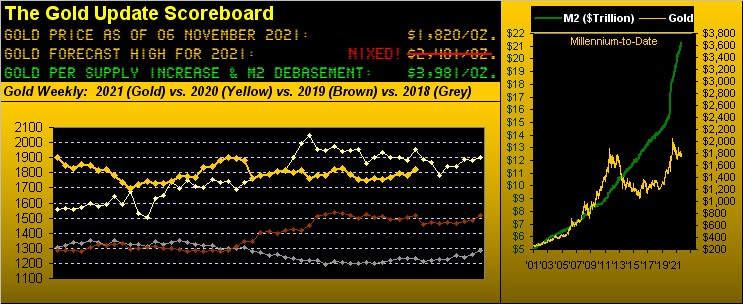

Gold FINALLY Breaks Free Amidst S&P INSANITY

Gold, after 18 weeks of being stuck in a maniacal Short trend without price really going anywhere, FINALLY broke the bonds of the M word crowd by flipping to Long -- but not without a mid-week scare: more later on that affair.

But we begin by assessing the stark INSANITY besetting the parabolic performance of the S&P 500, +25% year-to-date. It settled yesterday (Friday) at 4698 (reaching 4718 intra-day), a record closing high for the seventh consecutive session. Such phenomenon has occurred but five other times in the past 41 years!

So here's a multiple choice question for you: Ready?

Across all those years (i.e. from 1980-to-date), what is the longest stretch of time between all-time highs for the S&P 500?

■ a) eight months

■ b) just over three years

■ c) slightly less than six years

■ d) all of the above (for you WestPalmBeachers down there)

■ e) none of the above

If having answered "e)", you are correct: the longest stint was almost seven-and-one-quarter years from 24 March 2000 through the DotComBomb up to 13 Jul 2007. 'Twas the complete antithesis of the current paradigm of an all-time high every single trading day.

But wait, there's more: those of you who were with us way back in the days at AvidTrader may recall our technically having "mild", "moderate" and "extreme" readings of both oversold and overbought conditions for the S&P. Well, get a load of this: yesterday was the S&P's 12th consecutive day with an "extremely overbought" reading. During these 41 years, that has only happened once before, 36 years ago in 1985. And the price/earnings ratio then was a respectable 10.5x: today 'tis five times that much at 54.4x (!!!) easily more than double the S&P's lifetime median P/E (since 1957) of 20.4x.

And still more: Every time the S&P moves from one 100-point milestone to the next, 'tis a FinMedia "big headline deal", albeit the percentage increase comparably narrows. Nonetheless, trading gains and losses are measured by the point, not the percentage. And from 1980-to-date, the S&P has gone from 100 to now 4700, (i.e. through 46 milestones. Upon having just achieved the 4600 level on 29 October, the average number of trading days over these past 41 years to reach each 100-point milestone is 236 (just about a year's worth). But now from 4600-4700 took just five days! Cue John McEnroe: "You canNOT be SERious!!"

'Course, every trend reaches a bend, if not its end. And whilst the market is never wrong, something will the S&P upend. You regular readers already know the "earnings are not there" to support even one-half the S&P's current level. Moreover, 'tis said when the Federal Open Market Committee does nudge up its Bank's Funds rate, 'twill be "Game Over" for the S&P, (something of which the Fed is very fearful).

"But mmb, even a rise from just 0.25% to only 0.50% maintains a really low rate..."

Nominally still low, yes Squire: but upon it occurring, the Fed shall have doubled the cost for every bank that comes to the borrowing window, from which one can then ask banking clientele: "How's that variable rate loan workin' out for ya?" And thus falleth the first domino. And the S&P. Have a great day.

