Change Is In The Air

The confrontation between the US and China is simmering in the background, now superseded in the MSM by burning US cities and the protest against Trump. On the PM front, last week saw gold and silver ending a week on a firm note for a change. The global incidence of new COVID infections was the highest it had been over the past two days and the US had two days of more than 30k fresh infections, higher than any time since May 1. The Fed has openly become the buyer of last resort. Life keeps on being interesting with fresh surprises.

The weekly stats above cover the past 12 weeks with a disturbing change in trend.

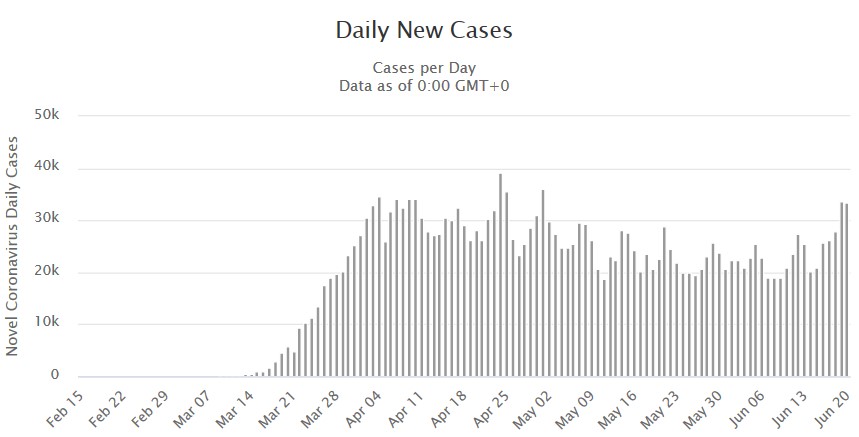

Globally and in the US the number of new infections has spiked higher, over the past two days. Globally, these were the highest numbers of the pandemic and for the US it was the highest number in seven weeks. The two Americas are making a significant contribution to the global records, with both the US and Brazil posting more than 30k new cases on Saturday. Is this going to be the new trend?

In Brazil, a country with high economic inequality, large numbers of poor people live in ‘favelas’, shanty towns, in close proximity to each other – fertile ground for the COVID virus to proliferate and spread. A number of tropical and other diseases are endemic, which contributes to a high mortality. The new spike in the US can be the result of two factors; the ‘return to work wave’ that brings people from different communities together in somewhat limited space and, where air conditioned, with reduced free air flow. Secondly, the anti-Trump protestations also result in large numbers of closely packed active people which also promotes many fresh infected.

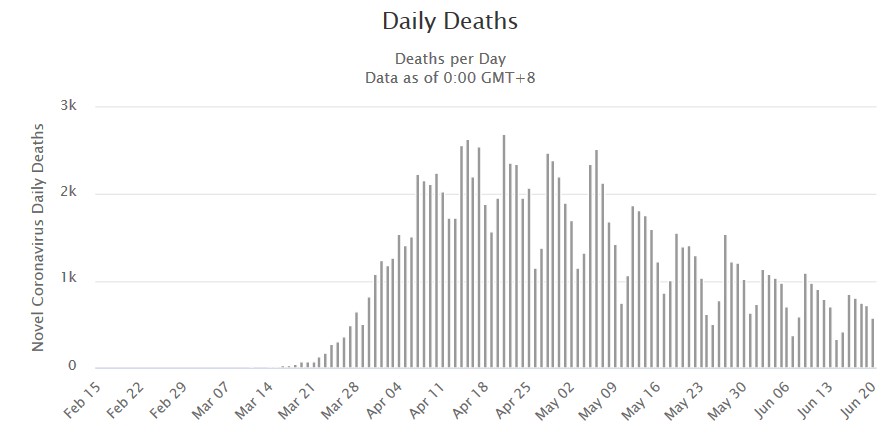

The charts above of daily new cases and deaths in the US show the new spike as well as the declining trend in mortality. It is interesting that deaths occur in a near weekly cycle; 2 to 3 days of relatively few deaths and 5 to 4 days of high mortality. The decline in mortality is likely to be due to both better treatment regimens and, probably, vulnerable people taking better care not to get infected. A reason for the cycle is not evident, but could be linked to a life style of more social contact during five weekdays and a weekend spent in more isolation. It is, whatever the cause, a surprisingly consistent cyclic pattern.

