Dancing…Again…On Gold’s Seeming Grave

You would think that an asset that had been in a rip-roaring bull market for a dozen years and finally, after all that time, suffered an annual decline would still garner some attention and respect. Yet such is not the case with that most desirable of metals known as "AU" on the periodic table.

You would think that an asset that had been in a rip-roaring bull market for a dozen years and finally, after all that time, suffered an annual decline would still garner some attention and respect. Yet such is not the case with that most desirable of metals known as "AU" on the periodic table.

Particularly due to the magnitude of the decline (from its 2011 top to its December 31 second bottom in the $1,180/ounce area, it's dropped some 38%) gold has been laughed at. Pretty much everyone not a dyed-in-the-wool gold bug has piled on, scorning the "barbarous relic" as having been a disaster for those who got sucked into this "bubble." And the carnage is not over, many claim; even some who believe in the longer-term bullish case for the yellow metal warn that this asset is so damaged technically--and the near-term case "I tell ya, gold gets less respect than I did!" for owning it so dubious according to themainstream financial press--that it will fall farther.

The narrative against gold specifically -- and precious metals generally -- is broad, if somewhat ill-informed (and in some cases self-serving.) In the self-serving department in particular we have Goldman Sachs; this quasi-governmental bank has long since taken over for the likes of Barrick Gold, Republic Bank of New York and J.P. Morgan as THE ogre that gold bugs most love to hate. After having successfully orchestrated a bear raid on gold last Spring and slammed it below what at the time had been solid technical support in the $1,525/ounce area, Goldman now says the metal will decline to $1,000/ounce this year. (Never mind that Goldman's market timing calls on most everything are just as often dubious as they are accurate; they said gold's goose was cooked at $700/ounce a few years back.)

The narrative against gold specifically -- and precious metals generally -- is broad, if somewhat ill-informed (and in some cases self-serving.) In the self-serving department in particular we have Goldman Sachs; this quasi-governmental bank has long since taken over for the likes of Barrick Gold, Republic Bank of New York and J.P. Morgan as THE ogre that gold bugs most love to hate. After having successfully orchestrated a bear raid on gold last Spring and slammed it below what at the time had been solid technical support in the $1,525/ounce area, Goldman now says the metal will decline to $1,000/ounce this year. (Never mind that Goldman's market timing calls on most everything are just as often dubious as they are accurate; they said gold's goose was cooked at $700/ounce a few years back.)

It's hard to know where to start in taking issue with these varying assumptions that have, for now, contributed to the bearish mood for gold. But over the next few pages, I'm going to give it that old college try! And as I do I will first stress again, as I have oft reminded you folks and others, that I am NOT a static "gold bug." Philosophically, I certainly am to some extent. I believe that not only gold, but silver, tobacco, whiskey, community currencies, some of the newfangled digital currencies and other things can and should be used as money.

