Exploring COMEX Gold And Silver

There is widespread disappointment in the PM camp now that we are almost 3 weeks into the new BASEL lll regime and little has happened. With new rules to differentiate between allocated and unallocated gold on the books of the banks, with substantial cost implications for unallocated gold, nothing much appears to have changed on the gold front. Silver is perhaps another matter, because the price has not shown similar recovery to what gold has done, albeit slowly until last week. It seemed an interesting exercise to look at other differences in the treatment of silver and gold by the Cartel.

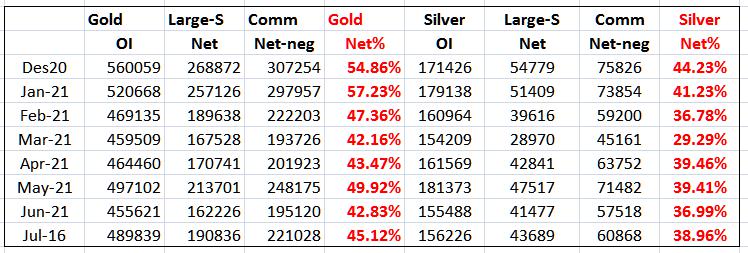

Sun Tzu advises that one should put oneself in the position of one’s opponent and try to think how he would think under the given circumstances. It becomes even better when one has a history of how he had behaved under similar circumstances, from which one can deduce what he considers a threat or a source of risk. The table below is an attempt to visualise the reactions of the Big Banks in terms of their positions on the COMEX exchange in gold and silver as from December last year.

This year has delivered them a future problem and a shock. The future problem was the BASEL lll rules that would take effect in July; the shock was the reaction of the REDDIT Apes-to-be after they had dealt with the hedge funds so dangerously short of GameStop et al. The table presents the COMEX OI for gold and silver and then for each metal the net exposure of the Large Specs and Commercials.

The net number of positions for the Commercials are then expressed as a percentage of the open interest – which in effect is a measure of how much they are willing to risk in order to suppress the prices of the metals. A low percentage implies that the Banks also carry a significant number of long positions to hedge part of their shorts.

(COMEX and Barchart.com)

A first point is that the percentage of the net positions relative to the OI has not achieved the same highs of December and January. If the premise that the number is indicative of the degree of their hedging of short positions – and if Dec/Jan is broadly indicative of what used to be the earlier norm – it means there has been a significant change in the perception of risk by the Cartel.

For both metals there is a significant change in the degree to which short positions are hedged after January. At that time, GameStop was in the news with the message that hedge funds that have gone too much short on the stock market opened themselves to a short squeeze. It does not take a genius to recognise that the Cartel was similarly exposed and to a substantial degree – which they partially rectified by February for both their gold and silver positions.

When the REDDIT Apes changed their focus to silver, gathering more forces than they had mustered late in February, the Cartel reacted by reducing their short exposure in both metals. For gold the OI in March was lower by 11.7% from the January number and for silver the decline in OI was almost 14%. The decline in the OI tells only part of the story: using the net-percentage as a measure of how the CABAL perceives the risk of their short positions, in the case of gold it declined from 57.23% to 42.16%. Silver shows a decline from 41.23% to 29.29% - a 56% decline in the hedging compared to 26% for gold.

The threat from the Apes clearly had influenced the Banks to be more careful of silver than of gold, although other factors such as available reserves surely also featured in their estimates of the risk. February was nevertheless the low point in both sequences of the measure of estimated risk, with gold at 42.16% and silver at 29.29% and also serving as a measure of the greater risk silver posed in the estimates of the Banks.

Subsequent to March the Banks maintained much the same higher risk profile for gold near the lower level that was established in March. Given the distinct high risk silver posed in March, the risk measure improved from the Banks to also settle at a much reduced degree of hedging, yet still with more cover than in December.

The total OI for both metals is much lower than it used to be six months or so ago. This by itself shows that the Cartel has toned down their exposure to risk. It firstly means that BASEL lll so far has had little effect on the Cartel’s management of their gold short positions.

