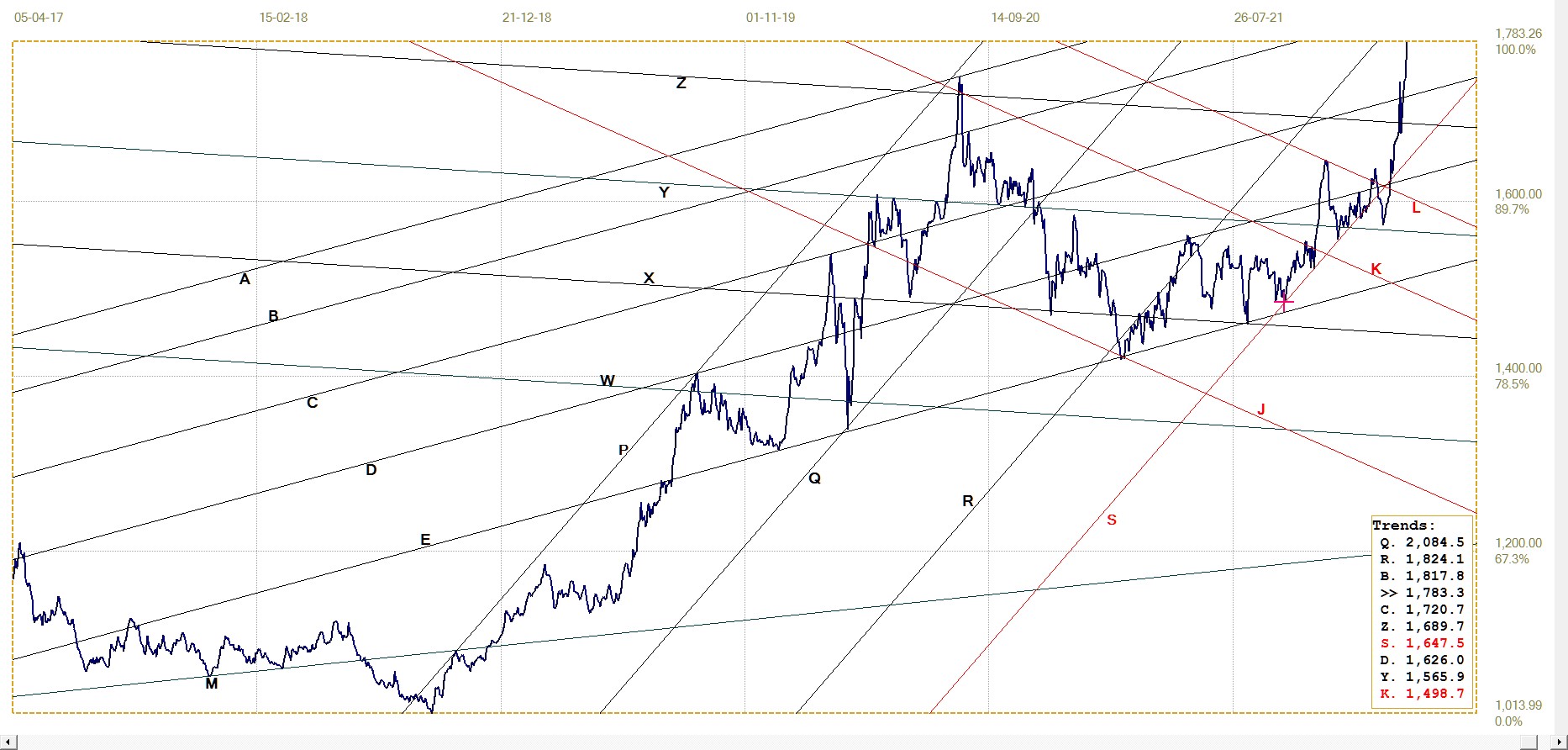

The descending wedge or pennant on the S&P500, updated below from last week’s discussion, also contains an implicit warning. While a pennant usually means that the main trend will resume when the pennant completes, a premature break from the chart formation, in the opposite direction of the main trend, can be expected to be steep and sustained. Last week, the index managed to hold above support of line B, keeping hopes that leg 5 will extend higher and break above line Q to resume and extend the bull market. If, during the next week or two, the stock market weakens for the S&P500 to break below line Q, the possibility of a premature break lower is bound to increase and so too the risk of a steep sell-off.