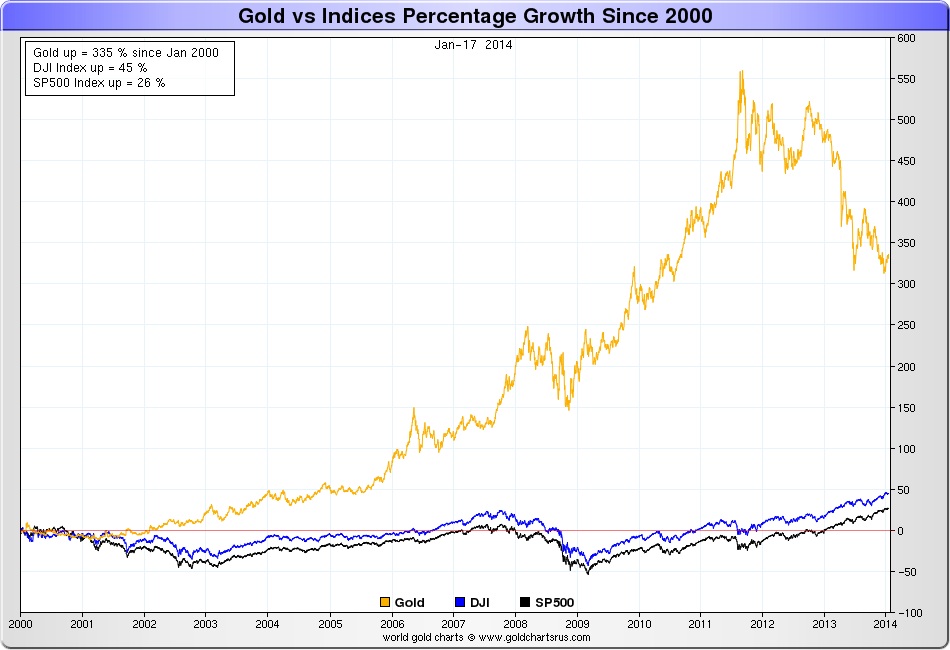

But as a practical matter, I am NOT a gold bug. It's not that hard to take issue with what I believe is a very flawed way in which the markets presently view gold; Moody's comments above are indeed an apt microcosm. For starters -- as the nearby chart courtesy of my old friend Nick Laird at www.sharelynx.com illustrates -- even after its recent shellacking, the yellow metal has still FAR outpaced the returns from equities since 2000.

A CHANGED SUPPLY-AND-DEMAND EQUATION

In a friendly and wide-ranging discussion with a colleague recently, I opined that pretty much nothing behaves and works as it did over three decades ago when I first got into the financial/investment field. Generally speaking, stocks react far more to financial than to fundamental factors. Bonds have been artificially priced for several years now, influenced chiefly by central bank monetizing of debt than any semblance of traditional, real-world measures of risk. So, too, have the supply and demand factors for gold been undergoing a change; but where the yellow metal is concerned, those changes are much less artificial and, frankly, easier to quantify.

But this has changed dramatically over the last few years. As gold was peaking at a bit over $1,900/ounce back in late 2011, the net demand from the world's central banks together with investment demand had almost turned this ratio completely upside down! Nearly 60% of overall demand had nothing to do with gold as a product of some kind, but due to its role as an asset class; as money.

I believe this trend will continue, if not become more pronounced. It is my belief that the world now is choking on too much debt and overcapacity. Emerging nations like China and India which had provided a lot of the "oomph" in the past for gold jewelry have problems. Policymakers the world over know how tenuous things are, and that they need to keep printing gobs of money not so much to reinvigorate growth, but to keep everything from imploding and bringing on a global, deflationary depression. In short, I do not see the world's consumers being the anchor for gold demand for quite a while.

Net demand by central banks -- especially in emerging countries like China, which by most appearances is acquiring a vast stockpile of gold with which to some day anchor a new reserve currency at least for Asia, if not the world -- will probably stay strong. But more than likely, the demand will come off its recent pace for a while.

Thus, gold's drop from over $1,900/ounce to present levels had less to do with any conspiracy or cartel (the obvious bear raid orchestrated by Goldman Sachs last year notwithstanding) than it did with the simple fact that one of its biggest "constituents" had left the party after first juicing it up.

WHY THE U.S. DOLLAR MATTERS LESS GOING FORWARD

One of the proofs that the secular gold move that began in 2001 became driven increasingly by investors and central banks looking to it as a monetary asset is how gold's relationship to the U.S. dollar changed DRASTICALLY.

One of the proofs that the secular gold move that began in 2001 became driven increasingly by investors and central banks looking to it as a monetary asset is how gold's relationship to the U.S. dollar changed DRASTICALLY.

From late 2001 through 2005, the U.S. Dollar Index plunged by a third; from, roughly, the 120 to the 80 area. During that same time, gold "correspondingly" jumped, from its $260/ounce or so low to the $425-450/ounce area.

THE CENTRAL BANKS' FIGHT AGAINST DEFLATION

Some bona-fide crazy notions get into the markets' head now and again. One I want to call particular attention to now is that there has been a growing belief for weeks that the Federal Reserve will be completely unwinding/exiting from its current quantitative easing ("Q.E.") program by the end of 2014, the economy is doing so well and the world's trouble spots having been neutralized. The thinking has pretty much been (at least until Thursday the 22nd as I finish this issue up) that at next week's F.O.M.C. meeting -- where outgoing Chairman Ben ("You Won't Have 'The Bernank' to Kick Around Anymore!") Bernanke will get his gold watch and say his good-byes -- the Fed would announce a second cut of $10 billion to the bank's debt monetizing efforts. Further, as long as unemployment keeps declining and no troubles manifest themselves, the ensuing seven meetings during 2014 would see similar "tapering" until we get to the end of the year and there is NO MORE Q.E.

The idea that the Fed -- for our present purposes -- would make this developing bad dream into a NIGHTMARE by trying to exit its "extraordinary measures" is absurd. Especially if the pattern of the early days of 2014 continues (this week particularly) and we see stocks unraveling on Wall Street, defaults in China, the would-be host of the 2016 Summer Olympics blowing up, or (fill in the blank here) any talk of further tapering will be dispensed with quickly.