Secondly, that the Cartel could relax the hedging of silver shorts means that they are more confident of managing any threat silver could pose. Reducing the hedging is also a consequence of the much lower silver OI after May. Because the hedging in silver has held constant since April, while the OI has now declined, it probably means that demand for silver contracts on COMEX has declined more than for gold contracts, at least if the situation as discussed above remains similar between gold and silver.

Reduced demand reduces the overall risk for the Cartel while making it easier to keep control of the price. This in turn means that the possibility of a short squeeze is also reduced, since silver deliveries are less likely to result from investment demand.

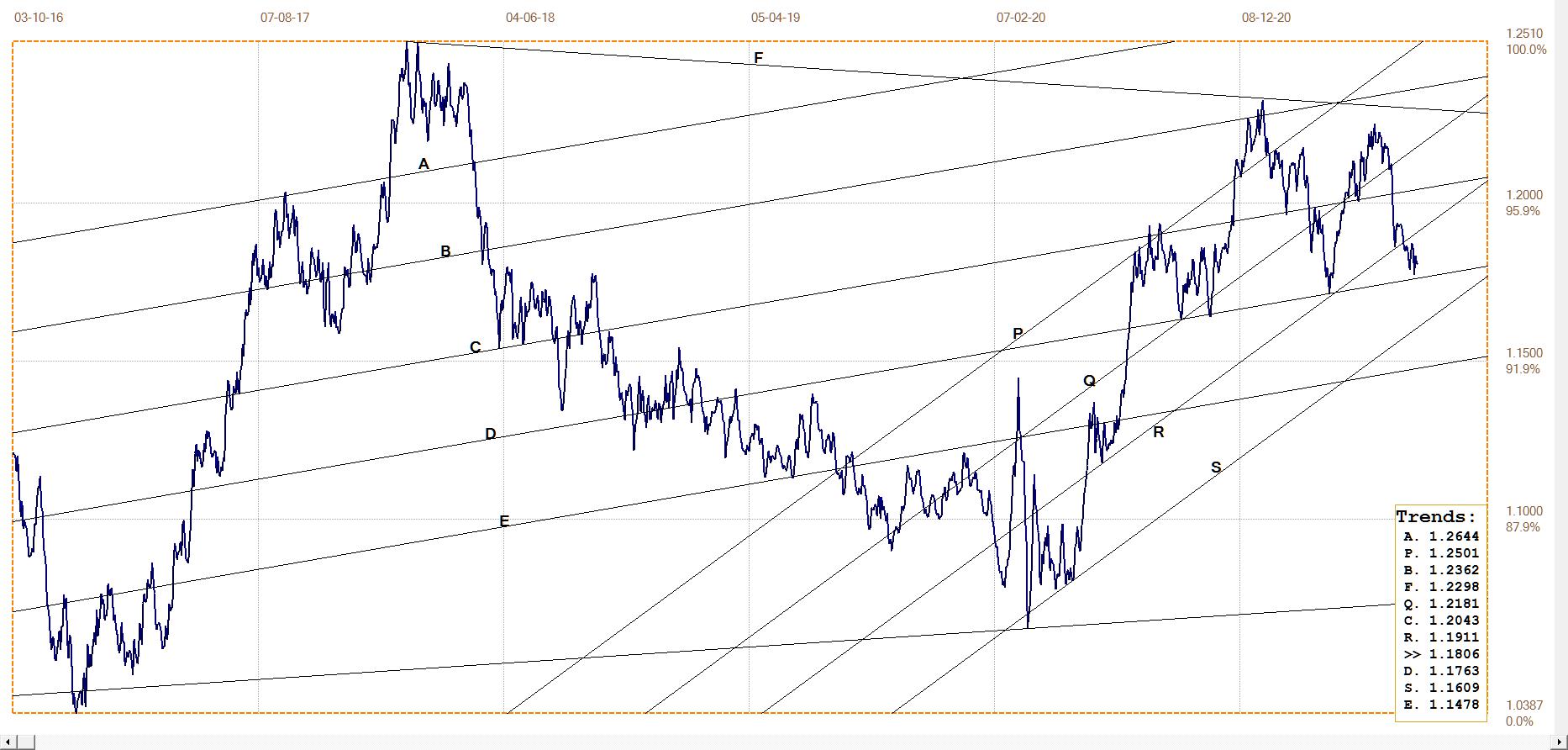

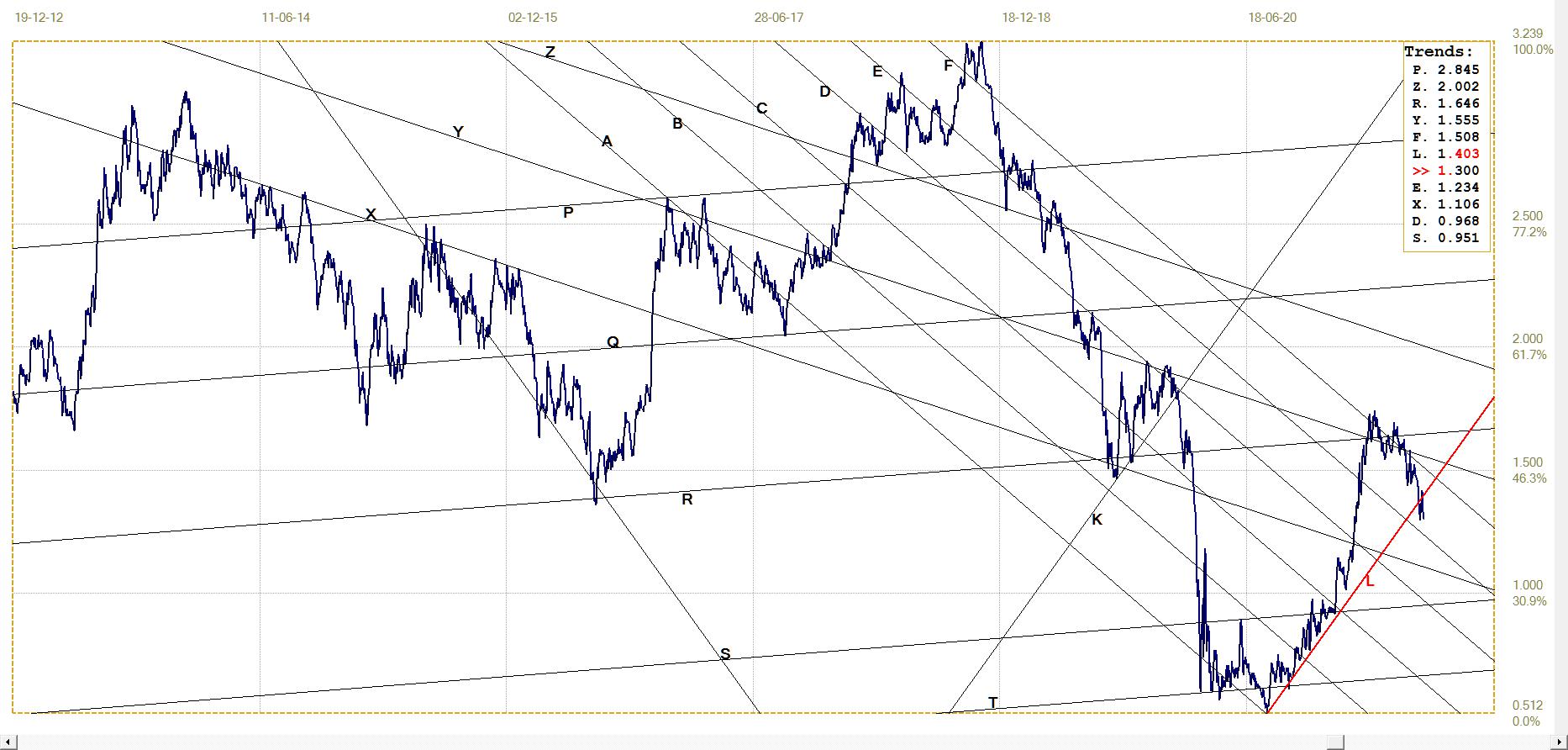

Euro–Dollar

Euro–dollar, last = $1.1806 (www.investing.com)

