Gold Forecast: The Yellow Metal’s Performance And Current Interest Rates

Every gold investor knows about the inverse link between real interest rates and gold. One of the key determinants of real interest rates are nominal interest rates. Within today’s article, we’ll examine the Fed monetary policy turns – just how did they affect the broad debt markets? The long-term interest rates are flashing a valuable signal for us, gold investors.

As the Fed turned dovish this year, not only did the short-term interest rates move down - the long- and very-long-term ones also declined. Why would this be the case? After all, the long-term rates are set by market forces, not through Fed's direct decision... More importantly, though, why should you, the precious metals investor, care? What kind of signal does it send to the gold market for the following months and years?

It's not that the Fed directly controls the long-term rates that is the issue here - it doesn't.

The long-term interest rates are based on supply and demand, which are in turn based on market expectations. After all, markets are forward looking.

And what does the Fed provide in addition to interest rate decisions? Forward guidance.

Year after year, public debts have been increasing across the world's most advanced economies, and it's becoming increasingly obvious that this debt cannot be repaid using regular revenue of the official sector (taxes). The debt can be repudiated but that's an unthinkable proposition - take a look at how Greece's efforts turned out. Realistically, the debt will need to be inflated away... Or maybe it won't have to be. After all, in the scenario where long-term interest rates go below zero, the debt is no longer ballooning due to interest. Either way, the interest rates are likely to be lower in the long run based on the above. This is the core of financial repression - artificially low rates. But that's just one of the reasons.

The direct comments from the Fed clearly support the above - the rates are getting lower and that's happening even without incoming data that would support a rate cut. All the talk about the Fed being data-driven didn't amount to much after Trump started openly criticizing Fed and demanding rates be cut. He delivered the "trade risk" which served as justification of a rate cut. That's not an official statistic the Fed was supposed to follow - it's smoke and mirrors that helps to keep rates in a long-term downtrend. Then, it's no wonder that forward-looking investors expect rates to be lower in the following years, not only months. What does it imply for gold? In the very long term it's very bullish, because when the risk-free rate goes to (or below) zero, an asset that doesn't yield any interest becomes much more desirable. In normal circumstances, it's better to have an interest-yielding asset than one without. But when the long-term interest rates go below zero and investors can't earn money through bonds, gold will be a much better alternative. Especially when it outshines inflation.

The key thing to keep in mind is that the above is a long-term fundamental factor. It doesn't tell us where the market will move either in the short term or in the medium term. It's practically a factor of zero importance for day trading.

The markets are forward looking, which means that they are already discounting the above taking place and they aim to front run the obvious consequences even before they occur. The markets discount more than news and fundamentals, though. They also discount investors and traders' emotions for people tend to get ahead of themselves in terms of expectations and reactions to news. Consequently, the market could get ahead of itself and then decline regardless of the fundamental situation being positive. Or it might be in a medium-term downtrend and forced to move against it based on series of unexpected events. How do we know what price movement is real and which one is fake? The truth is that one can never be 100% certain with regard to any price movement. However, there is a way to detect what is likely and what's not. That happens by comparing the current situation to similar cases in the past and how consistently the follow-up actions unfolded. That's more or less what technical analysis is all about. There are more sophisticated techniques, but the overall general rule is as simple as the above.

So, without further ado, let's take a look at what the very long-term (30-year) interest rates are currently doing and how similar cases impacted the gold market in the past.