TO BE CONTINUED: In the next couple issues, I'll be talking more about gold specifically, and the metals/miners in a broader sense. As I said above in regard to the changing factors involving gold itself -- ones which gold bugs don't even seem to get at times -- the landscape for mining companies and their real and perceived attributes is going to change drastically going forward as well.

To be sure, many mining stocks generally are astonishingly -- even insanely -- CHEAP right now. But I fear the mistake that some will soon make is to pile into pretty much anything to do with gold and silver, especially if we get a breakout close above the $1,265-1,270 area for gold which causes BOTH new speculative/investment buying, and a bigger scramble to cover short positions. The knee jerk reaction will be that almost anything to do with metals moves higher. Indeed, we've already seen some big percentage moves (albeit, mostly in companies that were already down 80-90% from their highs) as bargain hunters step in to try to get companies at the bottom (they hope!)

Thus -- though there will be unique reasons why precious metals will do well in almost any conceivable environment -- anything to do with industrial metals will generally lag. For those most dependent on economic growth, company stories will need to be truly superior -- and in the case of exploration plays, the discoveries truly impressive -- to get my attention.

NEW RECOMMENDATIONS

In the case of junior metals exploration companies, one can find but a handful not selling for a small fraction of its price of a year or two ago (though the first of the two NEW opportunities below is an exception.) It's one thing that mining stocks generally are a shambles; even the "majors" were pretty much cut in half last year, as measured by indices such as the HUI and the XAU. Where the more speculative, non-producing companies are concerned, 80-90% losses in share price are common. Many are on life support. Some have already gone kaput, or will this year.

In the case of junior metals exploration companies, one can find but a handful not selling for a small fraction of its price of a year or two ago (though the first of the two NEW opportunities below is an exception.) It's one thing that mining stocks generally are a shambles; even the "majors" were pretty much cut in half last year, as measured by indices such as the HUI and the XAU. Where the more speculative, non-producing companies are concerned, 80-90% losses in share price are common. Many are on life support. Some have already gone kaput, or will this year.

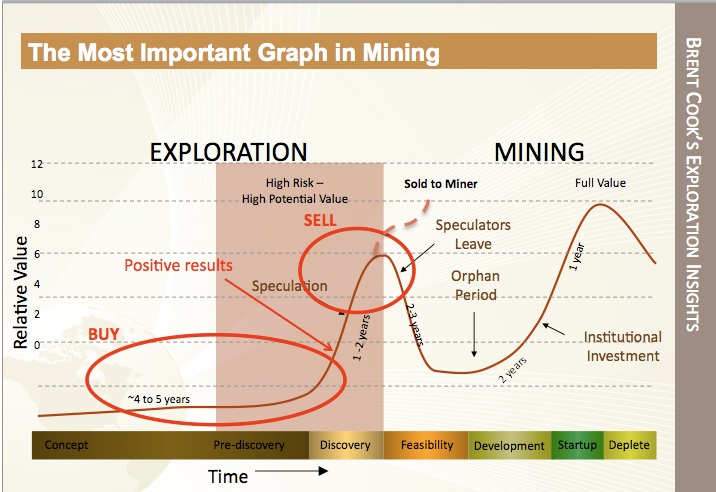

Nevertheless -- when timed anywhere near right, and when proper homework is done -- few segments of the stock market universe offer gains more explosive as can be gleaned from resource companies. As the accompanying graphic shows, some of the most incredible gains for shareholders come as discoveries are made and proven up, and a substantial new resource is unveiled.

The "really bad" got really bad this time around. In recent months, as you know, I have been slowly, methodically getting acquainted with some additional stories. I have been in no great hurry to be adding companies in this sector, as much as I believe that most of the damage is finally over. But at the same time, I feel that some companies can (and should) be bought now, even if we get "whipsawed" where the metals are concerned, and those warning that gold could still tumble to $1,000/ounce are proven right.

Though the medium-to-larger companies will for the most part mirror the moves in metals prices, I think it can be said that the smaller explorers are going to be less apt to do this, and instead trade on their own unique stories and developments. Are they making great progress in uncovering/developing a truly eye-catching resource? Does management know what it's doing? Can they raise money? Is the overall story compelling, if not off the charts?

********

(Courtesy of http://www.nationalinvestor.com/ )