A Changing World

For the most part, my life has been simple and cloistered. Being a loner of course had consequences. My outlook on life was naive; I tended to accept life in general and people in particular at face value. When I read about the Illuminati and their ilk, my instinctive reaction was one of disbelief; so many rumours, but no real hard evidence. What I could believe were the chart patterns that could be generated with software I had developed. My restricted world view changed early in 1996 when the gold price failed to behave as anticipated when it broke higher from a multi-year triangle.

Interest in gold had me becoming active on the Gold-Eagle forum, just in time to join a debate on whether the LBMA’s claim, after decades of secrecy, that their daily trade in gold averaging 900 tons, referred to bullion or only paper. I explained that the high volume would be a real logistics nightmare if gold changed ownership at that rate and thus, if the gold was not moved out of the vaults, the LBMA was essentially involved in paper trading. Reading all that was said in forums and media, and being persuaded by the evidence, I became a full believer in the suppression of the gold price.

It was easy to understand the motive for the price suppression, given the near daily refrain from Clinton and Rubin about the need for a ‘strong dollar.’ But the concept of a conspiracy among the elites planning the future of the world nevertheless seemed so improbable to either engineer or to keep under wraps, that I did not consider the rumours to be true. Then we in South Africa experienced the campaign to achieve state capture by the Gupta brothers in cahoots with President Zuma during his 10 years’ reign of corruption. That attempt which luckily failed showed what could be achieved, surpassing the previous level of corruption by far.

During this time, the Davos-inspired “Great Reset” developed its own narrative and it became clear that the roots of the New Age view of a one world state in some fashion or another was being seriously pursued at the highest level. In the US, this world view had origins in the years of the senior Bush president, while the Clinton administration brought changes that confused me, since there appeared to be a strategy being put in place to impoverish the middle class. Initially, this did not make much sense. What would be the benefit to the US if the middle class became poor and thus stretched the wealth gap between those with money and those without?

When the junior Bush became president, I thought that we would see a reversal in this trend. The middle class would come into its own again, with salaries and wages able to keep pace with actual increases in prices and not tied to a denatured CPI. Then 9/11 brought a new focus and the quick reaction to punish the instigators suggested that things could change. But other for the military adventures in Afghanistan, there was little or no change to trends set in the Clinton era to weaken the US.

It gradually sunk in during the Obama years that the US was being carefully prepared for the new world order, with Hilary ready to take over after the two Obama terms and to complete the transition of America. Success in this NWO global objective rests almost exclusively on the creation of a worldwide union of states consisting mostly of nominal equals. There had to be a balance of power at the top since this would not work when there is one dominant player, as the US had been since the Iron Curtain had rusted through. When China was still relatively small, this meant the US had to be handicapped or otherwise prepared to quietly accept the loss of prestige and power it used to enjoy before merging quietly into the new world order. A tame and obedient US middle class would be essential for the NWO to succeed and to achieve this was a key feature of the new doctrine that was planned perhaps as early as the 1990s.

Two things happened to cause a hiccup in the plan. Trump, who with his supporters must have known what was happening, decided to stand for president, and won. Then China also exploded onto the scene as a major global major player, with its economy growing from low on the world ranking in 2000 to challenge the US within little longer than a decade. Trump, despite having a grating personality and being no favourite of mine, at least knew that for the US to sustain its global leadership role it must reclaim the status of the manufacturing nexus of the world, at least to the level where it was no longer reliant on China for much of its consumer goods.

Before he could progress much along the road to more self-sufficiency for the US, the 2020 election happened and Biden moved into the White House with an agenda that is primed with a set of woke ambitions. Fighting global warming is high on the list, and so too is the effort to ensure Democrat hegemony in US politics by their opening the gates to immigrants that would vote the right way in future elections. US demographics no longer will reflect its heritage, but will become a microcosm of the heterogeneous world we live in with a new culture that in time will encompass resignation from the leadership role the US has played since WWII, to become just ‘one of the gang’ on the global stage.

I fear that in this process the original puritan qualities of self reliance, loyalty and hard work to care for family first, will then be replaced by reliance on the state, taking care of number one, driven by whims and fads in order to be considered woke and diverse. Appearance is to replace substance as the most important measure of a person. While diversity and fluidity within limited context is praised, one will be stringently required to conform to the prescribed model behaviour if one is to be accepted by one’s peers.

With Europe likely to be mostly Muslim 20 to 30 years from now, the world currently seems destined to become a very different place from what those of us who had lived much of your lives before 2000 have known. It will be a world in which the pursuit of excellence will be frowned upon; the ideal will be for everyone to become merged into a general mediocrity where nobody stands out from the crowd to cause the others to feel inadequate in any way, whether by genetics or inclination.