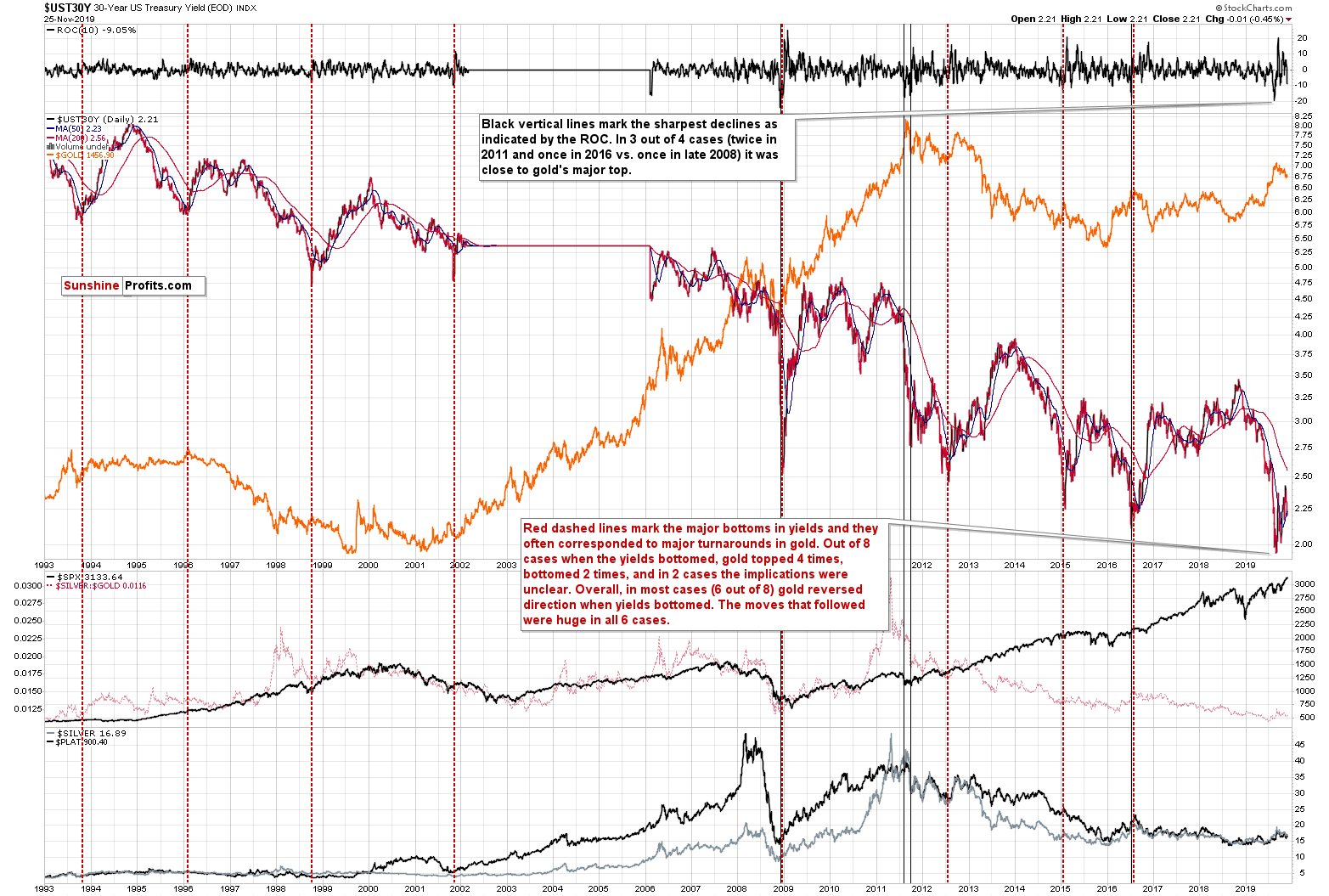

In short, we recently saw a huge drop in the long-term rates. It was neither the first one, nor the biggest one though. We saw similar developments several times in the previous years, and the 2008 drop was the most significant one.

Long-term rates are definitely in a long-term downtrend, but they are not declining in a straight line. There are big slides, just like the one that we saw recently, and there are upswings that take up to- or even over a year. The rates moved to new lows recently and then rallied back above the previous lows. This suggests that the short- or even medium-term bottom in the rates is in. Moreover, that's exactly what happened in 2015 and 2016, and gold topped at both lows in the rates. Of course, these are not the only cases when the rates bottomed, so let's check what happened in all previous cases since 1993.