S&P500 index. Daily close. Last = 4328.87

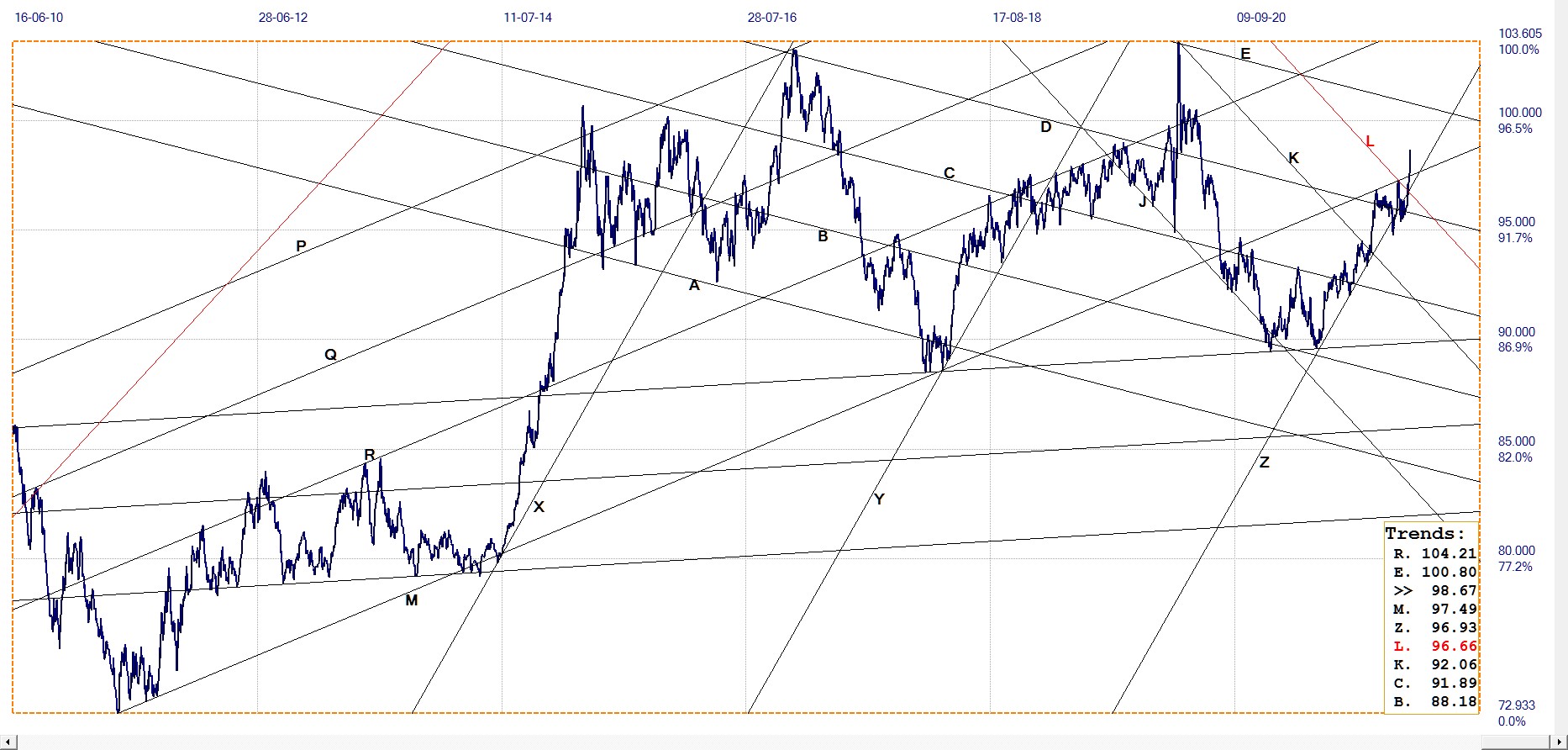

As we have seen, the dollar strengthens whenever equities get under pressure and last week almost reached a new two year high. It happened at the same time a major battle was going on to keep Wall Street stable. However, this could be coincidental, a consequence of what is happening in the Ukraine. Despite the havoc a stronger dollar is causing in currency markets, the prices of gold and silver kept on creeping ahead – a promising development for what March could bring!