Friday was a significant day for gold. Firstly, of the three waterfall attacks, the first two hardly had any effect and then corrected, to reach new highs for the day. Only the noon attack had the price under sustained pressure by about $8, and then it contained the recovery to keep the gold price down to $1744 by the close.

(KITCO)

This is the best finish prior to a weekend since mid April, when the gold price after several attempts at last managed to break above resistance at $1700 and hold. The reason for the good performance is evident when the preliminary COMEX numbers for Friday reveal the gold OI increased by 23 773, highest by far for some time.

Clearly, something has changed. After a period of mostly low trading volumes and small changes in the OI, buyers must have flocked into the market, not in numbers as yet, but sufficiently determined to bid up the price so that the Cartel had to keep on selling to try and contain it. The silver OI also showed a good increase of 4780 new contracts which means that the buying spree was not limited to gold. As could be expected, the price of silver was again less robust than that of gold.

This week should prove whether Friday’s buying was merely a flash in the pan or whether there is something more than a rumour behind the fresh buyer interest in the metals. Of course, the prices are bound to run into the early Monday wall during Asian trading as is almost routine. If that selling either does not materialise or soon is followed by a sustained increase in the prices, this week, starting on Midwinter’s day – to bring back memories of two separate years spent at an Antarctic research base – could become more interesting for the metal buls; to be a welcome change.

WWII is long ago history, but it is a period I have long found interesting. Something that I came across recently is an account of the war in China after the Japanese invasion during the 1930s. The Battle of China begins with the horrifying atrocities of the taking of Nanking, the almost first 30 minutes perhaps better to be skipped. However, as Sun Tzu in his popular “The Art of War” emphasizes, one should know one’s opponent very well indeed in order to prevail. Given the Trade War of the past year and more, this 1944 propaganda video – after the first third – provides a picture of how the Chinese reacted to the invasion and blunted the Japanese plan of establishing an industrialist Japanese state based on a hard working population of slave labour. More than a lifetime ago for most of us, but the story it tells might still be relevant for today.

Wishing readers to be safe and remain so in this strange new world.