Not taking into account the August top, out of 8 cases when the 30-year Treasury yields bottomed, gold topped 4 times, it bottomed twice and in the 2 remaining cases, the implications were unclear. In other words, gold rallied in only 25% of cases (in 2001 and 2013), but in both cases the exact bottom in gold took place along with the bottom in the rates. This means that in both cases when the implications were bullish, gold declined beforehand. This was definitely not the case recently. Gold topped along with the bottom in the rates in August, which makes it similar to the 4 cases when the slide and bottom in the rates were actually great shorting opportunities for gold traders.

This means that while the overall trend lower in rates is positive for gold for the following years, the very recent slide in rates does not have bullish implications for the short or even medium term. Whatever bullish action was likely to happen based on it, is likely already behind us.

Please take a look at what happened with the long-term interest rates at the 1996 top. This is particularly important, because based on what's happening in the USD Index, the current situation is just like what we saw in the mid-90s. The long-term interest rates formed a short-term bottom, then they rallied for a few months, consolidated and then declined once again for more than a year. And you know what happened in gold? Gold declined for practically the entire time. It even declined after the rates bottomed in 1998. That's exactly what we might see in the following months.

The USD Index is likely to soar next year (quite likely also this year) and while the rates might move lower in the long run, they are likely to bounce in the short term. And gold? It has likely topped just as it did in early 1996, and is now starting a major decline even though it’s likely to move higher in the next several days.

Summary

Summing up, the outlook for the precious metals sector remains very bearish for the following months due to several factors - and our point today is that the situation in the long-term interest rates does not prevent gold from declining. Because investors are forward-looking, what was likely to happen based on the decline in the long-term rates, has likely already happened and is not a factor due to which gold would move higher from here. To be honest, we do expect gold to move a bit higher in the next several days, but it’s likely to be just a counter-trend rally within a huge downswing.

In other words, the following months are not likely to be pleasant times for anyone who refuses to jump on the bullish bandwagon just because prices moved higher in the previous months. But what’s profitable is rarely the thing that feels good initially. Forecasting gold’s rally without a bigger decline first is likely to be misleading. There will most likely be times when gold is trading well above the 2011 highs, but they are unlikely to be seen without being preceded by a sharp drop first.

Naturally, the above is up-to-date at the moment of publishing and the situation may – and is likely to – change in the future. If you’d like to receive follow-ups to the above analysis, we invite you to sign up to our gold newsletter. You’ll receive our articles for free and if you don’t like them, you can unsubscribe in just a few seconds. Sign up today.

Przemyslaw Radomski, CFA

Editor-in-chief, Gold & Silver Fund Manager

Sunshine Profits - Effective Investments through Diligence and Care

* * * * *

All essays, research and information found above represent analyses and opinions of Przemyslaw Radomski, CFA and Sunshine Profits' associates only. As such, it may prove wrong and be a subject to change without notice. Opinions and analyses were based on data available to authors of respective essays at the time of writing. Although the information provided above is based on careful research and sources that are believed to be accurate, Przemyslaw Radomski, CFA and his associates do not guarantee the accuracy or thoroughness of the data or information reported. The opinions published above are neither an offer nor a recommendation to purchase or sell any securities. Mr. Radomski is not a Registered Securities Advisor. By reading Przemyslaw Radomski's, CFA reports you fully agree that he will not be held responsible or liable for any decisions you make regarding any information provided in these reports. Investing, trading and speculation in any financial markets may involve high risk of loss. Przemyslaw Radomski, CFA, Sunshine Profits' employees and affiliates as well as members of their families may have a short or long position in any securities, including those mentioned in any of the reports or essays, and may make additional purchases and/or sales of those securities without notice.

Przemyslaw Radomski, CFA, is the founder, owner and the main editor of SunshineProfits.com. You can reach Przemyslaw at: http://www.sunshineprofits.com/help/contact-us/.

Przemyslaw Radomski, CFA, is the founder, owner and the main editor of SunshineProfits.com. You can reach Przemyslaw at: http://www.sunshineprofits.com/help/contact-us/.