Dollar index. Daily close. Last = 98.67

There is an essential commodity that most people are often unconsciously buying on a daily basis, not fully aware that they are paying indirectly for the service that also has a significant effect on their lives and their attitudes - news. Every news channel, free or by subscription, invariably claims they present truly factual news even when they admit that their presentation is interpreted according to the bias of their own political commitment.

One can also expect that Fox News and CNN will present the same facts with different interpretations. At least one can believe that what they do present does justice to the integrity of the channel’s presumed ideology and public stance. Many of us know that this is not true of some subjects, like the PM prices and also the state of the economy as reflected in Wall Street prices. However, can we accept it when government pays the MSM to present heavily slanted news in support of material that imposes a major health risk on viewers who follow the advice being promoted?

Perhaps one fall-out of the war in the Ukraine, irrespective of how it will end, is that there will be greater general awareness that ‘caveat emptor’ applies as much to ‘free’ news as when one buys a car or a TV. One should at least compare alternatives to make certain that what one gets is genuine and not a fake rip-off. By all accounts and evidence, if the message that Wall Street and Covid vaccines are safe is believed, then people’s pensions and health are being placed at risk.

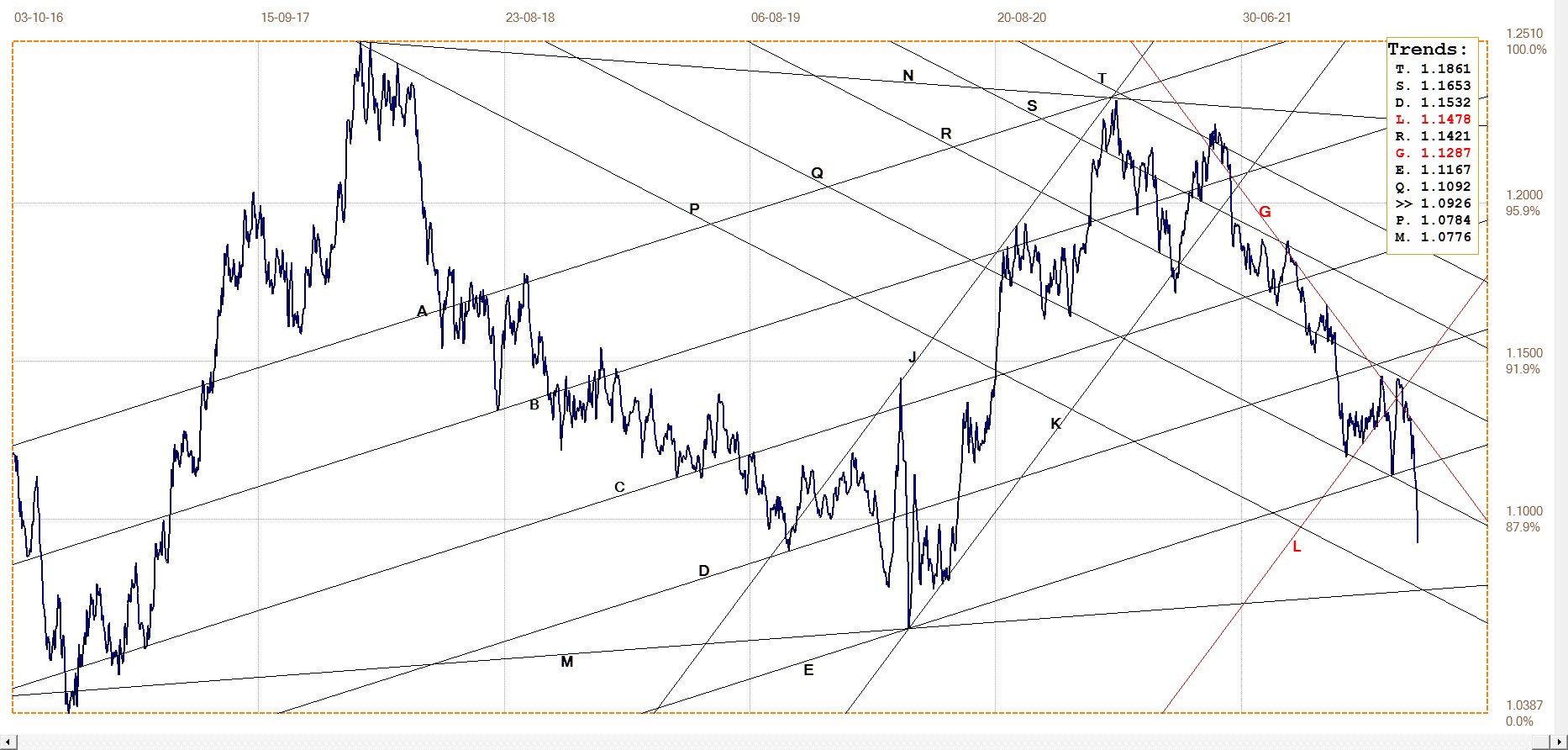

Euro–dollar. Daily close

Euro–dollar, last = $1.0926 (www.investing.com)

A suddenly plummeting euro is reacting to both a stronger dollar and a Europe that is suffering from fall-out of the invasion of the Ukraine and the sanctions that have been imposed on Russia – a kind of triple whammy, of which at least one is self-inflicted. How long the war is to last is not yet known. The Ukraine is not under full-out attack and so far civilians have suffered not as many casualties as would have been expected from a full-out invasion. Perhaps Putin has limited objectives of conquest and is more interested in effecting change in the relationship with the Ukraine and things could return to a new normal within a few weeks at most. Time will tell.