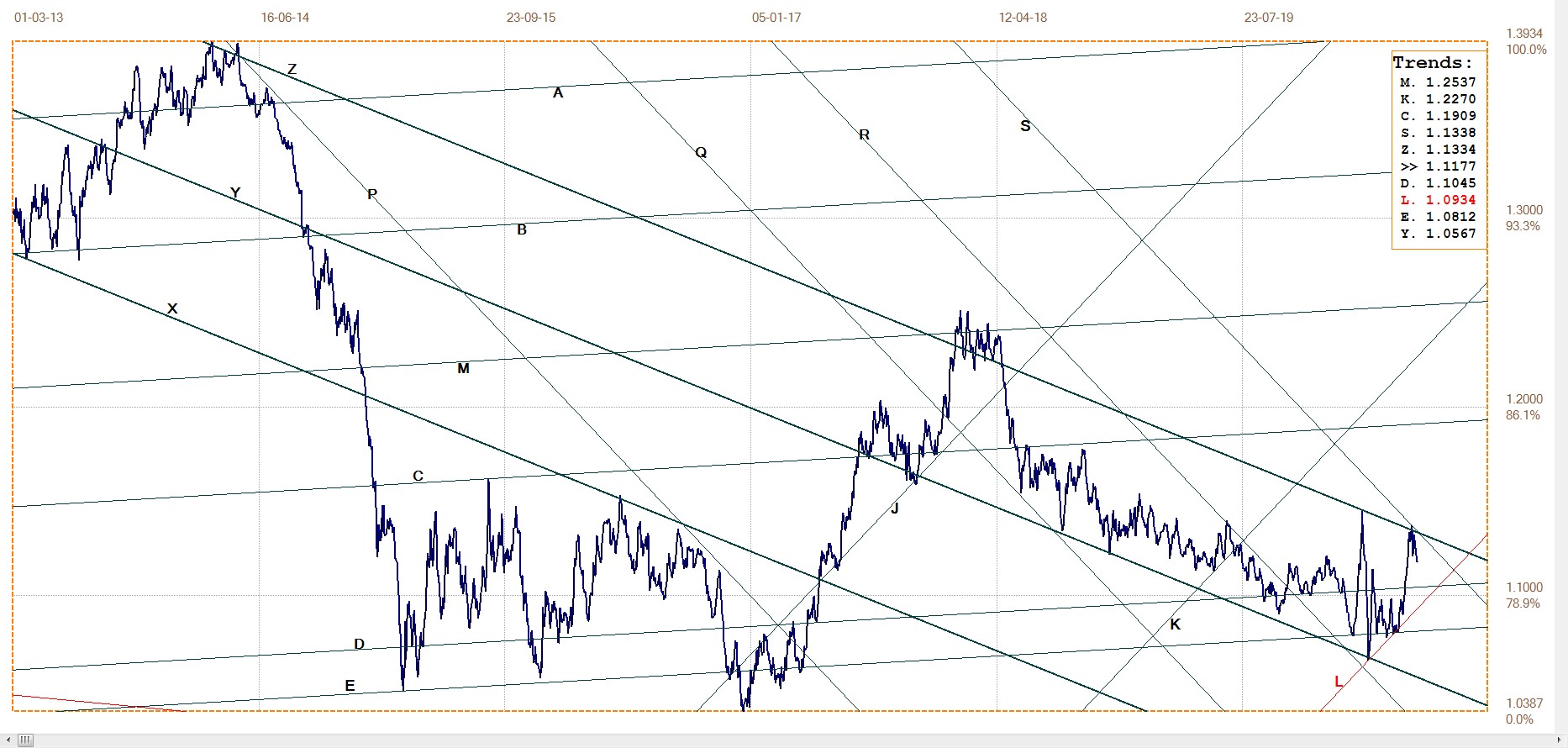

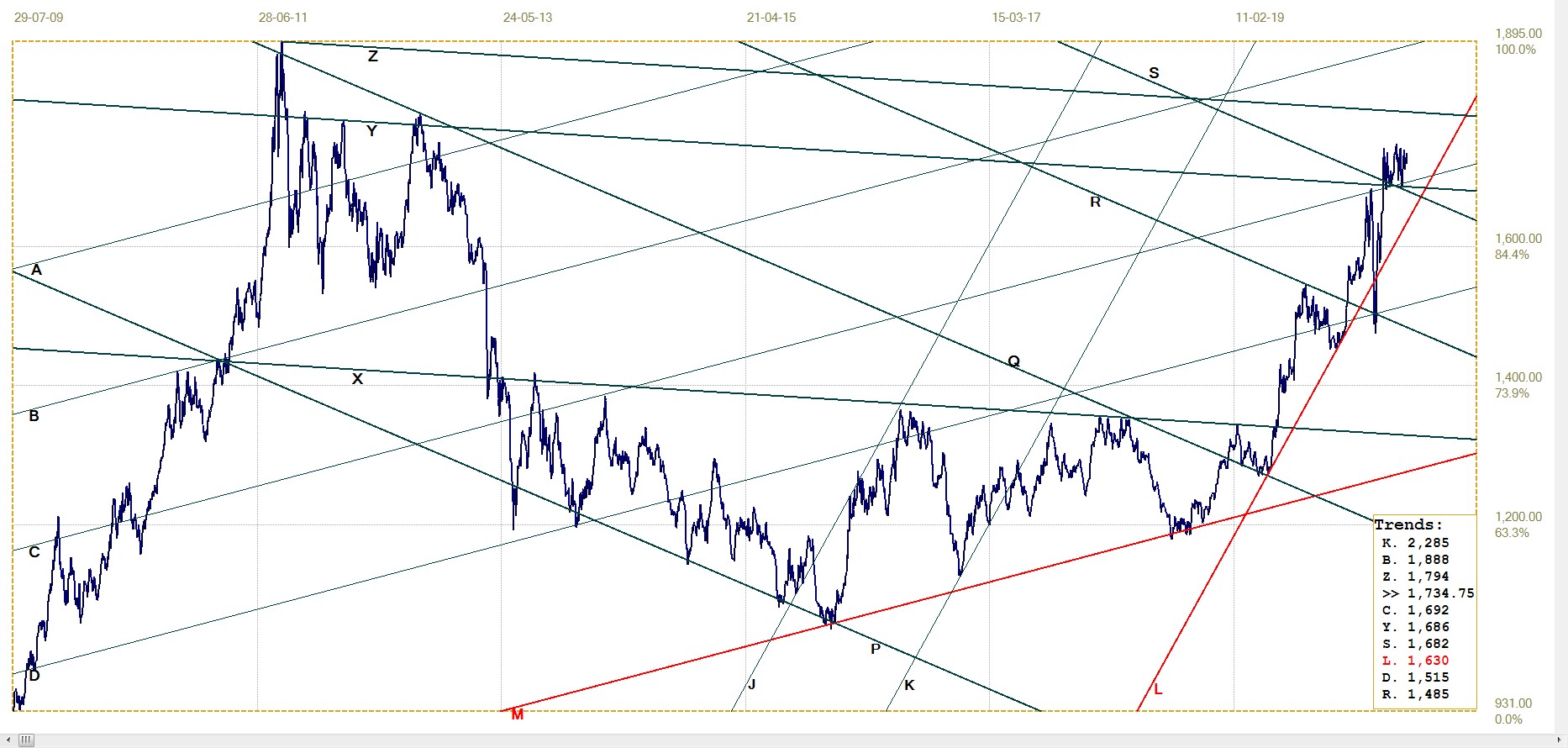

Euro–Dollar

After failing to extend the new rally above channel YZ ($1.1334), the euro pulled back into a sideways consolidation. A week ago it was challenging line Z again, but last week the euro reacted to the resurging dollar to end the week at the low point of the consolidation. A break above line Z has to confirm at the top of channel RS ($1.1338).

A definite and extending break above the long term bear pattern within and below channel XYZ while most or all of Europe is in the same invalid state as the US due to the COVID-19 infestation, might be a warning the dollar is really on its way to going hyper, as so many commentators have been saying. Will the Fed be able to control the situation if that were to happen?

Euro–dollar, last = $1.1177 (www.investing.com)

