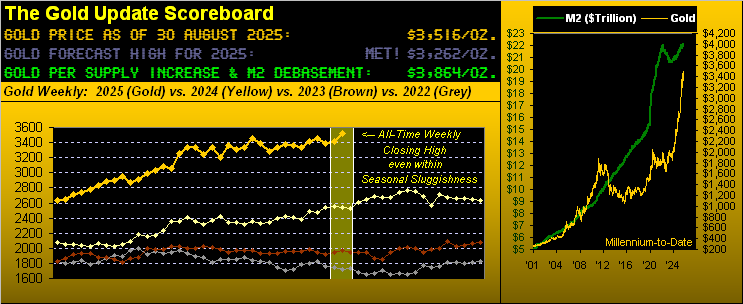

Gold Lookin’ Sporty; Silver Lovin’ Forty!

Absolutely we must start with Sweet Sister Silver. By her “continuous contract” (the front month for which is now December), she attained $40/oz. yesterday for the first time since (deep breath!) 21 September 2011; (for you math-challenged WestPalmBeachers down there, that is essentially 14 years ago). “Brava, Brava, Sista Silva!!”

‘Tis been long overdue, and yet Silver still remains “La Cheapa”. In settling out the week and August yesterday (Friday) at 40.75, the Gold/Silver ratio now at 86.3x nonetheless remains excessively above the century-to-date average of 69.3x. Thus as fabulous as ’tis to see Silver lovin’ $40/oz., were she priced today at that ratio’s average, she’d instead be +25% higher at $50/oz., (indeed at 50.76 for those of you scoring at home).

As for good old Gold, price settled the week lookin’ sporty at 3516, which too by its “continuous contract” (also now December) is another All-Time Closing High on both a daily and weekly basis; however the All-Time Intraday High remains 3431 from three weeks prior on 08 August. But “sluggish seasonality” aside, we’ll take it. Here are Gold’s weekly bars from a year ago-to-date, the rightmost blue-dotted parabolic Long trend nicely in place with price itself sitting upon the dashed regression trendline:

And whilst September is the worst month of the year for S&P 500, (as herein penned a week ago that “…through the 24 Septembers century-to-date, that month’s cumulative S&P change is -32.3%…”), ’tis been for Gold on balance a decent month, its past 24 Septembers netting an all-in gain of +7.2%. Too, by current conventional wisdom, Gold stands to benefit from this next 17 September Federal Open Market Committee vote to cut the FundsRate by -0.25%. But: ought they so do? Let’s go to our completed StateSide inflation summary table for July, bearing in mind that red backgrounds are in excess of the Fed’s inflation target of 2%…

…and “Uh-oh, say it ain’t so…” every measure now is backed in red. ‘Course that can be resolved with a rate hike … else exacerbated with a rate cut. Plus for August, both wholesale and retail inflation data shall be reported the week prior to the FOMC’s Policy Statement. Either way, if next week brings poor data for August’s payrolls, that shall be cut-friendly.

“But mmb, if jobs go down and inflation goes up, then what?”

‘Twould be ever so stagflative, dear Squire, such that the Fed may have to simply sit on its hands in being “…attentive to the risks to both sides of its dual mandate…” Not great. Add in the ongoing, ridiculous overvaluation of the S&P 500, and September may not be a very happy month, (unless one holds Gold).

Indeed as we next turn to our year-to-date standings of the BEGOS Markets, the Metals Triumvirate continues to own the podium, with Silver (as we’ve herein anticipated) rightly topping the stack in regaining $40/oz. by her rallying comeback:

Therein we also see the severely-stretched S&P 500 up +9.8% to this point, but actually underperforming the full percentage changes of the prior two years. And now with September in the balance, ‘twouldn’t be untoward by year-end to find the S&P in the red (see later our closing graphic).