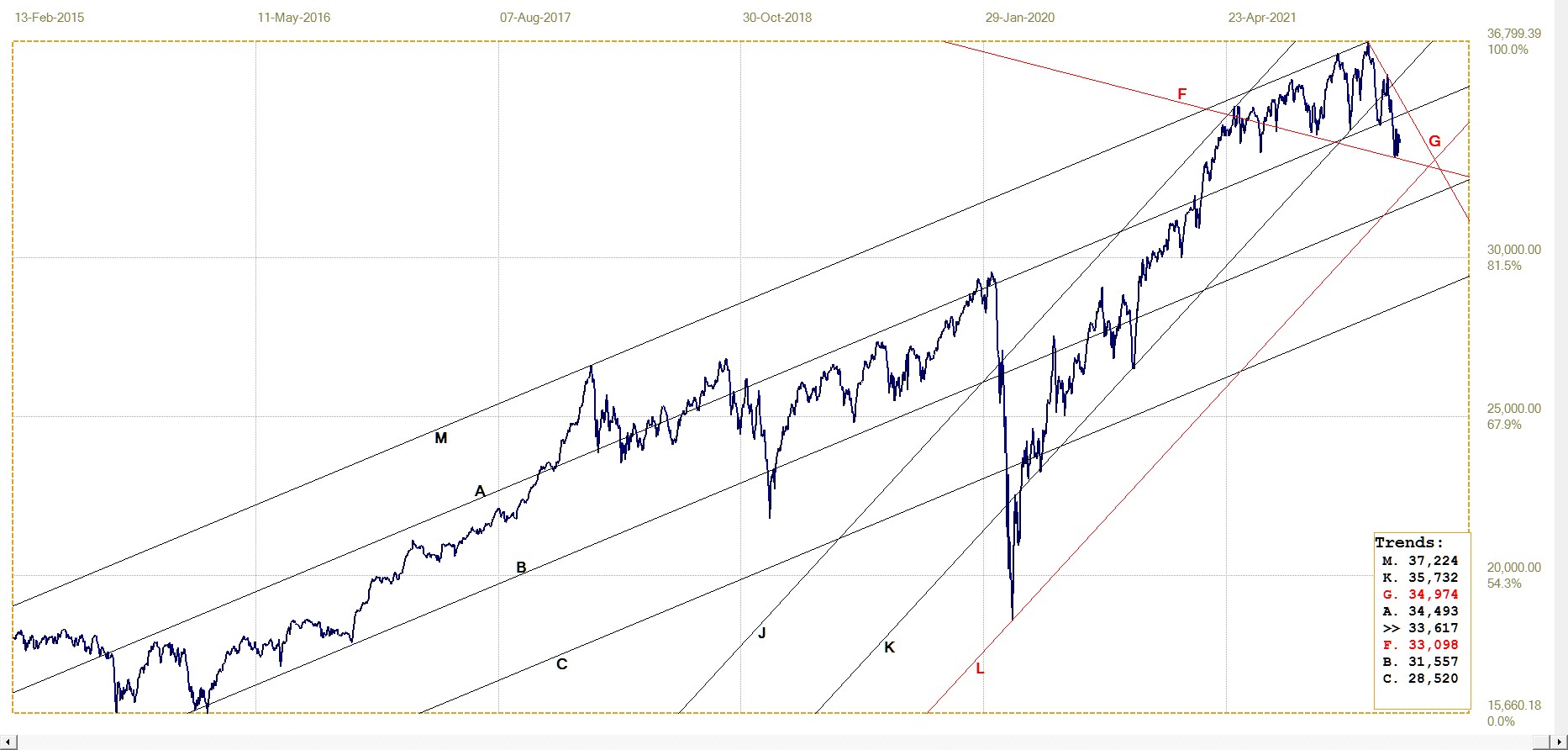

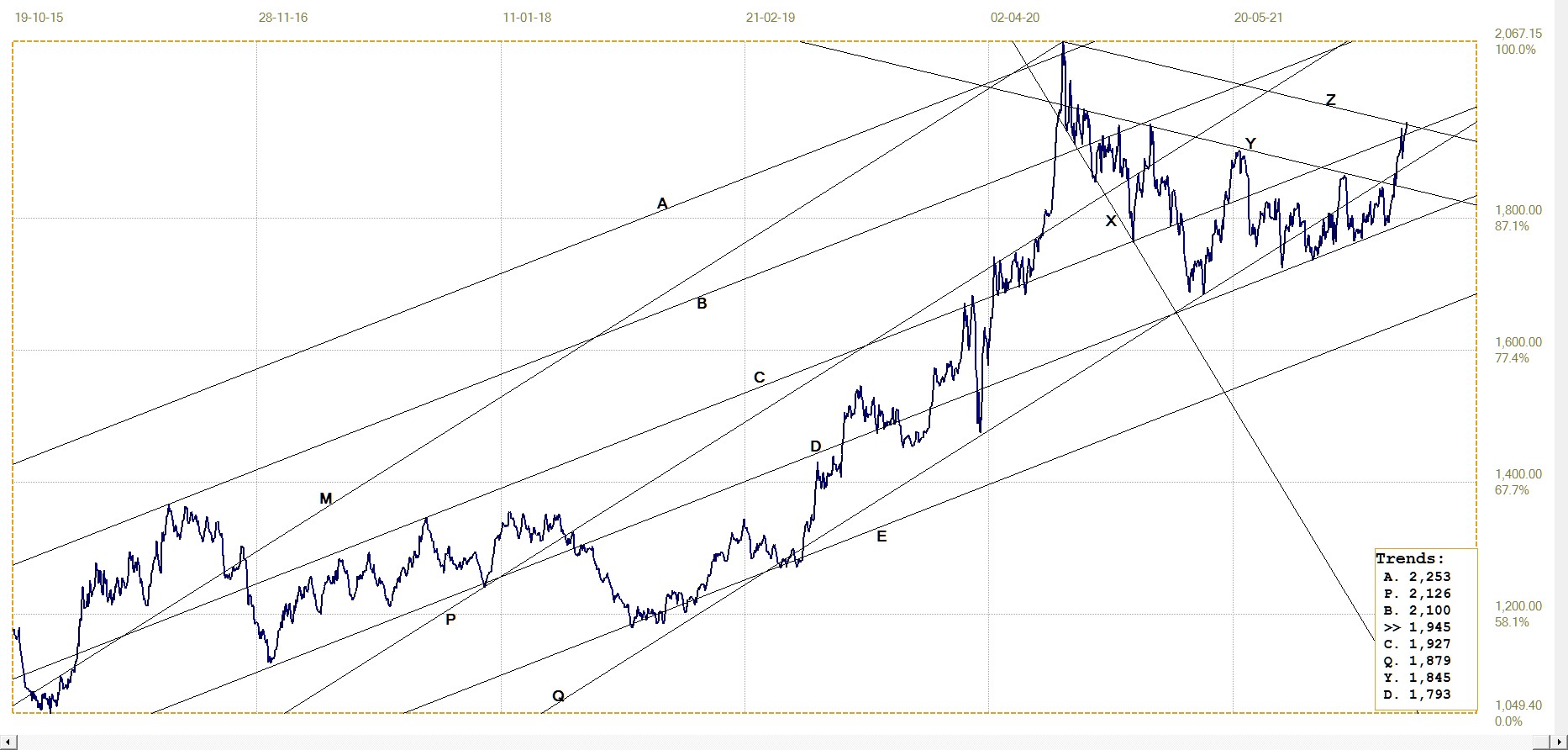

DJIA daily close

After failing to hold within bull channel MA, the DJIA has rebounded off the bottom of the developing megaphone between lines M and F to consolidate in a narrow range. A megaphone develops when strongly opposed forces in the market are engaged in a drawn out battle for supremacy. Depending on changing conditions, one is dominant for a while and then has to concede to the other and has to give way. The result is a sequence of increasingly powerful moves that last until one or the other force takes full control of the market to break from the megaphone and begin a sustained and usually steep move.

Given the increased uncertainty as a consequence of the new war and its consequences as well as a more delicate state of the US economy given the effects of the sanctions on Russia and other disruptive events, the odds still favour a break lower from the expanding pattern.

DJIA last = 33616.80 (money.cnn.com)