Gold had a great day yesterday in settling out the week at 1820. But as noted, 'twas not before a mid-week scare. With Gold wallowing on "The Taper of Paper" Wednesday -- down at 1758 (a three-week low) -- the tried-and-true, widely followed daily moving average convergence divergence (MACD) crossed to negative. Such previous 11 negative crossings had averaged downside follow-through of 86 points. Thus within that technical vacuum, another run sub-1700 was placed on Gold's table. What instead followed was a one-day whipsaw, Gold's MACD finishing the week with a positive cross, and even better, the weekly parabolic Short trend FINALLY being bust per the first Gold-encircled dot in our weekly bars graphic:

FINALLY too Gold had its first Friday in five of not being flogged ostensibly by the M word crowd. Should they thus have left the building, in concert with both the daily MACD back on the positive side and the weekly parabolic again Long, the door is open for Gold to glide up into the 1900s toward concluding 2021.

As for the five primary BEGOS Markets, here are their respective percentage tracks from one month ago (21 trading days)-to-date, the S&P having swiftly replaced Oil as the leader of the pack. Of more import, note the rightmost bounce for Gold and the Bond. Why are those two stalwart safe havens suddenly getting the bid? (See our opening commentary on S&P INSANITY):

Meanwhile as we waltz into the waning two weeks of Q3 Earnings Season, of the S&P's 505 constituents, 426 have reported (450 is typically the total within the seasonal calendar), of which 340 (80%) have bettered their bottom lines from Q3 of a year ago when much of the world purportedly was "shut down". Thus such significant improvement was expected: "They better have bettered!"

Yet as noted, our "live" P/E is at present 54.4x. Thus to bring earnings up to snuff such as to reduce the P/E to its lifetime median of 20.4x, bottom lines need increase by 167%: but the median year-over-year increase (for those 396 constituents with positive earnings from both a year ago and now) is only 19%. Thus for those of you scoring at home, a 19% increase is nowhere near the "requisite" 167%. "Look Ma! Still no earnings!" (Crash).

Still earning to grasp good grace is the track of the Economic Barometer, which bopped up a bit on the week's headline numbers. To be sure, October's Payrolls improved with a decline in the Unemployment Rate and a jump in the Institute for Supply Management's Services Index. But with a return of folks to the workplace (excluding those who've post-COVID decided they don't need to work) came a plunge in Q3's Productivity combined with a spike in Unit Labor Costs. As well, October's growth in Hourly Earnings slowed and the Average Workweek shortened, such combination suggesting temporary jobs materially lifted the overall Payrolls number. Also less highlighted was September's slowing in Factory Orders, shrinkage in Construction Spending, and the largest Trade Deficit recorded in the Baro's 24-year history. Here's the whole picture from one year ago-to-date with the S&P standing up straight:

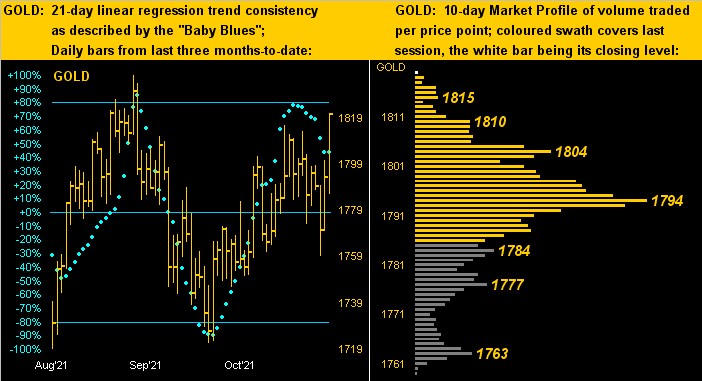

To our proprietary Gold technicals we go, the two-panel graphic featuring price's daily bars from three months ago-to-date on the left with the 10-day Market Profile on the right. And note the "Baby Blues" of linear regression trend consistency being abruptly stopped in their downward path thanks to Friday's "super-bar" -- Gold's best intra-day low-to-high run in nearly four weeks -- and the highest closing price since 04 September. As well in the Profile, price sits atop the entire stack, which you'll recall for the prior two weeks was at best a congestive mess. But to quote Inspecteur Clouseau, "Not any moooure...":

