Gold Forecast: How Many Months Are Left Until Gold’s Fundamental Landslide?

While gold prices remain elevated and investors continue to ignore the implications of the Fed’s rate hike cycle, a reality check should emerge sooner rather than later. For example, Bank of America’s latest Global Fund Manager Survey shows that institutional investors don’t expect the Fed to turn dovish anytime soon.

Please see below:

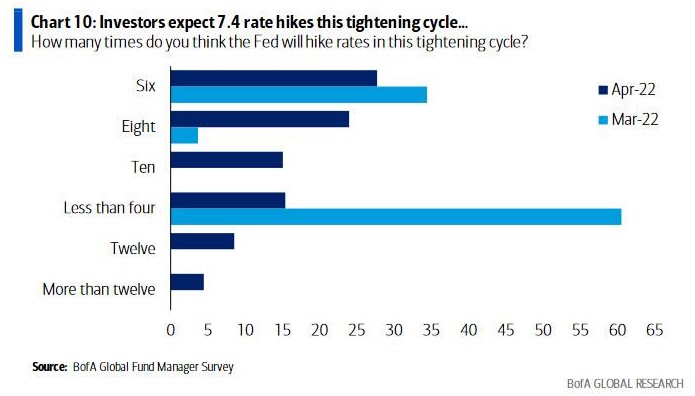

To explain, the consensus expects six rate hikes in the coming months. However, while roughly 5% of respondents expected eight rate hikes in March, that figure increased to roughly 25% in April. As a result, institutional investors are slowly coming around to the hawkish realities that I warned about throughout 2021.

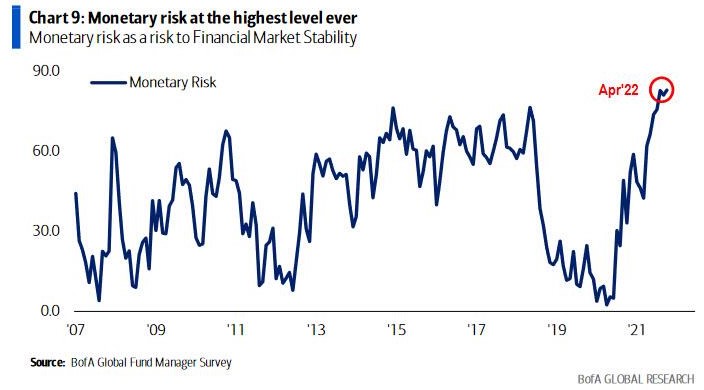

Furthermore, institutional investors’ assessment of monetary policy risk hit an all-time high in April.

Please see below:

Denial

However, old habits die hard, and while institutional investors realize what should materialize amid the Fed’s war on inflation, their positioning contrasts with the hawkish realities. As a result, the relative day-to-day calm contrasts with the crumbling house of cards.

Please see below:

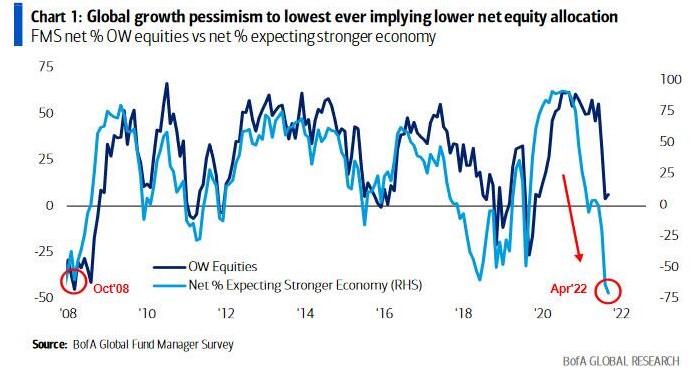

To explain, the dark blue line above tracks the net percentage of respondents overweight equities, while the light blue line above tracks the net percentage of respondents expecting a stronger economy. If you analyze the right side of the chart, you can see that the light blue line is on par with the global financial crisis (GFC) lows. Despite that, though, institutional investors refuse to sell their stocks.

Thus, while fund managers believe that a material tightening of financial conditions will commence, the ‘buy the dip’ mentality is hard to break. However, with reality likely to force institutional investors to recalibrate their positions, the prospective negativity should have a profound impact on the PMs.