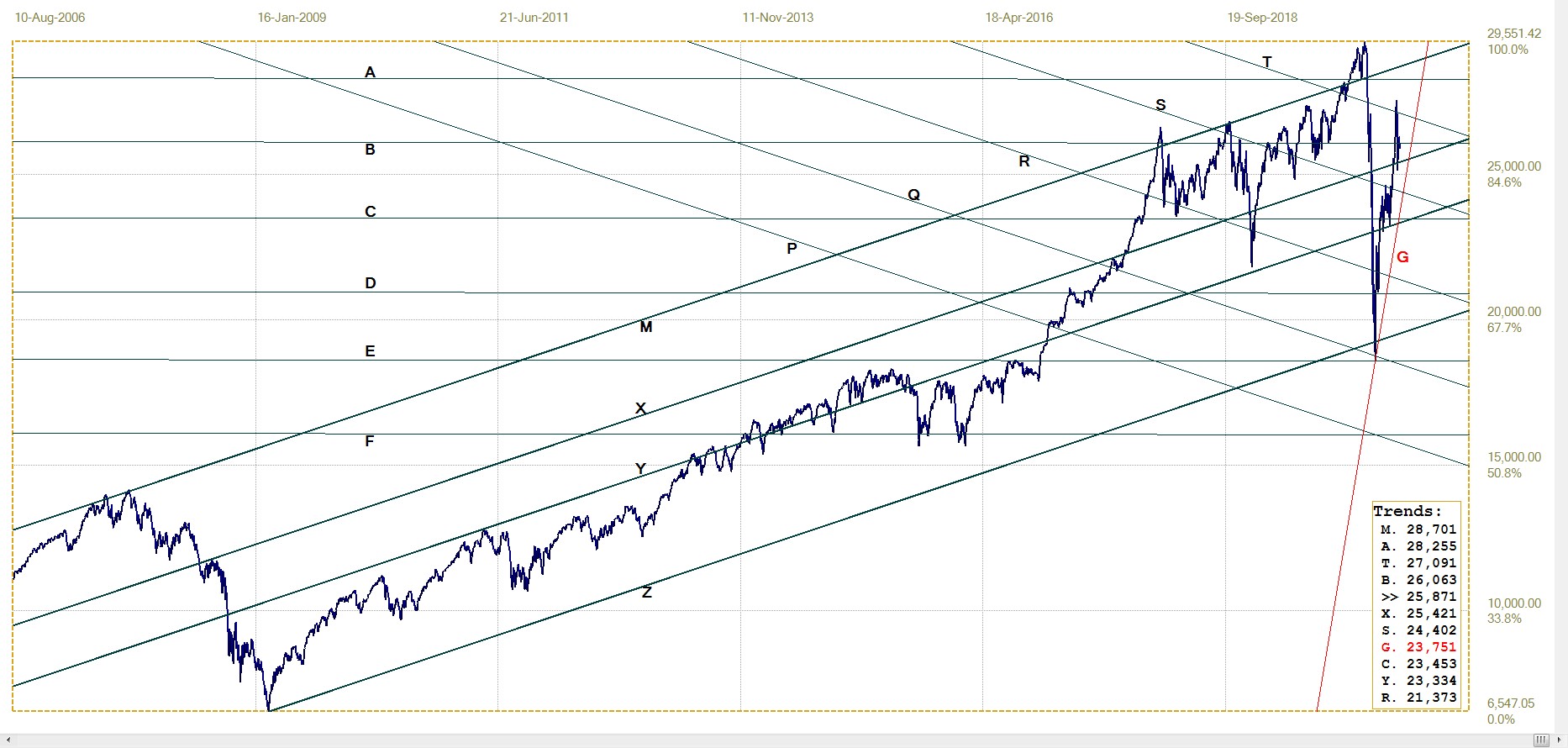

DJIA Daily close

DJIA, last = 25871.46 (money.cnn.com)

The steep rally that had started after 23 March, consolidated between lines C (23 453) and S (24 402) before the rally resumed to break above line T; the 48% gain off line E then failed to hold the break higher and the DJIA broke below the support of lines T (27 091) and B (26 063) for a bearish signal.

It remains to be seen whether expected renewed selling after the increase in recent fresh COVID-19 infections will overwhelm the efforts of the PPT to support the stock market. Nevertheless, given the persistence of support so far, it might be unwise to take out a heavy bet on the Bear soon taking over. The Fed has deep pockets.