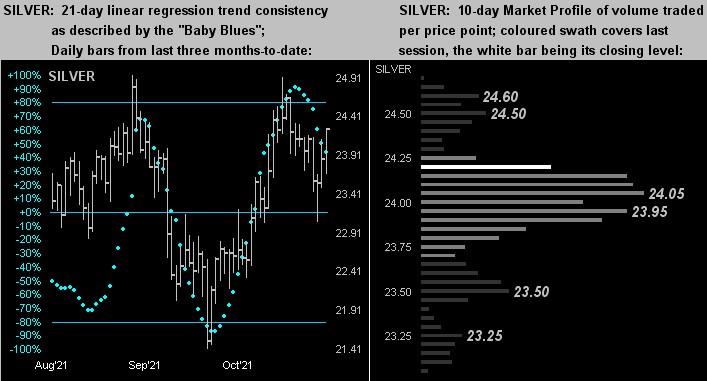

As for Silver, she's not as yet generating as much comparable excitement. At left, her "Baby Blues" continue to slip even as price gained ground into week's end. At right, the price of 24 clearly is her near-term "line in the sand". Still, our concern a week ago of her falling into the low 22s has somewhat abated, albeit the daily parabolic trend remains Short; however a quick move to 24.700 ought nix that condition. "C'mon, Sister Silver!":

So there it all is. We see Gold as poised to FINALLY move higher toward year-end, (barring a resurgence of the M word crowd). And we see the S&P as poised for its off-the-edge-of-the-Bell-curve INSANITY to cease, (barring an economic erosion that instead furthers the flow of free dough). After all, bad is good, just as Gold is always good.

In that spirit to conclude for this week, here are three good bits from a few of the smartest (so we're told) people in the world:

Betsey "With an e" Stevenson says with respect to folks not returning to the workforce post-COVID that "...It’s like the whole country is in some kind of union renegotiation..." That is True Blue Michigan-speak right there. But think about it: when you've got a) the upper labor hand, and b) the aforementioned free dough that you popped into the stock market to thus gain some 38% since the economy first shutdown, why work, eh? Besides, the feeling of marked-to-market wealth is a beautiful thing.

Elon "Spacey" Musk now notes that Tesla has not contracted with Hertz to sell 100,000 four-wheel batteries. Recall when that deal first was announced, the price of TSLA went up many times more than the additional incremental return of the transaction. But hardly has it since retracted. 'Course, the company's Q3 earnings were "fantastic", in turn nicely bringing down the stock's P/E to just now 345.8x. And comparably as you already know, the only other two S&P 500 constituents classified as being in the sub-industry category of "Automobile Manufacturers" are Ford (P/E now 26.1x) and General Motors (P/E now 7.7x). But a shiny object that rolls, too, is a beautiful thing.

Peter "Techie" Thiel has just opined that the soaring price of bits**t is indicative of inflation being at a "crisis moment" for the economy. 'Tis not ours to question this notion; rather 'tis beyond our pay grade to understand it. What we do understand is that THE time-tested (understatement) indicator and mitigator of inflation -- i.e. Gold -- is priced at such an attractively low level versus where it "ought" be (i.e. 3981 per our opening graphic's decreed,) that never again such a beautiful opportunity shall we see!

Mark Mead Baillie has had an extensive business career beginning in banking and financial services for two years with Banque Nationale de Paris to corporate research for three years at Barclays Bank and then for six years as an analyst and corporate lender with Société Générale.

For the last 22 years he has expanded his financial expertise by creating his own financial services company, de Meadville International, which comprehensively follows his BEGOS complex of markets (Bond/Euro/Gold/Oil/S&P) and the trading of the futures therein. He is recognized within the financial community of demonstrating creative technical skills that surpass industry standards toward making highly informed market assessments and his work is featured in Merrill Lynch Wealth Management client presentations. He has adapted such skills into becoming the popular author each week of the prolific “The Gold Update” and is known in the financial website community as “mmb” and “deMeadville”.

Mr. Baillie holds a BS in Business from the University of Southern California and an MBA in Finance from Golden Gate University.