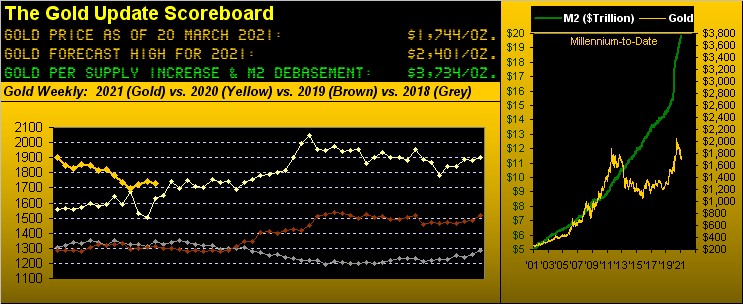

Gold From On Go To Narrow

"But first we begin with Breaking News: The S&P 500 is at a record-closing high following the largest drop in Personal Spending in nearly a year..."

So it hasn't crashed, yet...

In the meantime, 'twas but a week ago we penned "Gold on the Go", (replete in reviewing Moriarty's "Crow"); but since then Gold has gone notably narrow in a monetary/fiscal environment where one ought not think so.

Check it out: Year-to-date until a week ago, Gold's average daily net price change (either up or down) was 15 points. Now here are the net point changes for this past week (Mon-Fri): 5, 13, 8, 8, 6.

In fact, Gold's net change for the week was a wee -12 points. And further, Gold's overall high-to-low range for the past week was just 28 points, the narrowest since that ending 14 February 2020 over a year ago. Thus as we go to Gold's weekly bars from a year ago-to-date, the rightmost bar is the stubbiest of the entire lot:

"Well, mmb, the Dollar's been firming as yields are increasing..."

'Tis a good observation there, Squire. The Dollar Index this past week traded up to its highest level (92.940) in over three months as the Buck gets the bid to accommodate purchasing better yield. Why invest in the 10-Year Eurozone Central Government Bond at 0.040% when the yield on the 10-Year U.S. Treasury Note is 1.660%? Proves the point that the greater the proliferation of a currency (i.e. the Dollar), the less each unit is worth and thus the higher the reward (i.e. the yield) for taking such risk ought be, you see? (See, too, the Bolivar Soberano and ZimDollar).

But to the point of Gold's going narrow, 'tis peculiar indeed! With the diabolical debasement of the Dollar in its highest gear ever, should not Gold's trading range be more expansive that currently 'tis?

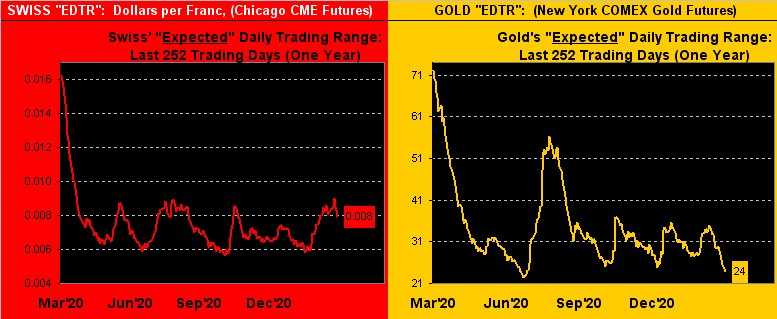

Take for example the EDTR ("expected daily trading range") of the Swiss Franc, its safe haven currency status closer to Gold than that of any other faux dough. To be sure, the Swiss Franc ($1.0671) of late has been coming off a bit given the Dollar's firming, but at least 'tis in play versus Gold's hitting the hay.

To wit, in the following two-panel graphic we've the EDTRs for the Swiss Franc on the left and for Gold on the right. The time frame is from one year ago-to-date. Note of late how the Franc's EDTR has increased from .006 points-per-day to .008 points ... but that for Gold has narrowed toward the bottom of its panel at 24 points-per-day. (And again for you WestPalmBeachers down there, this is not market direction, rather 'tis each day's anticipated distance between the high and low):

The point is: Gold for this "instant" (if you will) is not in play. 'Course, we view such "nap time" as a temporary malaise, or perhaps better stated, as a consolidative phase. Indeed per last week's missive, we expect Gold to now be on the rise, even with 1800 as a reasonably near-term prize.

Moreover, we're maintaining 2401 as our year's forecast high. That target is 39% above Gold's present 1732 level with some nine months left in 2021. But can Gold actually spring up that much so quickly? Historically it has done so on better than a dozen mutually-exclusive nine-month (or less) occasions in the last 15 years alone. So nothing new there. "Got Gold?"

Helpful to Gold's cause shall be an S&P 500 crash on the order of -50%, (the case for which in the email traffic is becoming more and more realized ... and even modest by some analysts' measures).

Let's briefly review Gold's performance across the breadth of the prior two -50% S&P crashes:

■ First we've the -50% DotComBomb which lasted from August of 2000 into October of 2002: Gold's change for the same period was +21%;

■ Second was the -50% GlobalFinFlop which lasted from October of 2007 into March of 2009: Gold's change for the same period was +33%;

■ Today (unless everything we were taught was wrong or is no longer relevant) we continue to await the "Look Ma, No Earnings!" crash, which even if -50% would still find the S&P 500 "expensive", but Gold again materially higher.

To be sure, the S&P's next crash is a day-to-day waiting game, but to reprise an advert quip from then evening San Francisco Examiner: "A lot can happen between 9 and 5."