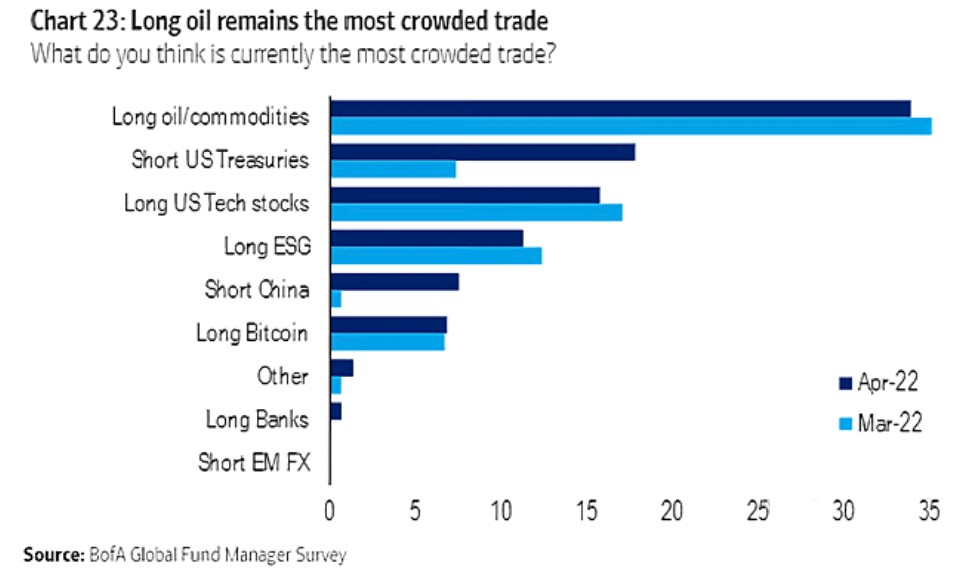

To that point, long oil/commodities are still the most crowded trades on Wall Street. Moreover, the idea that higher interest rates won’t impact commodity demand lacks credibility. In fact, slowing the U.S. economy should hurt commodities more than most sectors. As such, when the over-optimism reverses, the PMs should suffer substantial declines.

For more context, I wrote on Apr. 14

With Brainard and Waller telling you that their goal is to create a bullish environment for the USD Index and the U.S. 10-Year real yield, the PMs have fought this battle before and lost this battle before.

I wrote on Apr. 6:

Please remember that the Fed needs to slow the U.S. economy to calm inflation, and rising asset prices are mutually exclusive to this goal. Therefore, officials should keep hammering the financial markets until investors finally get the message.

Moreover, with the Fed in inflation-fighting mode and reformed doves warning that the U.S. economy “could teeter” as the drama unfolds, the reality is that there is no easy solution to the Fed’s problem. To calm inflation, it has to kill demand. And as that occurs, investors should suffer a severe crisis of confidence.

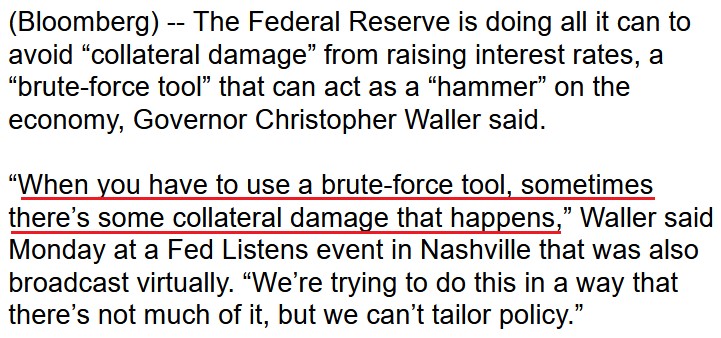

To that point, Fed officials aren’t even pretending anymore. Waller said on Apr 13:

“All we can do is kind of push down demand for these products and take some pressure off the prices that people have to pay for these products. We can’t produce more wheat, we can’t produce more semiconductors, but we can affect the demand for these products in a way that puts downward pressure and takes some pressure off of inflation.”

Likewise, Waller was even more realistic when he spoke on Apr. 11: He said:

“With housing, can we cool off demand for housing without tanking the construction industry? Can we cool down labor demand without causing employment to fall? That’s the tricky road that we’re on.”