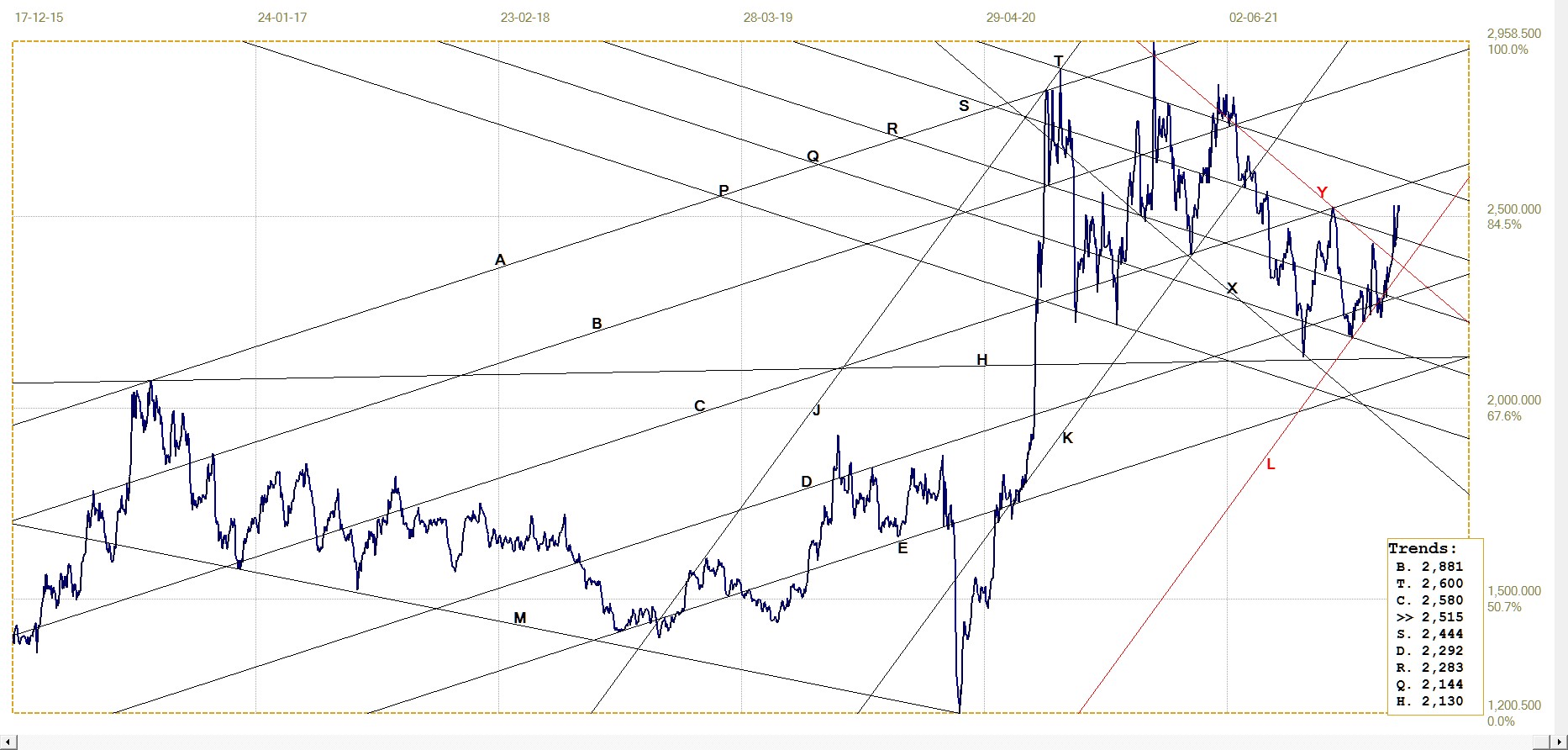

Gold London PM fix – Dollars

Gold price – London PM fix, last = $1945.30 (www.kitco.com)

The initial spike higher to above $1900 almost two weeks ago was fleeting, with the price of gold under renewed attack and soon back into the $1800s. However, as time passed and with mixed and presumably partly untrustworthy information on what is really happening on and around the field of battle, the uncertainty translated into action to seek a safe haven.

Interestingly enough, the cryptos at first hardly reacted to the new war – almost as if the crypto market was isolated in a world of its own. Yet the fact that the price of gold despite a strong dollar could resume its upward trend after the first pull-back to set a new high PM fix on Friday is a distinct and promising change of behaviour in the PM market. This week should provide some indication whether this is going to be a flash in the pan or whether it is the beginning of a definite new trend – which would have to be confirmed by what happens during the rest of March.

Euro–gold PM fix

The euro price of gold last week had the benefit of both a steady to firm price of gold and a steep loss in the value of the euro. No wonder then that the euro price spiked higher to set a new all time high – which should result in greater awareness in Europe of the advantages of owning gold.

Hopefully this will result in increasing purchases of the metal from individuals and funds or other institutions that have the freedom to invest in precious metals.

Euro gold price – PM fix in Euro. Last = €1783.26 (www.kitco.com)

