Hyperinflation Today?

Though it is too early to know how the war will evolve, markets are vulnerable. First Covid, now the war, it is clear however that amid the uncertainty, that deficits as far as “the eye can see” will be the norm. Inflation is the result, hyperinflation a possibility. In the last century, hyperinflation often was a consequence of wars from Weimar Germany after losing WWI, to China in the 30s, to Afghanistan today. Of concern is that we believe the United States is following the same destructive path that they and others like Turkey, Venezuela and Russia are now grappling daily with hyperinflation-type supply shortages and sinking currencies. In each of the previous periods, their governments ran massive deficits, racking up huge national debts and each had a central bank creating money to pay their bills. In each instance also there was a complacency in policymaking and economics.

One of the most wretched examples was Weimar Germany’s hyperinflation whose economy collapsed into economic oblivion such that in 1923, one dollar was worth 4.2 trillion marks vs 42 marks in January 1920 which helped pave the way for Adolf Hitler’s rise to power. The origin of the Great German inflation was due to the huge deficits run by the government during World War I and the Treaty of Versailles’ heavy reparation payments which were financed by the unlimited issuance of marks. A litre of milk which had cost 7 marks in April 1922, cost 26 marks five months later. Hyperinflation is not even a modern problem. Ancient Rome too suffered from hyperinflation when Emperor Diocletian fixed the price of 30,000 denarii for one pound of gold and 10 years later it had risen to 120,000 denarii ending in 337 when a pound of gold was worth 20,000,000 denarii. Wars were a factor then and today.

The Danger of Runaway Inflation

Hyperinflation is a rapid and unchecked increase in prices caused by excessive government spending and often, a falling currency. Noted economist Milton Friedman famously said, “Inflation is always and everywhere a monetary phenomenon in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output”. Through the chaos of the last few years, and particularly the last few weeks, history may be repeating itself as first Russia and then the United States are well on their way to risking the break-up of the international monetary system which could vault us into a hyperinflation spiral of yesteryears.

Turkey already is suffering from a Weimar-style hyperinflation with runaway inflation soaring at 55%. As a result, the lira has lost 50% of its value despite numerous multi-billion dollar central bank interventions that has cost the jobs of three central bank governors in three years. Food prices have jumped 65% as imports cost more. To shore up the lira, the central bank unveiled plans to persuade its citizens to swap some $50 billion worth of gold “held under the mattress” for lira. For thousands of years the Turks have bought gold as protection against a history of rampant inflation and to guard their wealth, gold was given as traditional gifts during weddings and births.

But don’t blame the Turkish central bank. Most central banks are supposed to be stewards of our money, but instead have become creators of our money accommodating their governments’ voracious demands and drowning them in debt. Central banks are part of the problem. Today the United States is flirting with double digit inflation and the war will ensure a commodity supercycle last seen in the Seventies. Commodity supercycles are decade long periods when commodities trade above their long term trend. They are rare, only five in the last century.

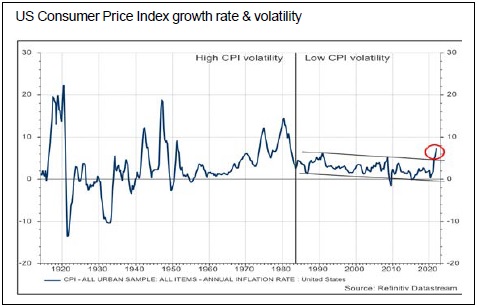

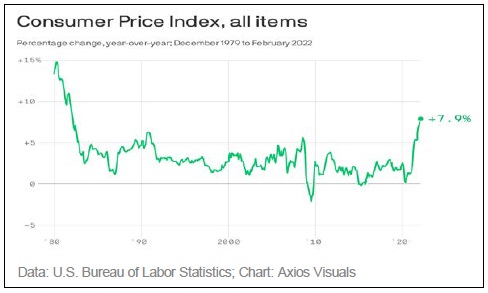

We believe that chaos in the global commodity market means higher interest rates, problematic for the United States, the world’s biggest debtor and money printer. US CPI has hit fresh 40-year highs near 8%, ahead of the surge in energy and commodity prices following Russia’s invasion. The Fed is torn between fighting inflation and cushioning the economy from the fallout from the war. Inflation keeps going higher. Up and up. Worrisome because the national debt has already reached a record $30 trillion and the Fed’s balance sheet has climbed to $9 trillion, paving the way for even more inflation, maybe hyperinflation.