As a result, while Fed officials understand how difficult it will be to normalize inflation, investors remain in la-la land. However, when the “collateral damage” eventually unfolds, the shift in sentiment should result in the profound re-pricing of several financial assets.

Please see below:

Source: Bloomberg

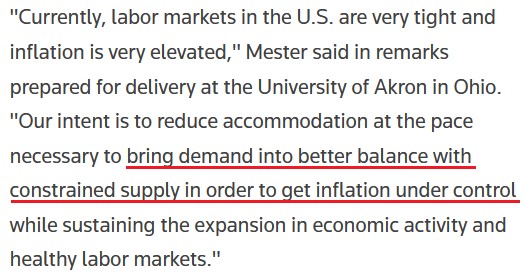

Building on that theme, Fed officials continue to use the d-word when describing how they will tame inflation. Speaking on Apr. 14, Cleveland Fed President Loretta Mester said: “It’s not really a tradeoff right now, it’s really an imperative that we take the action, that we are committed at the FOMC to do that, to get inflation on a downward trajectory.”

As a result:

Source: Reuters

Likewise, Philadelphia Fed President Patrick Harker said on Apr. 14 that the central bank will deliver "a series of deliberate, methodical hikes" to curb "far too high" inflation.

Please see below:

Source: Reuters

As a result, while commodities remain the belle of the ball, the reality is that the Fed has to reduce demand. When the light bulb goes off that demand is dropping while prices remain sky high, commodities’ history of epic rallies and drawdowns will likely repeat.

To that point, as long as inflation remains problematic, the prospect of a dovish 180 by the Fed is slim to none, and with the data still coming in hot, investors remain unprepared for the medium-term readjustments.

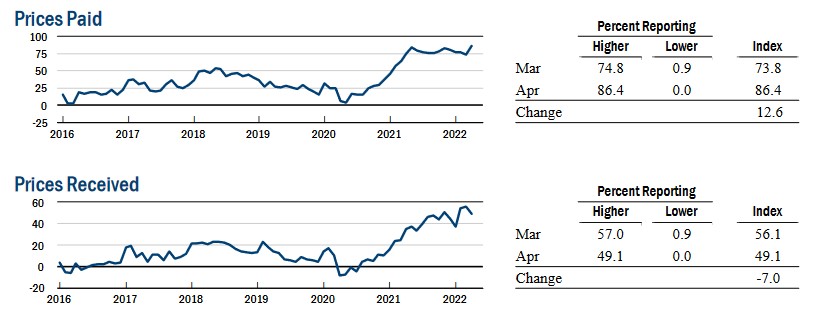

For example, the New York Fed released its Empire State Manufacturing Survey on Apr. 15. The report revealed:

“The prices paid index climbed thirteen points to 86.4, a record high, and the prices received index retreated seven points from last month’s record high, signaling ongoing substantial increases in both input prices and selling prices.”

Please see below:

Source: New York Fed

In addition, the University of Michigan released its Consumer Sentiment Index on Apr. 14. Chief Economist Richard Curtin said:

“Consumer Sentiment jumped by a surprising 10.6% in early April, although it remained below January's reading and lower than in any prior month in the past decade. Nearly the entire gain was in the Expectations Index, which posted a monthly gain of 18.0%, including a leap of 29.4% in the year-ahead outlook for the economy and a 17.2% jump in personal financial expectations. A strong labor market bolstered wage expectations among consumers under age 45 to 5.3%, the largest expected gain in more than three decades, since April 1990.”

For context, wage growth of 5.3% is mutually exclusive with the Fed’s inflation goal. Moreover, when Powell and his crew begin their crusade to kill demand, consumers will likely suffer the same come-to-Jesus moment as investors.