The break below bull channel PQR is short term bearish for the euro, provided that the support along line D continues to hold, as it has done on previous occasions. Even on a break below line D, the longer term outlook is still bullish; in this instance, as long as channel PQRS holds.

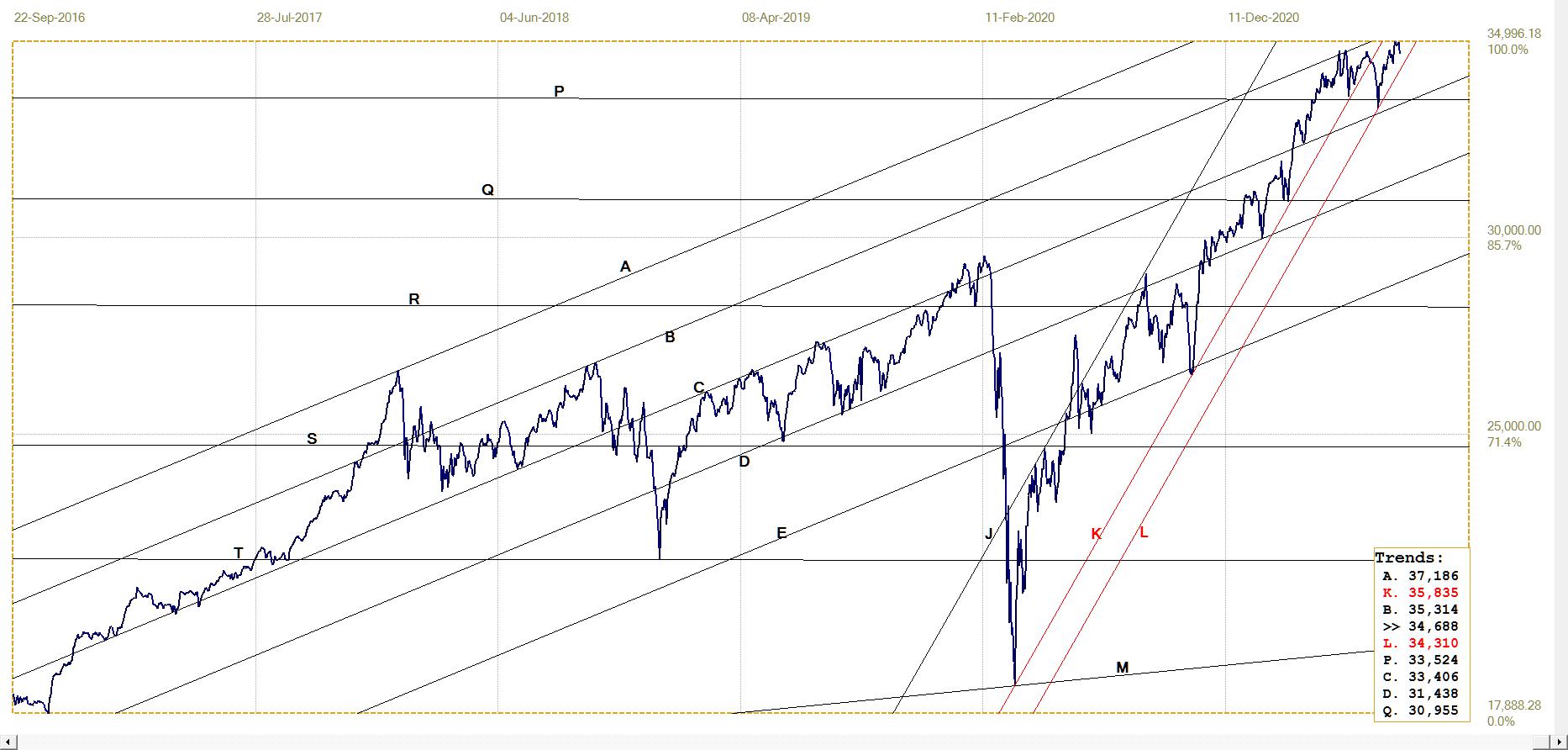

DJIA daily close

Last week the DJIA failed to join the S&P500 and the Nasdaq when they set new all-time highs in the course of the week. On Monday it came close to ending the trading day above 35 000 and tried again on the next three days, again without any success.

Then on Friday, the DJIA was under pressure for the whole day, to end not far above the day’s low, losing 299 points.

Expert comments from non-official quarters continue to predict a bear market, often using the term “crash” as an indication that Wall Street is ready to move lower with a BANG and not a whimper – drifting lower bit by bit in piecemeal fashion.

Given the sharp decline on Friday after several failed attempts to break above 35 000, this week looks to offer an interesting spectacle as the Bears try to repeat what they had achieved on Friday, while the usual bullish forces do all they can to stop them.

DJIA. last = 34687.85 (money.cnn.com)

Gold London PM fix – Dollars

Gold price – London PM fix, last = $1824.30 (www.kitco.com)

Last week the price of gold managed a London PM fix above $1800 and then held that break to the end of the week, slowly setting it higher through to Friday – which is a rare accomplishment. There has been a substantial increase in the OI since the end of June – increasing by almost 34 400 (7.5%) from 455 621 to nearly 490 000.

There is divided opinion about the potential effect of BASEL lll on the behaviour of the Big Banks and what effect this might have on the price of gold. The increase in the gold OI might imply that the bullish faction is putting its money where their mouth is. Assuming that there is no time pressure on the Banks to comply with BASEL lll – if the implementation of its critical features are not postponed – no fireworks are expected soon, even if better informed buyers of the gold contracts are later proven correct.

Euro–gold PM fix

The improvement in the dollar price of gold last week has had the euro price of the metal breaking above the descending resistance of line G. Firstly the recovery above line F and now the break higher also places a bullish bias on the dollar price of gold.

This mainly because this confirms that gold now has some inherent strength on which to build its advance.

Euro gold price – PM fix in Euro. Last = €1545.73 (www.kitco.com)