America has flirted with hyperinflation before. Federal Reserve Chairman Paul Volcker was forced to stop the threat of hyperinflation from two OPEC oil shocks and reckless government spending targeting the amount of money in the economy, raising interest rates to double digit levels, which crushed inflation but caused two recessions and double digit unemployment. Today, current Fed Chair Powell has responded to the worst inflation in four decades taking the first tiny step, raising rates by 0.25% for the first time in 3 years, even after inflation is running hot. Like the early Twenties and the Seventies, central banks today are reluctant to take the necessary steps to stop inflation, despite creating money without limit that helped inflate the world’s biggest bubble in history. It is not hard to be struck by the parallels of the past, and yet after trillions of pandemic stimulus packages, we expect government support again to offset the higher costs of war, with yet another round of extraordinary fiscal support or money creation. Milton Friedman’s other popular observation was, “that there’s no such thing as a free lunch.” And this time, Mr. Volcker is not around.

The Russians Are Coming, The Russians Are Coming

We believe the Ukraine invasion is the ratcheting point in the commodity supercycle. History shows that the combination of war, supply shocks and high inflation are destabilizing factors. The isolation of the Russian economy, once the 11th biggest economy in the world and one of its largest commodity producers will force already high prices higher, problematic for Europe which is heavily dependent on Russian energy. Energy markets and financial markets have become global with Europe depending on cheap energy from Russia for one third of its natural gas imports. Trade represents about 46% of Russia’s GDP, so “Fortress Russia” relies heavily on its customers. Russia also supplies about 10% of the world’s oil and more than 15% of its gas and the weaponization of gas supplies earlier this year helped push global energy prices to record levels. Noteworthy is that in ignoring US pressure and sanctions, the EU, India and China will continue to buy Russian crude, despite the American oil embargo. Europe sends Moscow 800 million euros every day to pay for its energy bill. Russian also supplies half of Germany’s requirement. But the lifeline is not enough.

The high risk economic war and piling on of unprecedented sanctions will sink the $1.6 trillion Russian economy into a black hole on the scale of its 1998 financial crisis which bankrupted the nation. Russia has joined other pariah states like North Korea, Venezuela and Iran. The Russian ruble has lost 50% of its value since the invasion and the economic boycott has impoverished its people, crippled its stock market and currency, raising prices of everything in a hyperinflation frenzy. A weaker ruble has raised the cost of imports like sugar, bananas and tomatoes which spiked 15% in a month. Russia’s central bank was forced to double its interest rate to 20% to prop up the ruble, now worth less than a penny. Half of its pile of foreign exchange reserves of $643 billion were vaporized, undermining Russia’s central bank efforts to prevent a run on its banks as Russian banks and the government are cut off from foreign exchange reserves and debt markets. To stem the collapse and stop the flight of capital, Russia put a ban on foreigners selling Russian assets after Exxon, BP and Shell announced plans to sell their Russian holdings, and some 400 companies had left already.