The world is changing, as it is wont to do, with one scenario developing as described above. There is another one that is being actively pursued, if one listens to opinions and perhaps plans of influential people. They believe that the world is over-populated with what has been termed since the 1980s as ‘useless eaters’ and that it would be a better place if the population could decrease by up to 80% or even more. The way it could be done is even specified, typically by a planned pandemic. Whether what has swept the world since late 2019 is such an experiment is a moot point, but so far this virus is not having the necessary effect, whether planned or happenstance. At the heart of this debate is Stein’s Law; a trend that cannot continue indefinitely will stop, which clearly also applies to the growth in population.

The talk about a New World Order may have sounded way out in the 1980s, but it is now on the verge of coming to pass. One should not be surprised to find in the not too distant future that the talk about the culling of the species has also progressed to be a long way beyond being just a lot of hot air.

While we wait for gold and silver to assume their proper role in global markets, the above has been a bit of a ramble across the current landscape with a few peeks ahead to what the future might bring. US and international politics are not as stereotyped as these have been, say, during the 1980s, when the world appeared to be set in a mold where options and alternatives were clearly defined. Now the future seems more like a blank sheet with a wide range of possibilities that surely will have significant impact on the way we live.

Euro–Dollar

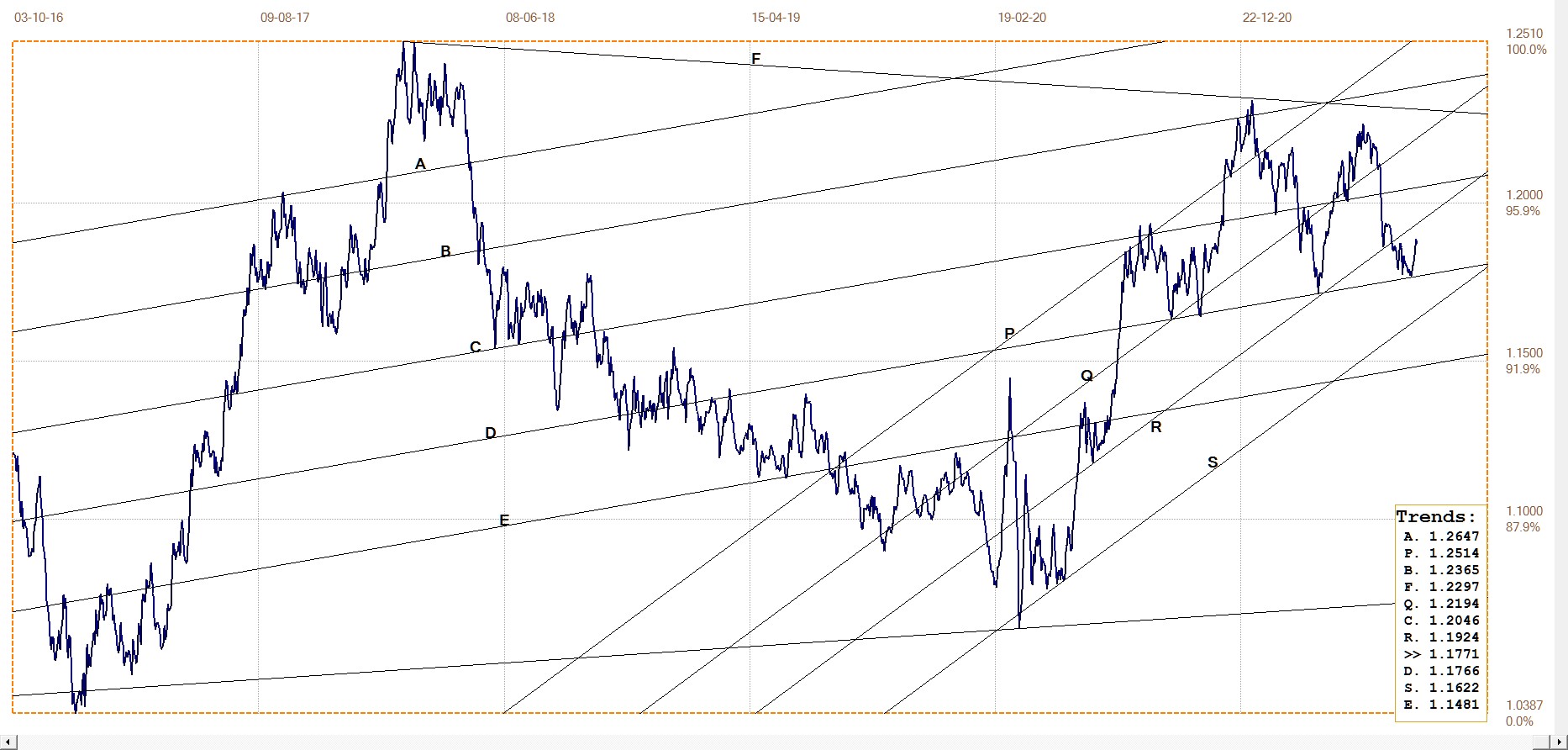

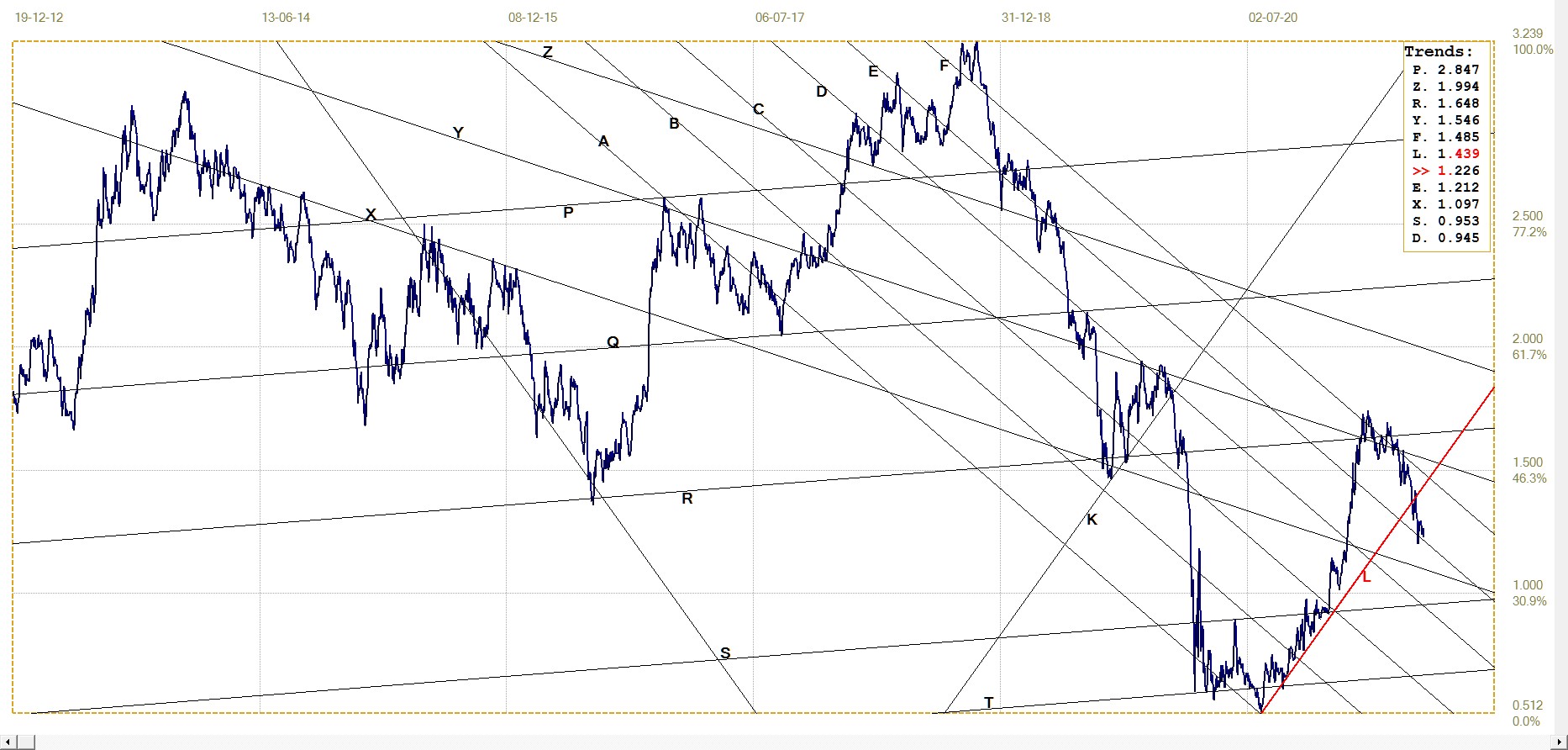

As anticipated on technical grounds in the previous two US Markets, the euro has so far managed to hold at support at line D and then reversed direction to turn mildly bullish again. While safely holding in the broad bull channel PQRS, it spent most of the recent months sitting in upper band of this channel, in channel PQR. The euro has some way still to catch up and break back above line R.

There is much talk in the alternative media about weakness in the dollar to come and even of some risk of hyperinflation in the not too distant future. The knee jerk reaction is to expect the euro to rally substantially against the dollar. However, it should be kept in mind that Europe is not without its own problems and that they are also inclined to use the printing press to address these problems.