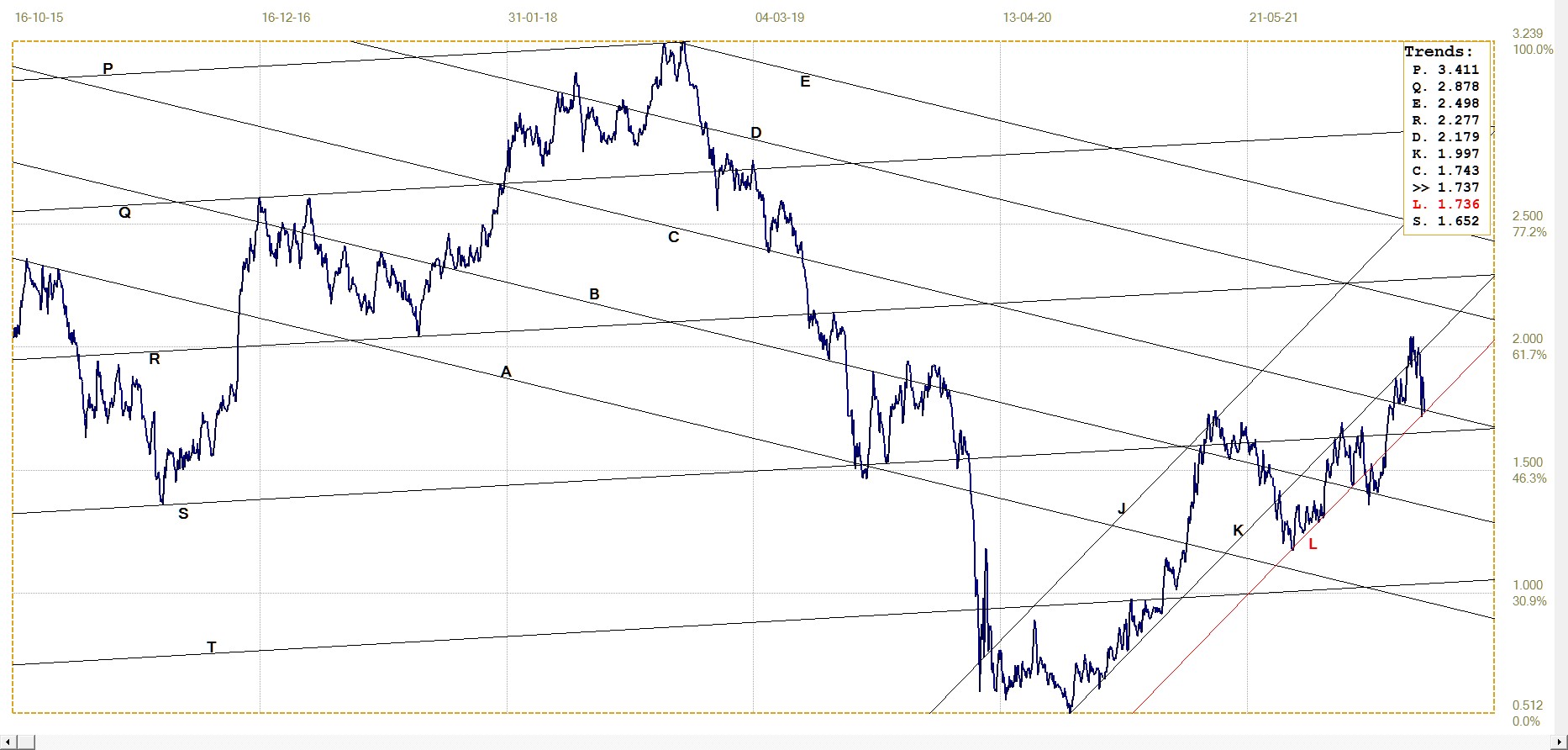

Silver Daily London Fix

Silver daily London fix, last = $25.12 (www.kitco.com)

News of the invasion had the price of silver breaking clear of its recent bear channel XY to also break into channel ST. The inevitable clamp down on the PM market after the spike higher had the price of silver briefly back below channel ST, but then the upward creep in the prices of gold and silver took hold and silver recovered into channel ST to end the week at a double top, unable to copy gold and set a new outright high.

Here too, this week is expected to give an indication of the persistence of the bullish trend that is holding to channel KL and has broken clear of the bear channel. If the trend can persist through March and reach new intermediate highs while the OI is increasing under attempts to slow down the rally, the expiration of April options and futures will become interesting – more so after the news that the settlement of PM March contracts standing for delivery at the end of February hinted at insufficient metal in the vaults.

U.S. 10–year Treasury Note

With the war in the Ukraine now going into its third week, the effects of the invasion as well as the sanctions imposed on Russia on US inflation and that of many other western countries is becoming clear. The prices of wheat and other grains that are normally exported from Russia and also from the Ukraine, which typically form a significant part of people’s diets and particularly of the poor, have risen steeply. So too the price of fuel, which affects prices throughout the economy for the worse from an inflationary perspective.