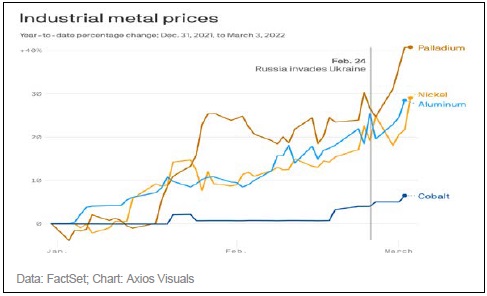

The Russian bear has awakened the world. The chaos in Russia’s financial markets will have consequences for the global economy and markets hurting investors who were earlier smitten with Russia’s reserves and market. The West’s entire post-Cold War policy will be replaced by an inflationary build-up in military spending, reorganization of supply lines and even a resumption of nuclear projects, Russia is a major producer of copper, aluminum and produces 12% of the world supply of palladium used in catalytic converters. Global demand for critical minerals used in renewables has soared. Inflation had raised the cost of commodities like lithium, cobalt and nickel used in the making of batteries for EVs. One wind turbine machine for example weighs 100 tonnes containing copper, steel and rare earths. Copper has jumped 60% and steel hikes raised the cost by 50%. Aluminum is at record highs and is used for everything from beer cans to EVs. Following Germany’s “U turn” on defense spending, every other country will bolster military budgets to meet an increasingly murky security outlook which will require more critical metals as hard power replaces soft power. All this is part of the rising cost of everything, now exacerbated by Russia’s invasion and the disruption of all important supply chains.

It’s not just metal. Russia and Ukraine are major food producers, often considered the bread basket of the world, accounting for nearly one third of the world’s wheat and barley exports. As well as fertilizers they are among the world’s leading exporters of corn and rapeseed, particularly to lesser developed countries in Africa and Middle East. Wheat futures hit record highs on fears of the worst disruption to wheat supplies since the first world war. Food will cost more. And interconnected global supply chains will take longer to unsnarl while supplies remain tight.

According to the Bank for International Settlements, Russian linked entities have borrowed almost $150 billion in dollar and euro-denominated bonds and with sanctions effectively cutting off Russia from the global financial system, a domino-type default will finance trigger credit default swaps (CDS). It was those same derivatives of mass destruction that almost sank the global financial system in 2008. BlackRock funds disclosed that its funds took a $18 billion hit owing to markdowns in Russian holdings. Déjà vu. Russia needs vital dollars. However the assets of Putin and some 500 oligarchs have been frozen. As Russians face economic, financial and geopolitical ruin, confidence has evaporated. The full impact of these ruinous sanctions is unknown, yet the freezing of Russia’s reserves leaves them little enough to prevent Russia’s financial and economic ruin and a default on its dollar-denominated bonds. Hyperinflation now?

American Exceptionalism

What a difference a war makes. Of concern is that there are also parallels today in the United States with hyperinflations past. We believe that the United States won’t be spared. First, monetary and fiscal policies remain too loose in an effort to keep the economic momentum from stalling and protect voters from rising inflation. In the past two years, Congress has passed roughly $5 trillion worth of relief packages or 13% of GDP, that fueled a surge in demand and that inflation frustrating its creators. Notwithstanding the Fed’s hawkish rhetoric and a tepid quarter percentage point increase, there is a reluctance like President Erdoğan of Turkey to raise rates by much, leaving the Fed to jawbone and tinker. But with the balance sheets of households, businesses and governments interconnected and the scale of outstanding debt at record levels, the economic fallout from the war has changed views on debt.

Second, world debt to GDP is currently at over 300% and the world's leading country has debts at 130% of GDP and the cost of the Ukraine conflict is yet to be calculated. Of concern is that the pandemic had already drained America’s resources leaving the economy like Turkey exposed. Worrisome is that America continues to maintain loose monetary and fiscal policies which threatens to further drive up the cost of doing business.

Third, start with the feedstock of inflation, M2 broad money supply has increased a whopping 40% since February 2020 and higher than pre-epidemic levels. Milton Friedman once observed, “monetary policy is not about interest rates, it is about the growth of the quantity of money”. Today, consumption makes up almost 70% of America’s GDP and America’s rebound in spending despite the ever-changing Covid landscape continues unabated. The Fed had viewed the supply chain disruptions “temporary” blaming the pandemic but now the war has unleashed one of the biggest commodity shocks and commodity supercycles causing booming prices for “everything”. The Fed is part of the problem. US debt is unsustainable and the bill to resurrect the Iron Curtain and its aftermath has yet to come due. Public debt charges will only increase in the years ahead as interest rates rise. While central banks’ balance sheets were supposed to shrink in a form of “quantitative tightening”, a systemic shift is underway and the inflation shock from the war is poised to hit double digit levels. Like Turkey, Russia and the United States are caught in a debt trap. Hyperinflation now?