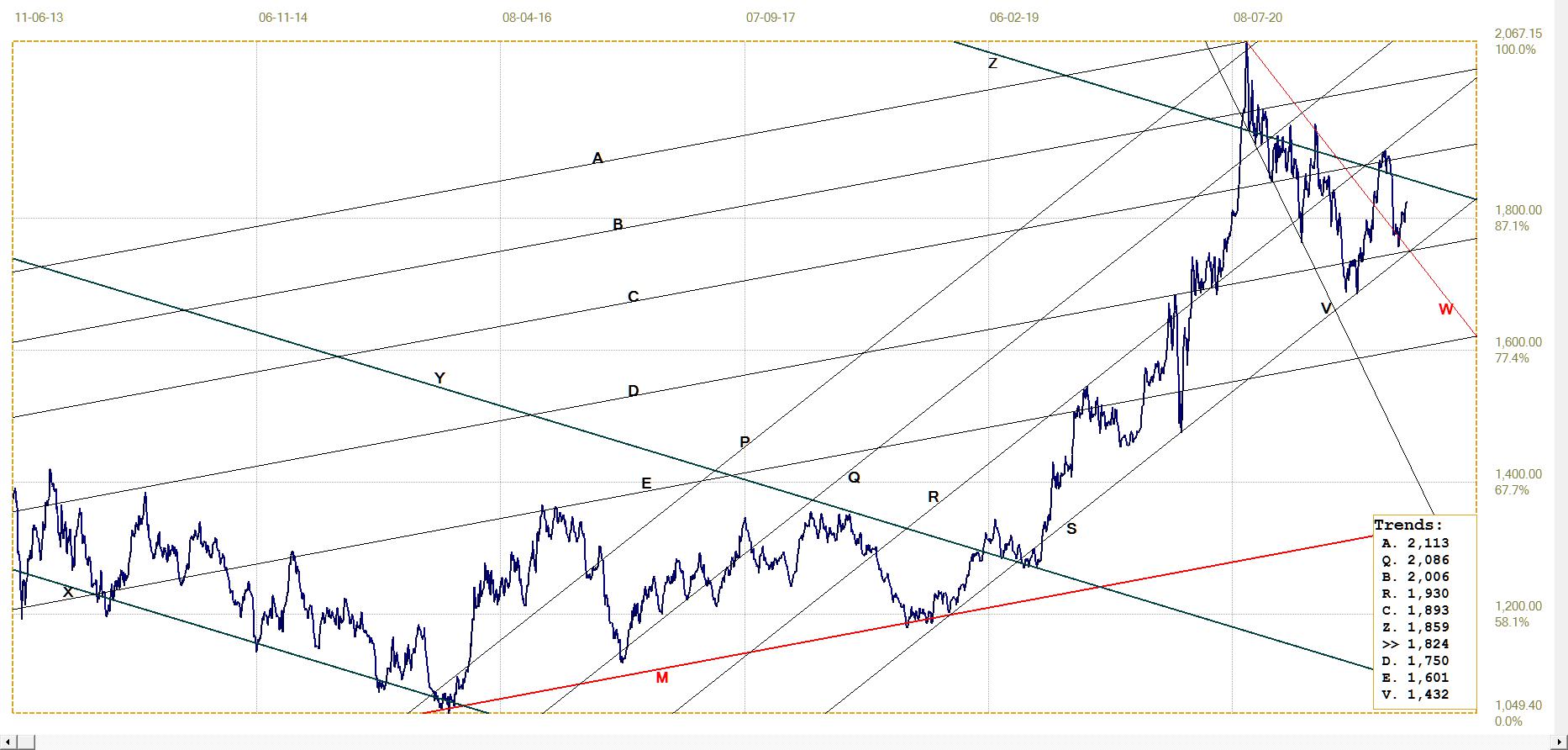

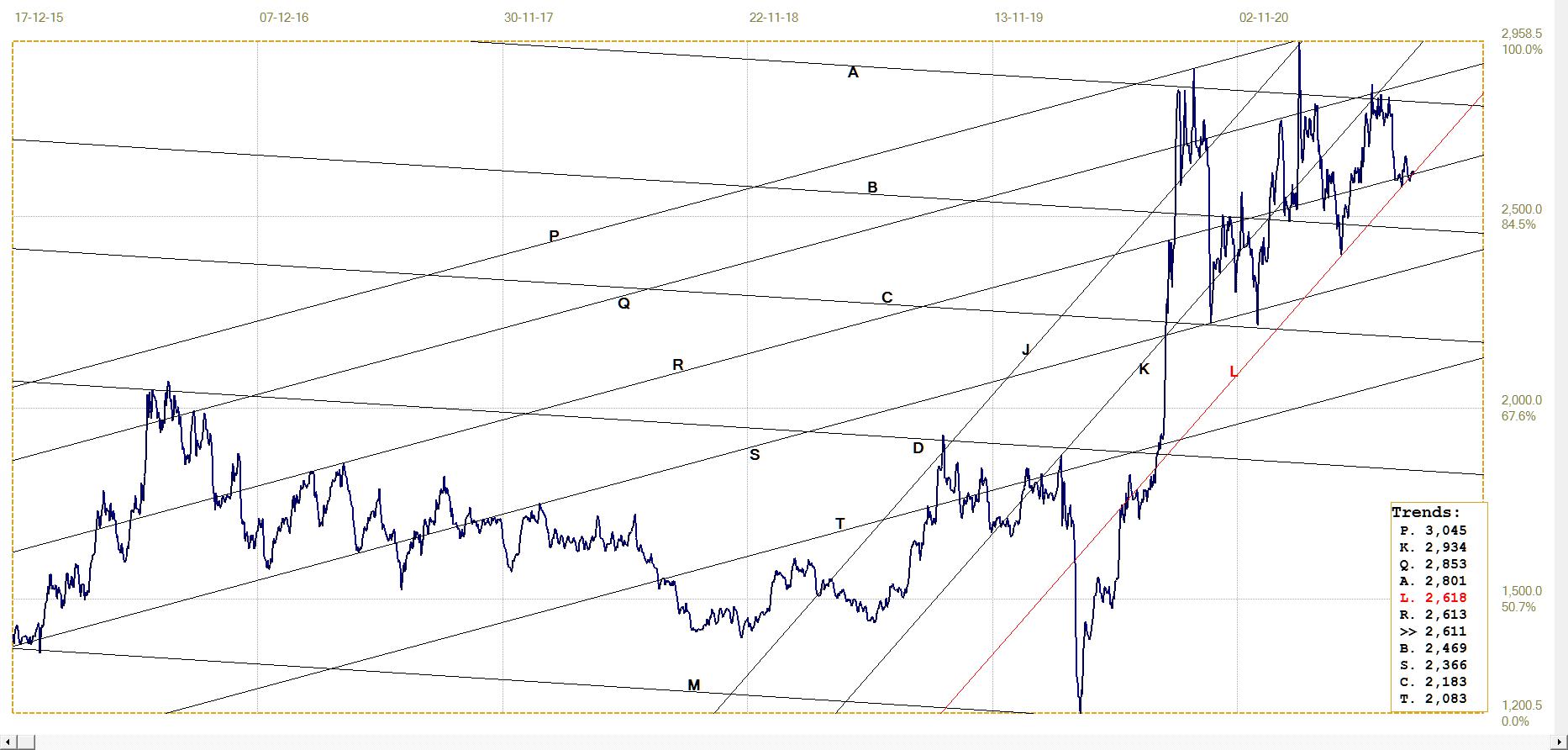

Silver Daily London Fix

It really does look as if silver is well aware of the support offered primarily by line L of the medium term bull channel JKL and also by line R of the shallower bull channel. It was on midsummer’s day, 21 June, when the silver London dropped below $26 for the first time since late April. This placed it right on line R, but was followed by a break to below the support to rest on the bottom of the bull channel. From there it bounced to hold above $26 until early in July, when it tested line L again – which held again and is still holding as the silver price creeps higher. Bullish outlook while the channel holds.

If demand for silver contracts at COMEX is trending lower, it will be ever more difficult to get the price that is generally accepted as “official” moving higher. Should the open market price build a sufficient premium over the fixed price to where it becomes really profitable for arbitrage for the large players, this may change. It does not seem as if the existing premiums for the metal are any cause of embarrassment for the Cartel or a cause of concern for the CFTC.

Silver daily London fix, last = $26.105 (www.kitco.com)

U.S. 10–year Treasury Note

The break below bear channel KL, presumably because the market believes inflation will be transitory, appears as if it had briefly developed second thoughts, with the yield breaking back into the channel. It again broke lower to form a double bottom.

What happens this week at the double bottom and perhaps at line L should show whether the market thinks the new higher CPI is merely another flash in the pan or confirmation of higher inflation to come.