Yet the yield on the US 10-year Treasury note, which had spiked above channel KL to reach a high of 2.04% closed last week, barely closed within channel KL for the second time the past week. The bond market has become more volatile, but the main trend is to lower yields, not increasing to keep in step with current and expected increases in the prices of important commodities.

To what extent the volatility is a result of intervention to keep rates low or simply the normal effect of increased uncertainty in the market can only be guessed at. However, if the war drags out much longer without a definite conclusion being reached, surely the bond market will begin to adjust to the new reality.

10–year Treasury note, last = 1.737% (Investing.com )

West Texas Intermediate crude. Daily close

The jump of the price of crude to well above $100/bbl shows the sensitivity of the US energy market now that various interventions in the exploitation of oil have resulted in reduced production and increasing reliance on imported oil. The cushion that existed when the US for a while was a major global producer, able to export oil, is no longer available. This means that the US is exposed to the full inflationary effect of reduced supplies of oil – and for Europe of gas as well – as a consequence of the war in the Ukraine and the very strict trade and other sanctions that were imposed on Russia. The longer the war continues, the worse its effects on the economy will become – more so if the conflagration in the Ukraine should spread to drag other countries in as well, whether as active participants or simply as material supporters of either the Ukraine or Russia.

WTI crude – Daily close, last = $112.11 (www.investing.com)

©2022 daan joubert

*******