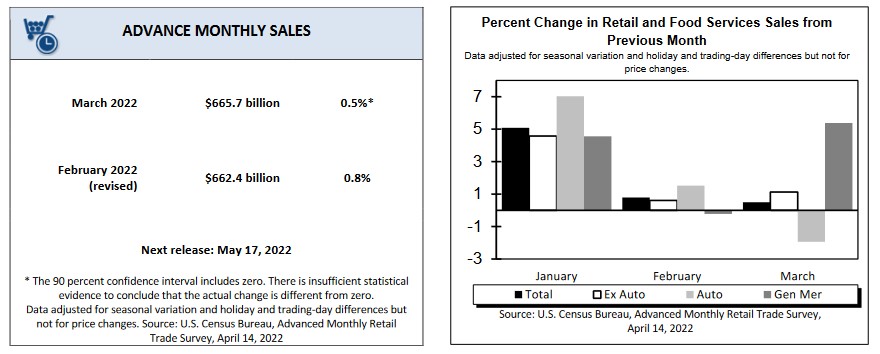

Finally, the U.S. Census Bureau released its U.S. retail sales report on Apr. 14., and with the metric hitting a new all-time high of ~$666 billion in March, consumers’ spending spree remains alive and well. As such, the Fed still has plenty of work to do to curb demand and inflation.

The bottom line? While the PMs remain in momentum-driven upswings, their medium-term fundamentals continue to deteriorate. With real yields rising, the USD Index north of 100 and the Fed in inflation-fighting mode, the officials’ war against demand and inflation should upend the PMs in the coming months. As a result, while gold, silver, and mining stocks’ recent price action may seem bullish on the surface, there are plenty of material risks on the horizon.

In conclusion, the PMs were mixed on Apr. 18, as financial markets continued to assess macroeconomic developments. Moreover, while the Fed keeps hammering home its message, investors are still far from acknowledging reality. Thus, while the timing remains uncertain, medium-term enlightenment should result in a profound shift in sentiment.

Summary

Despite the ongoing Russian invasion of Ukraine, and despite gold being the traditional safe haven in times of turmoil, the overall outlook for the precious metals sector remains bearish for the next few months, and the medium-term outlook for the yellow metal remains pessimistic.

Since it seems that the PMs are starting another short-term move lower more than it seems that they are continuing their bigger decline, I think that junior miners would be likely to (at least initially) decline more than silver.

Since neither the USD Index nor real interest rates are likely to stop rising anytime soon, the gold price is likely to fall sooner or later. Given the analogy to 2012 in gold, silver, and mining stocks, “sooner” is the more likely outcome.

As silver often moves in close relation to the yellow metal, when gold falls, silver is likely to decline as well – it has probably already started its slide. The times when gold is continuously trading well above the 2011 highs will likely come, but they are unlikely to be seen without being preceded by a sharp drop first.

Thank you for reading our free analysis today. Please note that it is just a small fraction of today’s all-encompassing Gold & Silver Trading Alert. The latter includes multiple premium details such as the outline of our trading strategy as gold moves lower.

If you’d like to read those premium details, we have good news for you. As soon as you sign up for our free gold newsletter, you’ll get a free 7-day no-obligation trial access to our premium Gold & Silver Trading Alerts. It’s really free – sign up today.

Thank you.

Przemyslaw Radomski, CFA

Founder, Editor-in-chief

Sunshine Profits - Effective Investments through Diligence and Care

* * * * *

All essays, research and information found above represent analyses and opinions of Przemyslaw Radomski, CFA and Sunshine Profits' associates only. As such, it may prove wrong and be subject to change without notice. Opinions and analyses are based on data available to authors of respective essays at the time of writing. Although the information provided above is based on careful research and sources that are deemed to be accurate, Przemyslaw Radomski, CFA and his associates do not guarantee the accuracy or thoroughness of the data or information reported. The opinions published above are neither an offer nor a recommendation to purchase or sell any securities. Mr. Radomski is not a Registered Securities Advisor. By reading Przemyslaw Radomski's, CFA reports you fully agree that he will not be held responsible or liable for any decisions you make regarding any information provided in these reports. Investing, trading and speculation in any financial markets may involve high risk of loss. Przemyslaw Radomski, CFA, Sunshine Profits' employees and affiliates as well as members of their families may have a short or long position in any securities, including those mentioned in any of the reports or essays, and may make additional purchases and/or sales of those securities without notice.

*********

Przemyslaw Radomski, CFA, is the founder, owner and the main editor of SunshineProfits.com. You can reach Przemyslaw at: http://www.sunshineprofits.com/help/contact-us/.

Przemyslaw Radomski, CFA, is the founder, owner and the main editor of SunshineProfits.com. You can reach Przemyslaw at: http://www.sunshineprofits.com/help/contact-us/.