Meanwhile, from the "At What The Heck Are You Looking Dept.", we uttered quite the guffaw this past Wednesday upon Dow Jones Newswires referring to the U.S. Economy as "Hot". Obviously they adore "can do no wrong" PrezJoe, but come on man, look at the Economic Barometer:

And again, that rightmost pip of the S&P 500 (red line) is an all-time closing high at 3975. Just bear in mind (for the billionth time): yields are rising and exceeding that of the S&P (1.465%); 84 of the S&P's 505 constituents have negative 12-month earnings; our "live" price-earnings ratio for the Index is at present 72.0x; and (for the cherry on top) the Senate is moving for "sharp corporate tax increases" which can only push the P/E even higher (ex-the inevitable crash). Just in case you're scoring at home.

As for the Econ Baro's metrics recorded this past week, obviously by the declining blue line they again were poor, notably with Feb's slowing of Home Sales, and actual shrinkage in both Personal Income and Personal Spending, as well as in Durable Orders. 'Course Federal Reserve Chair Powell was right there, stating that his bank shall continue to support the U.S. economy (even though 'tis "hot", right?) and that Federal Debt reduction should not be an issue for now. (Really?) Instead, the bank is assessing conversion to a digital Dollar. "Got bits**t?" (Whilst we deplore the latter, at least its supply supposedly is fixed...)

As to some extent is the supply of Gold. To be fair with our opening Scoreboard valuation of Gold (the current reading being 3734), one must include Gold's marginally increasing supply in the calculation: to otherwise not so do is to cheat, (as is typically done with the P/E of the S&P: "Well, if we include the negative P/Es, they'll make the ratio appear attractively lower.") Typically around some 85 million ounces of Gold are added annually to its global supply. Seems a large number, but essentially by volume 'tis just some 147 cubic meters, or less than three standard size shipping containers: that's it. 'Tis taken nearly 40 years for the supply of Gold to double; the supply of Dollars has doubled in just nine years. "What's in your wallet?"

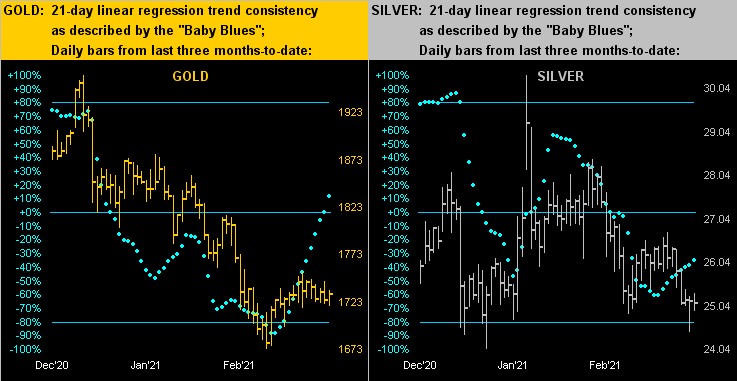

What's in our next two-panel graphic are the daily bars of Gold (below left) and Silver (below right) along with their "Baby Blues", those dots of regression trend consistency. As much as we are looking for price to rise near-term, neither panel looks overly encouraging. Gold's "Baby Blues" have been zooming up nicely, but with trading at present out of puff, they look set to stall until price itself begins climbing the wall. As for Silver, she's gonna be playing the blues should her price not rise soon:

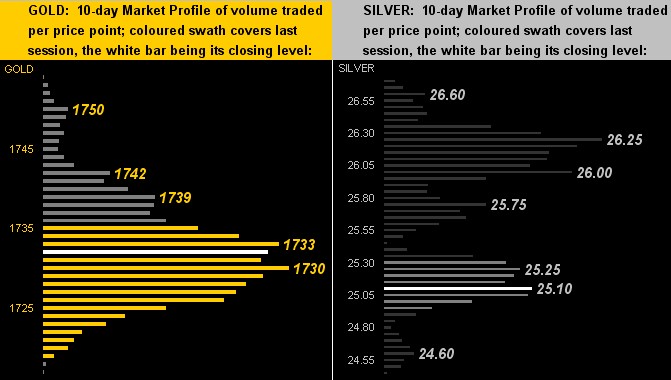

And as for their respective 10-day Market Profiles, Gold's narrowness (at left) thus finds price in the belly of the beast, with Silver's struggling (at right) to maintain the 25s. Hang in there Sister Silver!

Still, the fundamentals remain Gold-positive (understatement), even if trading at present is narrow. The Stateside Legislative Branch's raising taxes (thus reducing already terrible earnings) shall send the S&P 500 over the cliff, whilst the Executive Branch's certain signing for another $3 trillion in spending shall beautifully well bode for one's Gold lode!

www.deMeadville.com

www.TheGoldUpdate.com

********

Mark Mead Baillie has had an extensive business career beginning in banking and financial services for two years with Banque Nationale de Paris to corporate research for three years at Barclays Bank and then for six years as an analyst and corporate lender with Société Générale.

For the last 22 years he has expanded his financial expertise by creating his own financial services company, de Meadville International, which comprehensively follows his BEGOS complex of markets (Bond/Euro/Gold/Oil/S&P) and the trading of the futures therein. He is recognized within the financial community of demonstrating creative technical skills that surpass industry standards toward making highly informed market assessments and his work is featured in Merrill Lynch Wealth Management client presentations. He has adapted such skills into becoming the popular author each week of the prolific “The Gold Update” and is known in the financial website community as “mmb” and “deMeadville”.

Mr. Baillie holds a BS in Business from the University of Southern California and an MBA in Finance from Golden Gate University.