The turmoil unfolding in the energy, food and metals market is broad and pervasive, particularly since we are also experiencing widespread inflation for key energy, materials and food prices at 40-year highs and that was even before Russia invaded Ukraine. US oil prices rose 70% over last year. Double-digit inflation is a real risk. The US economy is particularly vulnerable to inflation, specifically energy. The genie is out of the bottle, thanks in part to Covid. Energy was soaring before the Russian invasion due largely to the fossil fuel divestments from the global green effort that limited oil and gas spending. Also low inventories have left the world with tight markets and little spare capacity. The move to renewables hobbled fossil fuel capacity which was shutdown at a faster pace than the bringing on of renewable capacity. Germany is to shutdown their last nuclear plant this year, ironically making them more dependent on Russian gas. Of growing concern is that the greater the loss from Russian oil and gas, the higher energy prices will go.

Commodity Supercycle Is Upon Us

We believe that the more powerful economic and individual sanctions, the greater the risk of collateral damage and the more they are used, the less effectiveness as countries seek alternatives. Powerful financial sanctions are a double-edged sword since there is also a heavy Western cost, much more than the supply shocks which make a bad inflation problem worse. After all sanctions did not stop Putin from invading Ukraine, they only increased its cost. The confiscation of half of Russia’s central bank reserves not only removed Russia’s ability to prop up the ruble, it sent a message that foreign exchange reserves could now be made inert and confiscated, particularly when a country needs the reserves most. Foreign exchange reserves no longer are stores of value and is the beginning of the end of the post-Forties unipolar monetary order based on a fiat dollar, established in 1971 when President Nixon severed its linkage to gold.

We also believe that the economic rupture between Russia and the West introduces a new era of economic warfare which will have profound effects that might take generations for Russia to recover. Three decades later, we didn’t win the Cold War, it only went into hibernation. The longer-term fallout is the end of global supply chains, globalization and integrated markets. And there is now a political risk premium to add to the commodity calamity.

The world faces even higher inflation and a commodity supercycle reminiscent of the 1970s “Great Inflation” whose roots stretched back to Lyndon B. Johnson’s “guns and butter” deficit policies of the mid-60s that led to too much stimulus, strong economic growth and a surge in prices as supplies were disrupted by two OPEC oil shocks. The economy entered a commodity supercycle, overheated and inflation reached near hyperinflation levels within the decade. The dollar was subsequently severed from its linkage to gold. Today, prices are again rising and a war complicates the geopolitical picture. Inflation fighting like then, is nowhere to be seen. The Fed’s monetary spigots remains open as energy has spiked from 10% of GDP to almost 20%, a level once reached in the “Great Inflation” 1970s. And the fifth commodity supercycle has begun, similar to the 1970s. Fasten your seatbelts.

A Chinese Gold Standard?

Different this time is that the rules-based world order stitched together after the Second World War threatens to unravel, ushering in an economic war with the dollar-based system set up in the Forties. Russia’s onslaught on Ukraine has made financial markets another field of battle. At one time, foreign exchange reserves were an asset but with the freezing of billions of Russian sovereign wealth, countries will seek to reduce their reliance on dollars and diversify making it harder to weaponize the dollar system next time. Russia’s isolation from the West makes that country more reliant on China, who will use the sanctions as an opportunity to buy Russian grain and energy on the cheap. Asia, led by China remains the biggest single engine of economic expansion, the source of 60% of global gross domestic product. And as more countries are added to the sanction list, they prove less effective as countries find ways to bypass the system.