Conceivably this could result in a race for the bottom. Should the euro rally back into channel PQR, the odds of such a race will decline a little, with the euro recovering into a stronger technical streak against the dollar – perhaps even able to repeat the break above that channel in due course.

Euro–dollar, last = $1.1870 (www.investing.com)

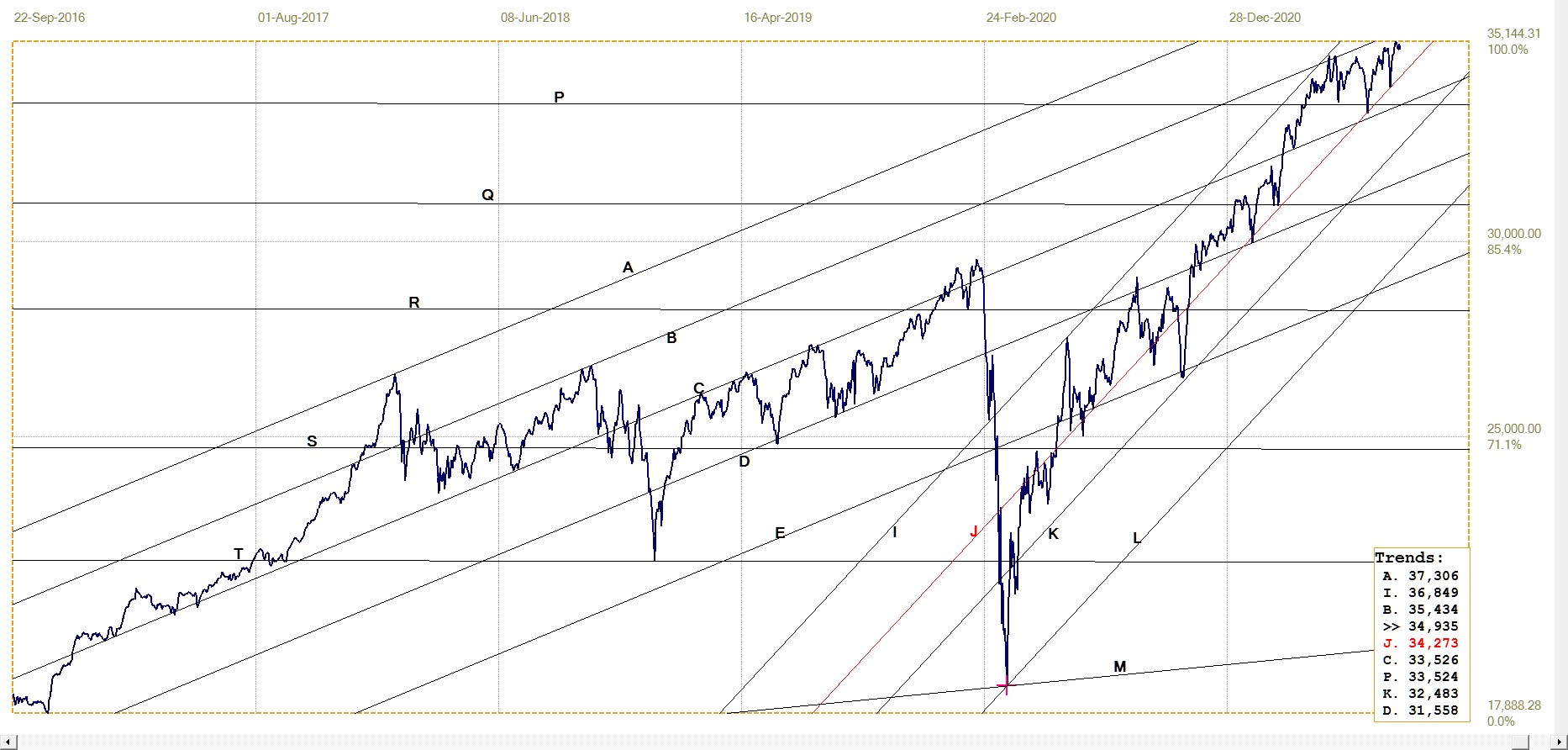

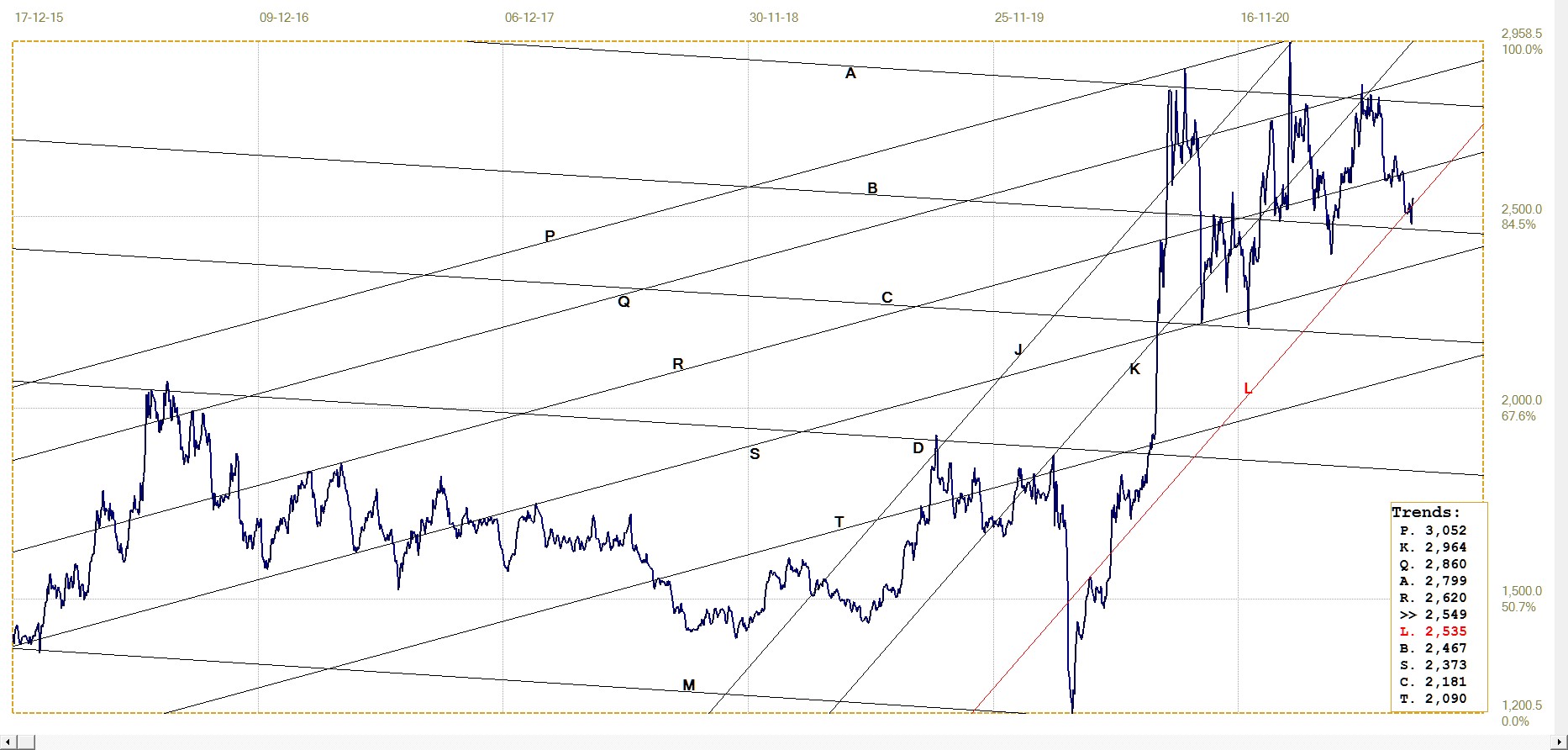

DJIA daily close

DJIA. last = 34935.47 (money.cnn.com)

A new and shallower bull channel IJKL is now used to define the post March-2020 bull market that completely disregarded the COVID pandemic and its effects on the US economy. The gradient of the new bull channel is also derived from master gradient, M, and is one Fibonacci transformation shallower than the bull channel in last week’s report. The fit is again very good, with line J now acting as key support during the two recent attempted sell-offs.

The rising wedge shown recently in the report did break out to the low side as could be expected from completion of the five waves. However, the forces in the stock market – presumably not all strictly typical market forces – have seen to it that the break is more sideways than down. There is quite some room to continue a sideways trend before line J is challenged again, but how long before that happens will depend on the ability of the bullish forces to hold the DJIA near its current level.

Gold London PM fix – Dollars

Gold price – London PM fix, last = $1796.60 (www.kitco.com)

The $1800 ceiling was mostly kept in place until the end of the month to enable the banks to pocket the premiums on gold options. While the price was let loose to above $1800 some of the time, at the key moments in time it was assisted lower to make sure the Banks could bank their profit and then the price was again left to recover above $1800. DTja vu has struck again as it had done innumerable times in the past, right at the time when options expire or contracts will mature to stand for delivery.

Hopefully Stein’s law will apply here as well, in that it is a behaviour that cannot continue indefinitely and will stop.