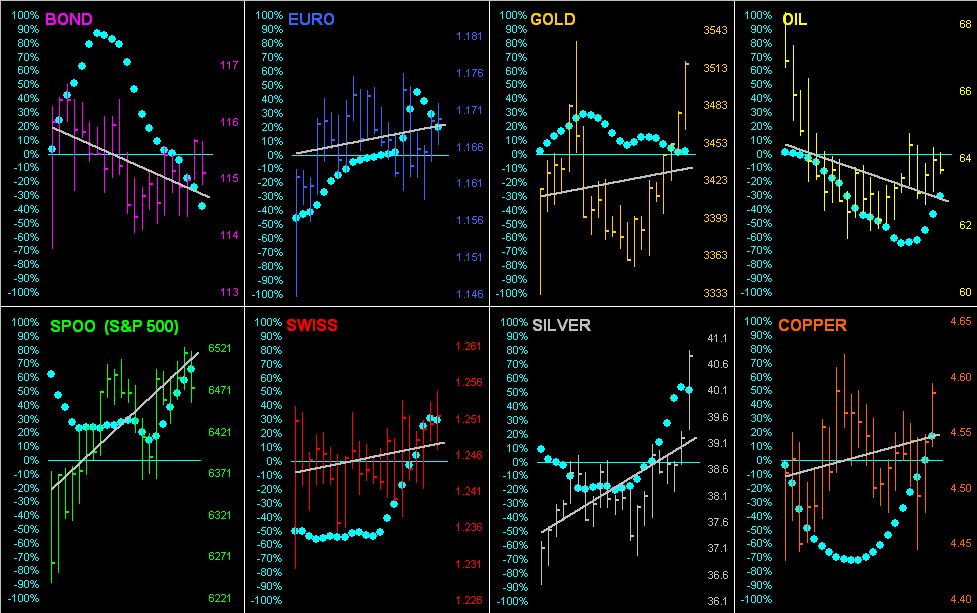

Yet in looking at the BEGOS bunch across the past 21 trading days (one month), let’s go ’round the horn by their respective daily bars, grey trendlines and “Baby Blues”, the dots which depict each trend’s day-to-day consistency. And specific to the Bond, yesterday was its worst net daily change since 15 August, that day having been a week prior to non-committal FedChair Powell in Jackson Hole. So, are the “Bond Ghouls” (hat-tip the late Louis Rukeyser) thinking the Fed may not cut come 17 September? That would not make for a happy head of The Executive Branch in Washington:

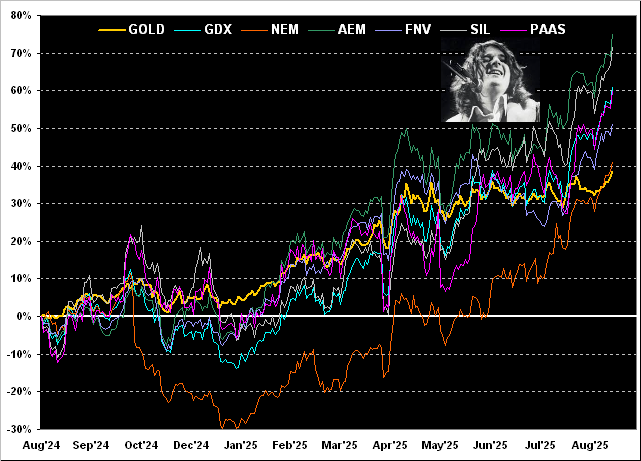

However on a happier note, let’s go to Gold’s percentage track from one year ago-to-date along with our usual top-tier precious metals equities. And from “worst-to-first” — the leverage of the equities over Gold really now standing out — they rank as: Gold itself +38%, Newmont (NEM) +41%, Franco-Nevada (FNV) +51%, Pan American Silver (PAAS) +60%, the VanEck Vectors Gold Miners exchange-traded fund (GDX) +61%, the Global X Silver Miners exchange-traded fund (SIL) +72%, and Agnico Eagle Mines (AEM) +75%. Cue Steve Miller from back in ’76: “Fly Like an Eagle”:

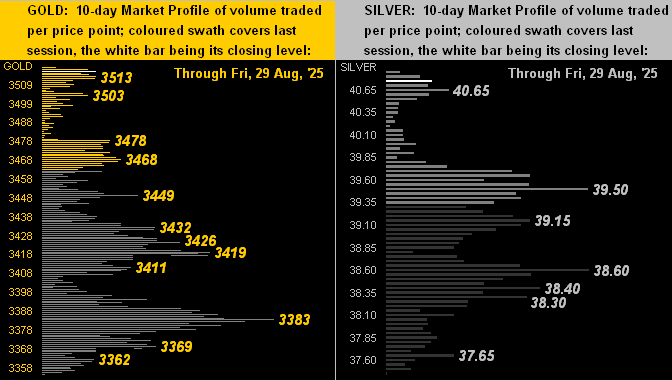

Next let’s zoom in on the 10-day Market Profiles for Gold on the left and our star player Sister Silver on the right, the respective white bars being yesterday’s settles. To borrow from a 1913 newspaper advertisement for Ohio’s Piqua Auto Supply House, “One look is worth a thousand words“. Thus in this case, nothing else need be said:

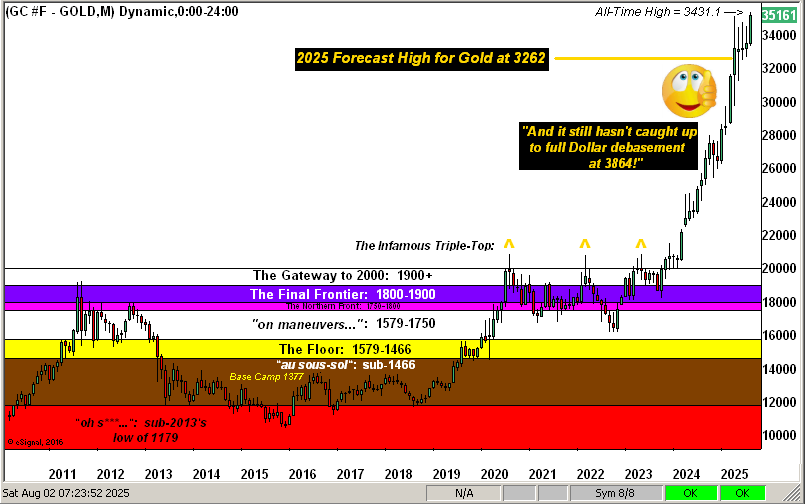

Too, words are challenging by which to come as we turn to Gold’s Structure per the monthly bars since 2010. But unlike the S&P 500 — which for month-after-month has been valued pathetically beyond perfection despite unsupportive earnings — Gold remains priced (per our opening Scoreboard) at a discount to Dollar debasement. Got Gold?

For this week’s missive we’ve saved the Economic Barometer toward the end as it segues well with what we’re perceiving as the perfect September storm. As aforementioned, across the past 24 years the S&P 500’s cumulative percentage changes for September come to -32.3%; moreover from the “7/11 Dept.”, seven of the past 11 Septembers have finished in the red. And what if en rout the Fed does not budge on 17 September?

Again, August job creation (or lack thereof) works in the Fed’s cutting favour. And the Chicago Purchasing Managers’ Index for the month just came in as quite sour, down from July’s 47.1 — and missing by a mile the consensus for 46.0 — at 41.5. Yet on the other hand, (hat-tip Bloomy), Chicago FedPrez (and FOMC voting member) Austan “The Gools” Goolsbee is less concerned about the employment picture than the inflation outlook. Also, both Personal Income and Spending increased their paces for July. Further too, of the past week’s 12 incoming Econ Baro metrics, just four were worse period-over-period. Therefore: does apparent economic strength warrant cutting the rate? The perfect September storm indeed:

Thus into September we go with this friendly graphic reminder:

Reprised query: “Do you know where your stops are?”

Here’s to Gold and Super Stellar Silver!

Cheers!

…m…

www.TheGoldUpdate.com

www.deMeadville.com

and now on “X”: @deMeadvillePro

********

Mark Mead Baillie has had an extensive business career beginning in banking and financial services for two years with Banque Nationale de Paris to corporate research for three years at Barclays Bank and then for six years as an analyst and corporate lender with Société Générale.

For the last 22 years he has expanded his financial expertise by creating his own financial services company, de Meadville International, which comprehensively follows his BEGOS complex of markets (Bond/Euro/Gold/Oil/S&P) and the trading of the futures therein. He is recognized within the financial community of demonstrating creative technical skills that surpass industry standards toward making highly informed market assessments and his work is featured in Merrill Lynch Wealth Management client presentations. He has adapted such skills into becoming the popular author each week of the prolific “The Gold Update” and is known in the financial website community as “mmb” and “deMeadville”.

Mr. Baillie holds a BS in Business from the University of Southern California and an MBA in Finance from Golden Gate University.