U.S. 10–year Treasury note, last = 1.300% (www.investing.com )

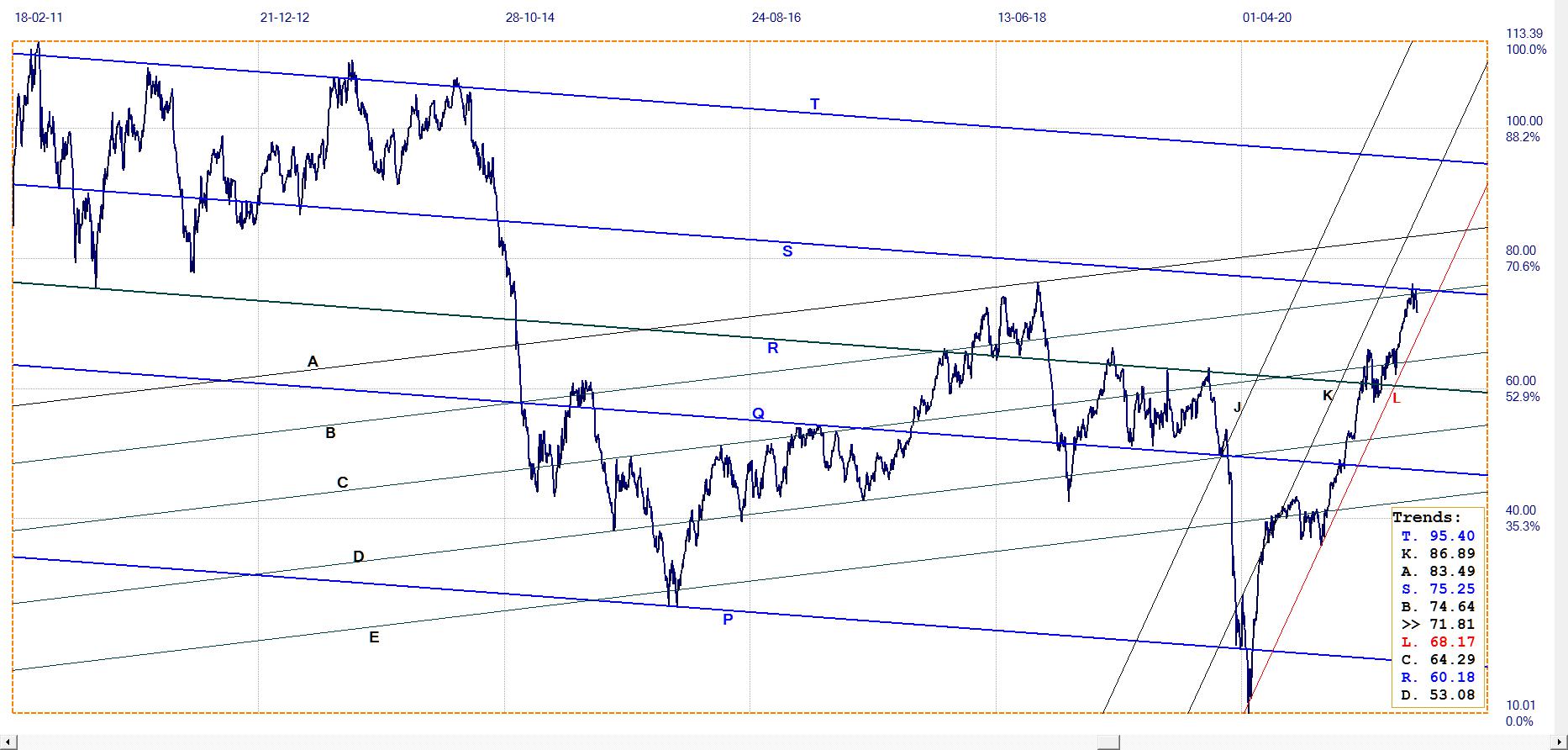

West Texas Intermediate crude. Daily close

WTI crude – Daily close, last = $71.81 (www.investing.com )

On Friday, the price of crude was at a new low of the current consolidation below lines S and B. This could be either reduced demand, which could put a lie to the news that the economy is growing and consumers are buying, or it could be a similar belief to what could be at play in the bond market, namely that the relatively small increase in the CPI over the previous month implies that inflation is due to be lower next month and back to the normal 1-2% quite soon.

*********