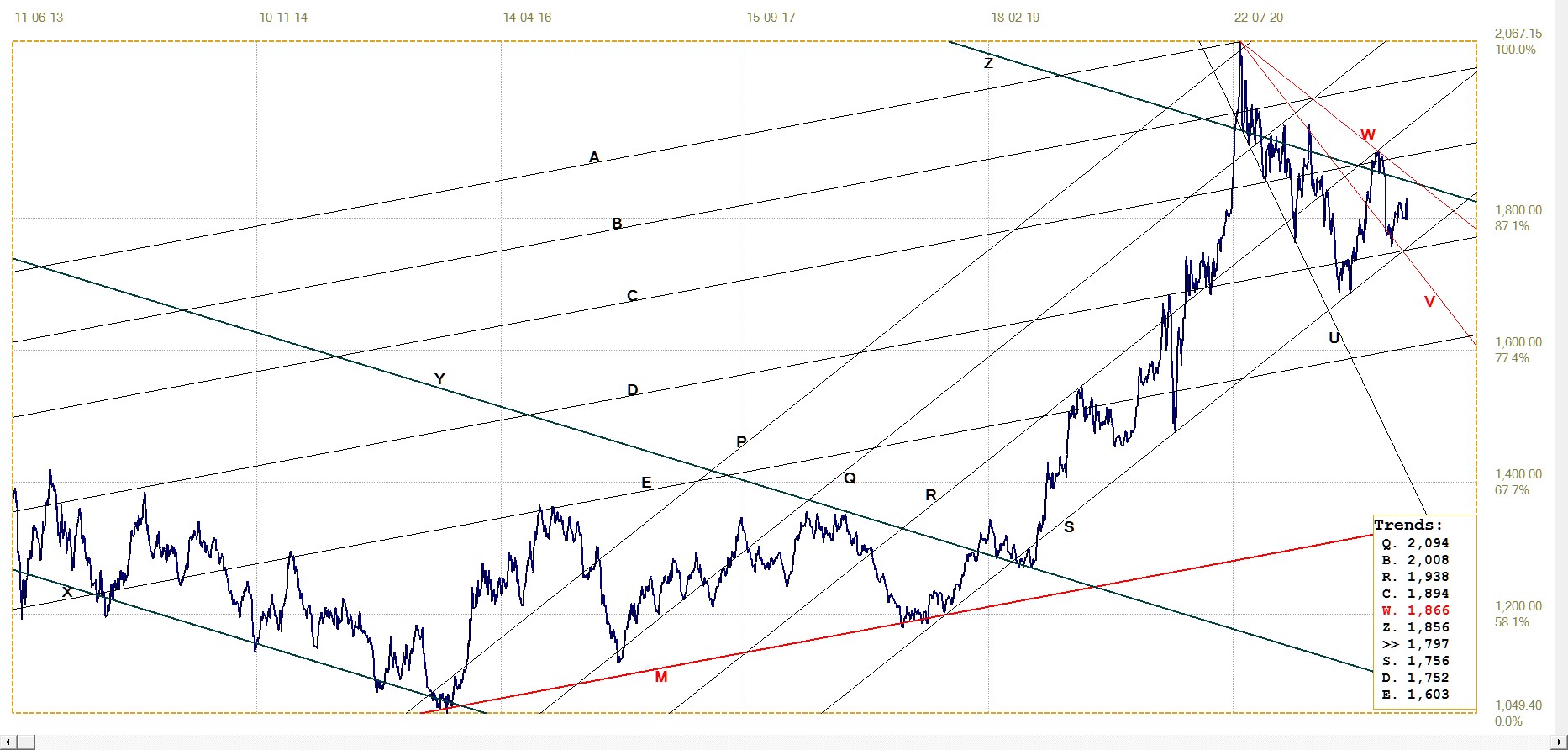

Euro–gold PM fix

The firmer euro last week, combined with an enforced ceiling on the dollar price of gold, meant that the break above line G was not able to extend higher. Instead, the euro price of the metal retreated off the recent top to hold at line G – a behaviour that is often enough seen to be given a name, a ‘good bye kiss’ that serves to confirm the presence of the trend line that has been penetrated.

For that move to qualify as a goodbye kiss, the price has to reverse higher to resume the rising trend that preceded the break higher. A move lower, down to line F, before the rally resumes – if that is what really will happen – cannot be excluded. Line F has served well on more than one occasion as support during the recovery off the bottom of megaphone PE. This kind of chart formation is associated with strong and sustained trends in both directions and a definite break above line G could see something of that kind materialise.

