Gold Still in Stall, Looks Further to Fall

Wave the Gold Flag as vigorously as we might, that ol' phrase "the market is never wrong" remains Gold's plight, (arguably with scheming manipulators a-sleight). And with Gold now in stall, price looks further to fall, (which if you've been keeping abreast of these weekly missives ought not be a surprise at all).

We can simply look at Gold's last three months by the day in context with the following graphic's rightmost selling: price thus repelling. Note from this year's high at 1975 the two forceful down days followed by three skittish up attempts this past Monday through Wednesday, all of which were then hoovered away just this past Thursday, price en route to settling out the week yesterday (Friday) at 1876:

We've thus drawn on the above chart a support zone spanning from 1851-to-1798. For if Gold doesn't get a grip right here, price in the ensuing week need only to trade down through 1863 (just a point below this past week's low) -- and by Gold's weekly bars as we next show -- the blue-dotted parabolic Long trend now 14 weeks in duration shall flip to Short and into the support zone we'll go:

And "assuming" the flip from Long to Short confirms in the new week, recall from our prior missive that "...for the past 10 parabolic Short trends, the average decline from the flip price is -153 points..." However, a move from 1863 - 153 = 1710 seems irrational, (let alone does Gold's present price of 1876 being but half our opening Scoreboard's valuation of 3862). Again our refrain: "What the hell are we doing way down here?

"Well, the volume still isn't really there, mmb..."

Succinctly said, Squire. Whilst Gold did begin this year with a bit of a bang, trading volume has since waned such that through these first 28 trading days of 2023, any materially price-moving interest in buying the yellow metal still seems at bay; (price year-to-date is now just +2.5% after being +7.9%). Across the past ten years, here is the respective cumulative volume through such opening 28 days per year, this year being but a smidge higher than a year ago, and basically half the more robust trading we saw in both 2018 (albeit a net down year for price) and 2020 (a firm up year for price to its still present 2089 All-Time High):

And until Gold ceases being kicked around as a commodity and is eventually driven higher upon the realization of it being the world's de facto true currency, we sense the technicals (such as our parabolics and so forth) shall continue to trump the fundamentals. And various near-term technicals suggest lower levels. Again however: we look to these 1800s as being price supportive with a new All-Time High in this year's balance.

Speaking of balance, the Economic Barometer is attempting to regain same, although this past week was nearly void of any substantive incoming data, save for the (no surprise) ever-burgeoning U.S. Trade Deficit; December's Consumer Credit, too, weakened, which is a negative participation concern. But there were positives from February's first read of The University of Michigan's "Go Blue!" Sentiment Survey, January's reduction in the Treasury's Budget Deficit, and December's working off of Wholesale Inventories. And thus a wee up-blip for the Baro:

That said, Mr. President, at odds over a pending StateSide recession are SecTreas Janet "Old Yeller" Yellen versus BofA CEO Brian "Pay Cut" Moynihan, the former saying "Nay" whilst the latter says "Yea". Best to watch the Econ Baro for the true play.

Meanwhile, we read of tech company carnage continuing, of note this past week the Silly Con Valley entity known as "Yahoo!" letting go 20% of its workforce (no "Yahooing!" going on there), whilst across the Southwest in a Texas town the employee count at Dell is going down.

As for the stock market, we herein took quite the usual whack at it a week ago, the state of earnings and yield being so low. Indeed you may also have seen this quote from one Nassim "Nicky" Taleb [aka Mr. Black Swan] who queried the MarketWatch folks the prior week with: "Why should you put your money in the stock that gives you 2% dividend yield, if you’re lucky, when you can get 4.75% from the bank while playing golf?" (Clearly he must be reading The Gold Update).

Further jumping on the overpriced equities bandwagon this past Wednesday from another Morgan Stanley standout came CIO Lisa "Shall I?" Shalett as seeing (hat-tip Bloomy): "Massive Disconnects" in stocks, which falls neatly in line with our S&P "live" price/earnings ratio having settled the week at 40.1x. (We shan't again drag you through the downside math, but as you know, the potential price plunge is indeed "massive").