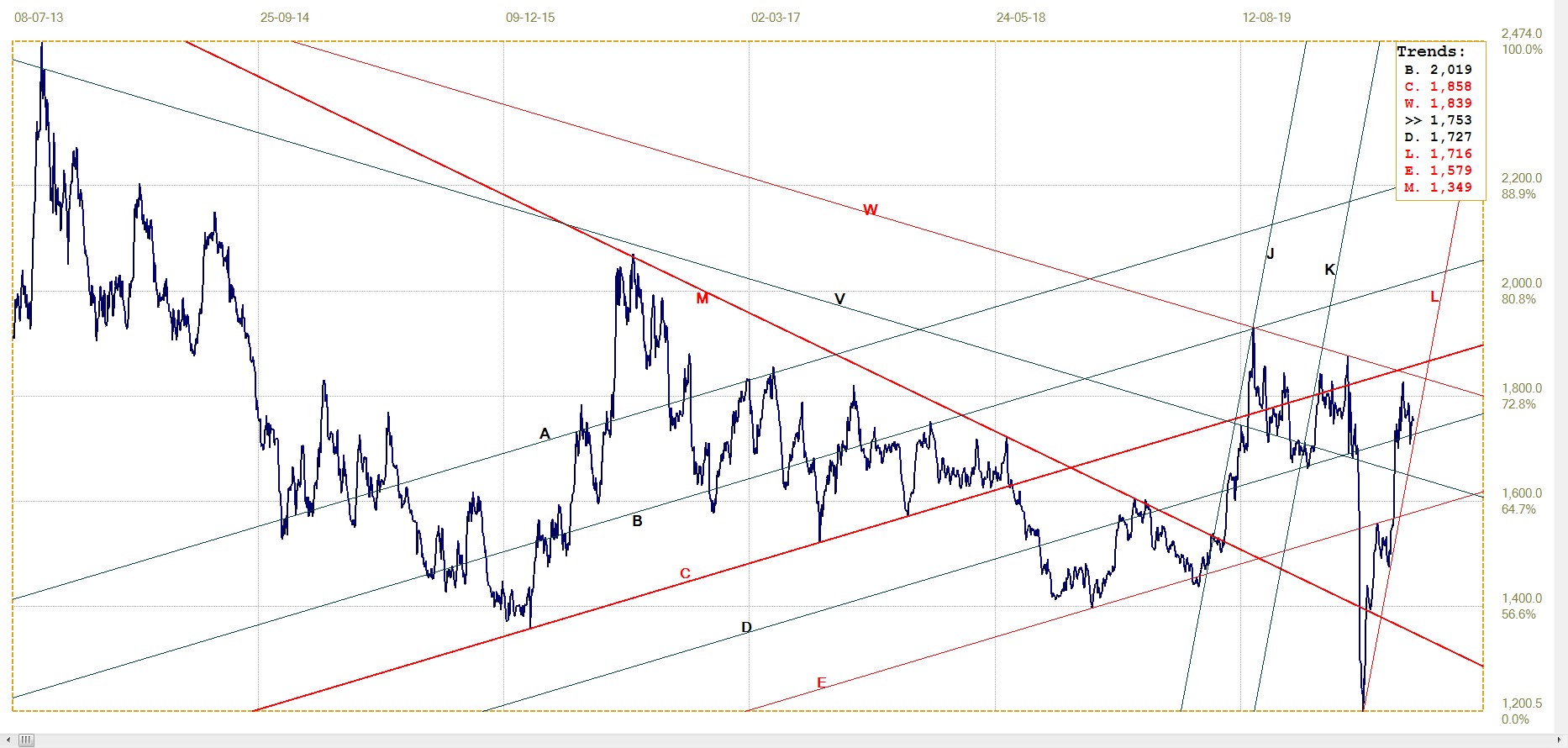

Gold London PM fix – Dollars

Gold made its break above the channels RS ($1682) and XY ($1686) and line C ($1692) over the long Easter weekend and since then used them as support for a volatile consolidation that has a high point of $1748. Friday’s close at $1743 is launching a challenge to set a new high on Monday, with the later PM fix. However, to do so, it will have to overcome the typical early Monday morning attack on the price during Asian trading hours. The new spike in COVID infections might be the spark that gold and silver needs to attract renewed buyer interest.

Gold price – London PM fix, last = $1734,75 (www.kitco.com )