Euro gold price – PM fix in Euro. Last = €1524.24 (www.kitco.com)

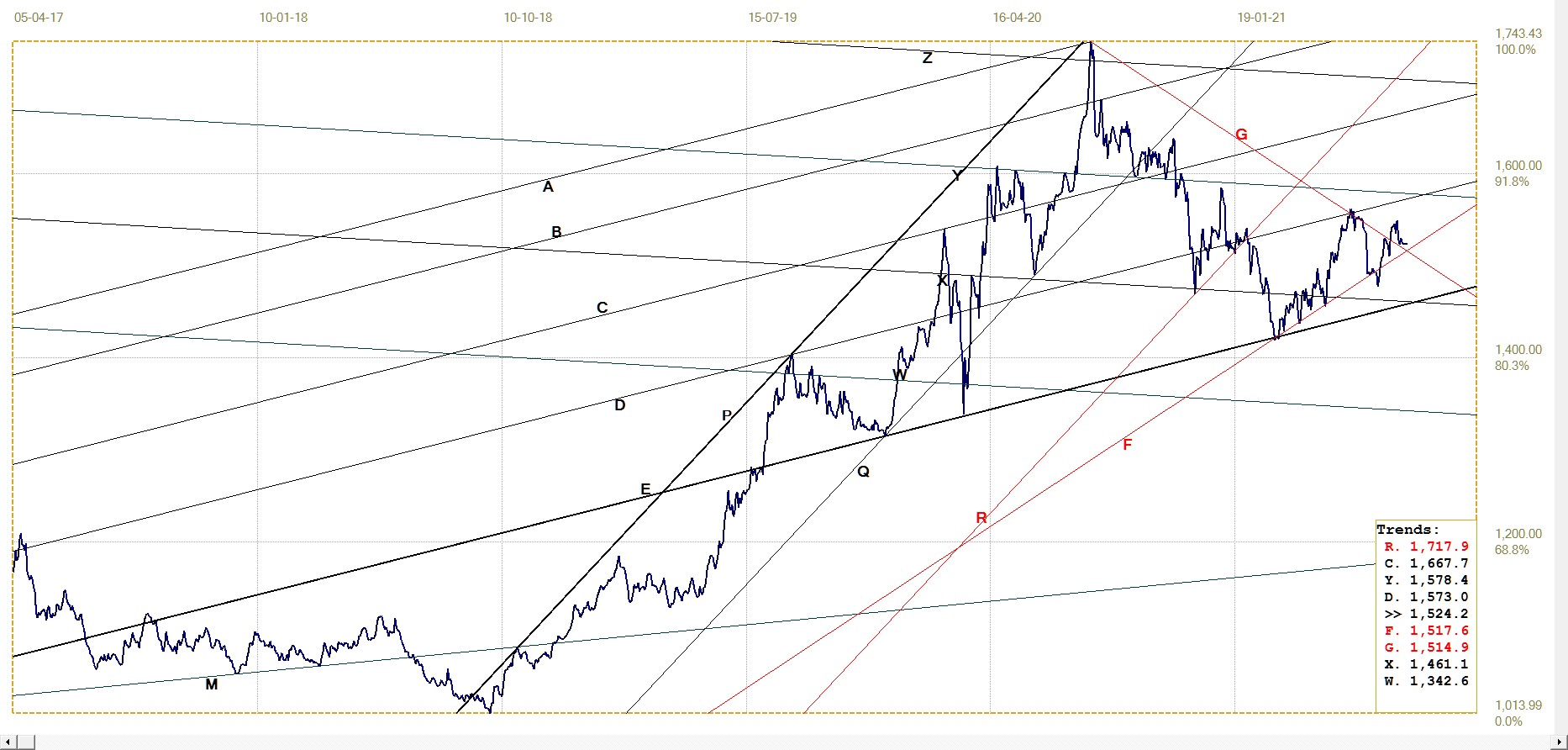

Silver Daily London Fix

After failing to break above channel BA despite several attempts, the silver price fell steeply to ensure that many August options would expire out of the money. The dip to below channel KL, after at first holding at the support, was timed to coincide with the expiration of the options – another example of the luck of the Banks that coincidence favours them much more than the buyers of PM options on COMEX. This happens so often that it is a surprise that the buyers have persisted so long in putting their money at risk with a low probability of collecting what is due. The recently reduced interest in silver in particular might be an indication that this fact is being realised and that silver traders are either saving up for when silver can break free or, heaven forbid, are now looking to Bitcoin and the crypto market as a better proposition.

The recovery back into channel KL is still tentative and August should tell us if the bullish bias will continue to hold.

Silver daily London fix, last = $25.49 (www.kitco.com)

U.S. 10–year Treasury Note

The break below bear channel KL is holding near the low yield levels. This implies that the narrative of a transitory phase of higher inflation is still making sense to the larger players in the bond market. Or is it that the funds flowing out of Wall Street are finding their way into the bond market, as is the traditional practice of the large funds, going back many decades.