Moreover from the "Sounds Familiar Dept." we've recently likened the market's ongoing nonearnings-supportive run back to those days leading up to the DotComBomb which began after the S&P peaked at 1553 on 24 March 2000. The "live" P/E then? 43.2x ... just in case you're scoring at home and fully knowledgeable that the lifetime mean is 22.5x. (Hint-hint, wink-wink, nudge-nudge, elbow-elbow...)

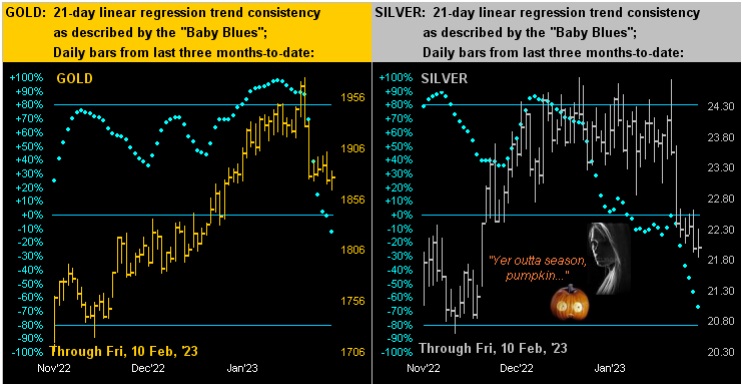

'Course waiting neither for hints and nudges are precious metals prices which for Gold on the left and for Silver on the right across the past three months now find their respective 21-day linear regression trends having rotated to negative, notably so for Silver. Indeed (as earlier displayed), the Gold/Silver ratio today stands at 85.3x, its highest reading since Halloween... BOO!:

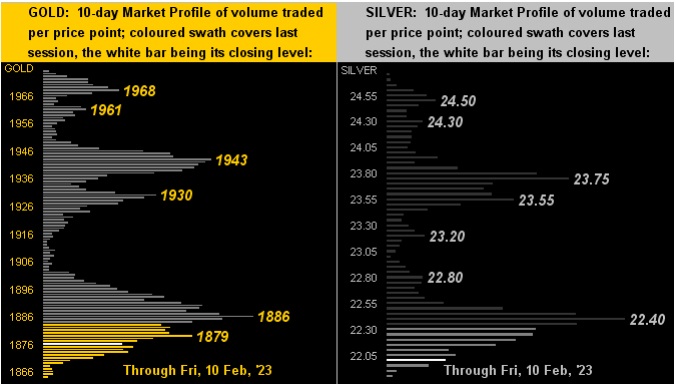

And as to the 10-day Market Profiles for Gold (below left) and for Silver (below right), both remain as cellar dwellers with still lower levels likely looming:

However not looming in the new week is a dearth of data. For the Econ Baro we've 18 incoming metrics, the most of any week in memory, (without combing back through the Baro's history of 1,284 weeks). More importantly (notwithstanding a near-term blight) toward proper portfolio grooming you do have some Gold, right? Better than ending up financially plowed amongst the "What was I Thinking?" crowd.

Cheers!

...m...

********

Mark Mead Baillie has had an extensive business career beginning in banking and financial services for two years with Banque Nationale de Paris to corporate research for three years at Barclays Bank and then for six years as an analyst and corporate lender with Société Générale.

For the last 22 years he has expanded his financial expertise by creating his own financial services company, de Meadville International, which comprehensively follows his BEGOS complex of markets (Bond/Euro/Gold/Oil/S&P) and the trading of the futures therein. He is recognized within the financial community of demonstrating creative technical skills that surpass industry standards toward making highly informed market assessments and his work is featured in Merrill Lynch Wealth Management client presentations. He has adapted such skills into becoming the popular author each week of the prolific “The Gold Update” and is known in the financial website community as “mmb” and “deMeadville”.

Mr. Baillie holds a BS in Business from the University of Southern California and an MBA in Finance from Golden Gate University.