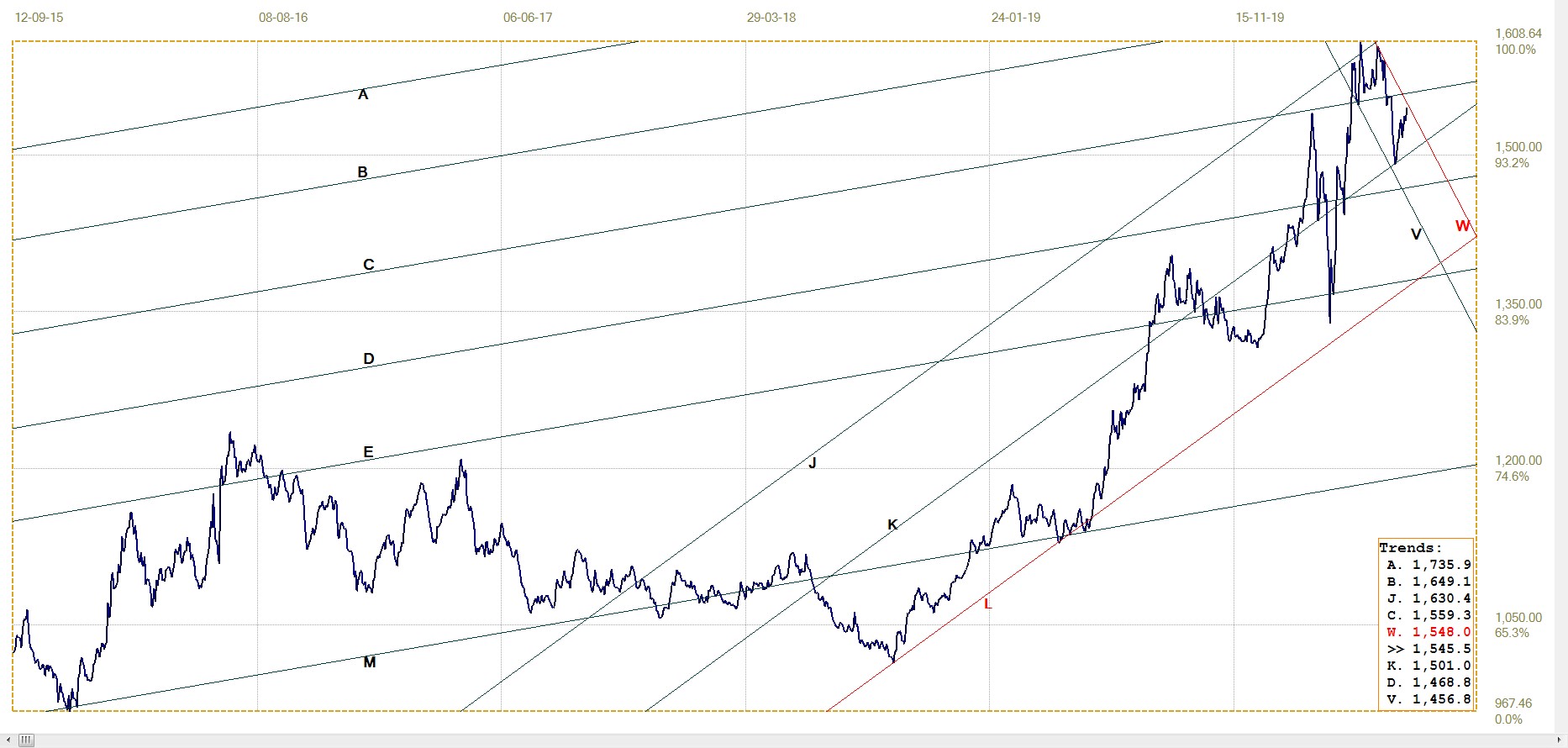

Euro–gold PM fix

Euro gold price – PM fix in Euro, last = €1545.50 (www.kitco.com)

The weaker euro – in reaction to the firmer dollar – during the past two weeks has seen the euro price rallying off its support at line K (€1501) to approach and the top of bear channel VW (€1548) and prepare for a challenge. The recovery of the dollar clearly has a role to play in positioning the economy to favour the narrative that is flowing from the White House for voter consumption – and to block possible claims that Trump’s policies are bad for the dollar.