Should general price increases – in part fueled by the rising oil price – continue to put the CPI on a rising trend as well, it will be interesting to see how the powers that be react. With a still fragile economy, a counter-acting increase in interest rates will be most unwelcome. Given the widespread fiddling with markets and the need to keep rates low, it would not surprise to see a widening gap between the official CPI and one’s personal experience of changes in consumer prices.

U.S. 10–year Treasury note, last = 1.226% (www.investing.com )

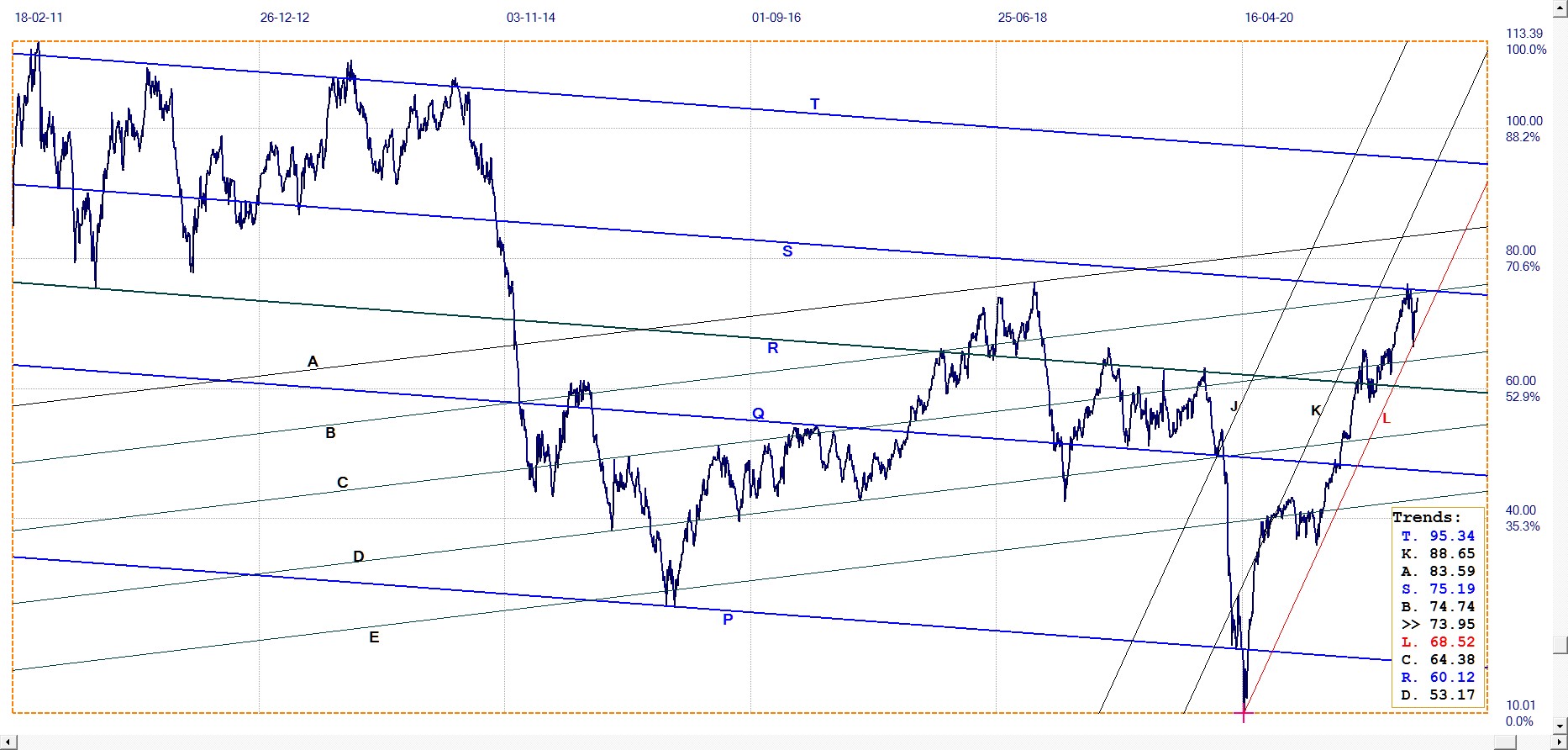

West Texas Intermediate crude. Daily close

WTI crude – Daily close, last = $73.95 (www.investing.com )

The price of crude is holding closely within bull channel KL, having just rebounded steeply off line L to reverse the recent trend to lower prices for crude oil. The move higher within into channel KL again, as stated last week, is a bullish warning that will only take full effect on a definite break above lines B and S to continue higher in the bull channel. Should this happen, the ripples will spread far and wide through the economy to repeat the finding in the latest CPI, namely that expensive fossil fuel is one of the key drivers of the rising trend in the CPI.

*********

More from Gold-Eagle