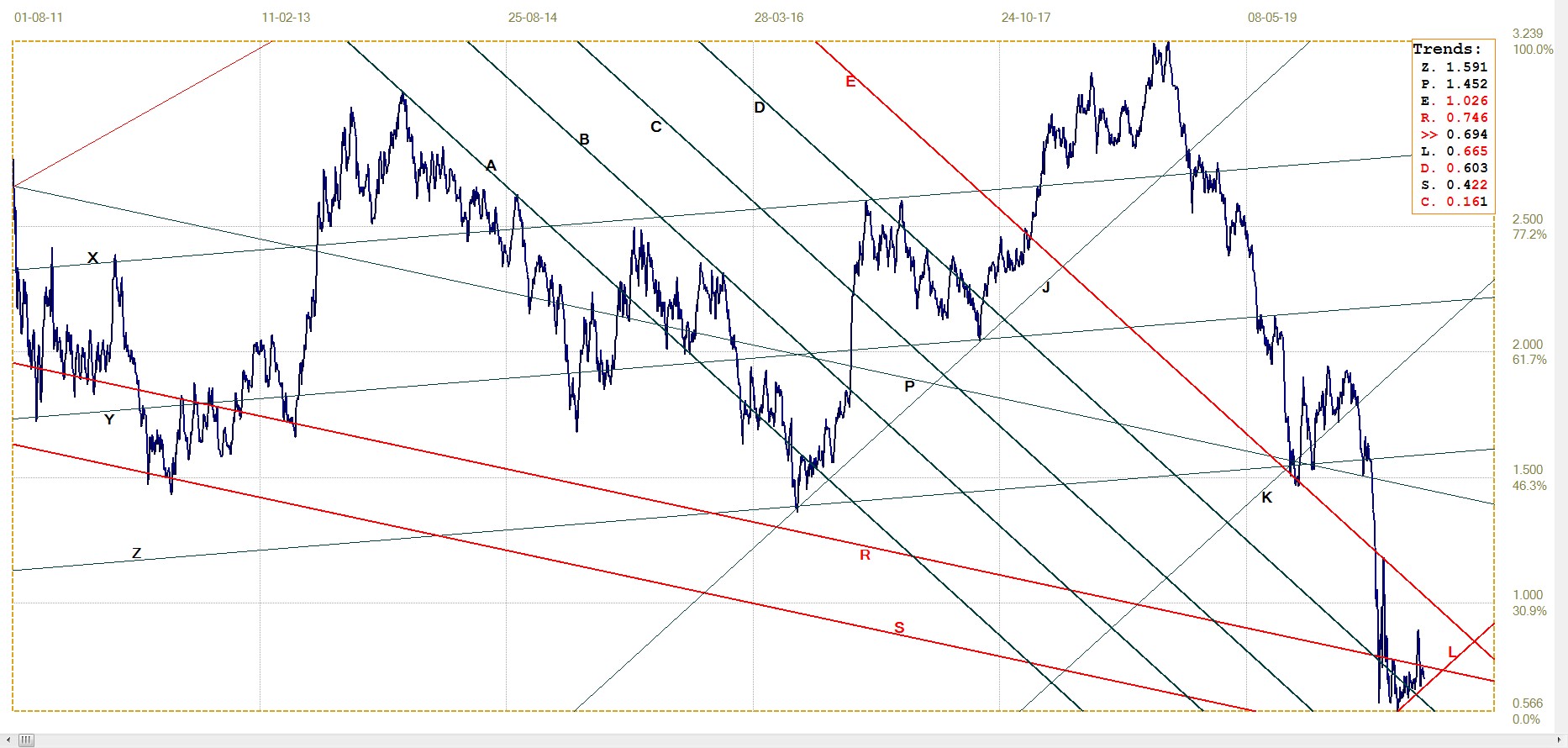

Silver Daily London Fix

There is a near unanimous opinion among letter authors that silver has all that is required to outperform gold once the brakes are off and the bull market breaks loose. Technically, the potential is there as long as bull channel KL ($17.16) can hold and provided the price manages a break above nearby resistance at lines W ($18.39) and C ($18.58). Should the rally extend above line B, this will imply that silver has broken the psychological $20 barrier with potential to move much higher.

The economic law of price and demand finds resonance in what I have recently read about Ancient Egypt. While gold was relatively widely spread in the old first empires silver was not. Discovery of a silver piece that was interred with a mummified body, was interpreted as evidence that someone regarded the dead person very highly. Small objects of gold are relatively common even with other burials than the royal house, but silver was regarded as too precious to be lost forever.

Silver daily London fix, last = $17.525 (www.kitco.com)

U.S. 10–year Treasury Note

U.S. 10–year Treasury note, last = 0.694% (www.investing.com )

Following the spike higher after the unexpected NFP number, the yield on the 10-year Treasury note returned to the narrowing region between lines R (0.746%) and L(0.665%). This new stability in the bond market, after the recent high volatility – which must have created turmoil in the large bond futures market – indicates that a silent hand has been extended to the bond market to bring calmness and stability, to give the shaken banks an opportunity to get their books balanced again.

West Texas Intermediate crude. Daily close

WTI crude – Daily close, last = $39.75 (www.investing.com )

It looks as if the oil price has also found a niche just below $40/bbl where the price is high enough to enable a good fraction of the fracking wells to operate at break-even level or, for some, even in profit. Yet, at a price not so high that it threatens the recovery in the economy; that is, if COVID is going to allow the breathing space for that to happen without fresh interruptions.

*********

More from Gold-Eagle