China is both Ukraine and Russia’s largest trading partner and a China-Russia axis will have global financial implications. The West’s sanctions have tied China and Russia more closely together as both share a similar worldview, chafing at US financial hegemony. And there is the unintended consequence of other nations stockpiling commodities or gold instead of dollars, if their reserves could easily be frozen by a stroke of a pen. Nonetheless although demonized by America, there is the need to get China onside to influence a taciturn Putin, so the China/US rivalry for global influence may be sidelined. Both have no desire to be on “the wrong side of history”. Realpolitiks is back.

Once the largest holder of American debt, China has reduced its holdings to $1 trillion, becoming the second biggest creditor after Japan, exacerbated no doubt by Mr. Trump’s trade war with China which war was lost. Markets follow money. America has huge current account and fiscal deficits, meaning they have to borrow or print to pay their bills. America’s overworked printing press has already generated 8% inflation, so they must borrow from others. After watching the West weaponize their financial system, China has accelerated its non-reliance on the West particularly when Russia's access to SWIFT was cut off, forcing Russia to more closing align itself with China and the renminbi dominated “CIPS” (cross-border Interbank Payments System) which offers settlements in about 100 countries. When Mr. Trump imposed sanctions on Iran, the Europeans too came up with an alternative cross border payments to the SWIFT payment system to get around the curbs.

Global debt is at record levels with the US becoming the world’s largest debtor financed largely by central bank printing. In the interim, China in turn has become the world’s largest creditor with $3.2 trillion of foreign exchange reserves. Today China has the power to disrupt markets. The truth today is that America’s debt to GDP is 130%, and vulnerable to a change in capital flows. China’s economy supports a debt to GDP at 68%. America’s debt load is its Achilles heel. America’s debt is also financed by foreigners. First, under Mr. Trump and now Biden, the hawkish escalation of the economic rivalry has created a Beijing-led world order with Russia its newest member. Sanctions have helped create an Eastern-based monetary order and the China-Russia bipolar axis in turn undermines the Washington-led bloc dollar hegemony, particularly following the confiscation of Russia’s currency exchange reserves as easily as Mr. Trudeau’s government seized the dollar accounts of the Freedom Convoy.

When The Swamp Drains…

Instead of the traditional mutual fund, pension or hedge players, the beneficiary of the biggest stock market bubble in history was a different set of players that took prices to the moon. Markets today are dominated by private equity players, high-frequency traders, meme Reditt traders as well as new platforms for trading stocks, derivatives and cryptocurrencies. Unlike 2008 when Wall Street created toxic mortgage derivatives tied to the housing boom that caused an implosion sinking Wall Street’s biggest banks, there is today a broader range of assets like crypto, swaps and commodity derivatives which are much more leveraged and unregulated. In the shift of investing power from the traditional pools of capital to the “flavour of the day” type speculators, unknown is how much leverage is used, particularly with financing coming from the private equity or alternative pools where regulators are behind the curve. Unknown also is when the bubble bursts, what happens when everyone tries to get through the same door at the same time.

That is happening today where American banking losses on Russian sovereign debt derivatives and markets are in the multi-billions in a rush for the exits. A Russian default on its bond payments looms and there is the collateral financial fallout on Wall Street. Margin calls have hit the commodity markets and the largest energy trading players are asking the central banks for bailouts to avoid a Lehman-type crash. In the commodity markets, the 145 year old London Metal Exchange (LME) stopped trading in nickel after it was disclosed that the world’s second largest nickel and stainless steel producer, Tsingshan Holding Group faced $8 billion of losses after a cascade of margin calls. The Chinese government stepped in to save Tsingshan as the LME also cancelled bona fide trades. Some of Wall Street’s biggest banks are owed billions.

It has happened before. We recall the last Russian debt default in 1998 which triggered the collapse of the quant hedge fund Long-Term Capital Management (LTCM) after losses of $550 million triggered a global meltdown. And now the Russian government’s tearing up of decades old international treaties and passing a law allowing foreign jets to be re-registered in Russia has seen the seizure of 500 planes worth $10 billion which will result in billions of write-downs, litigation, and bankruptcies. In a tit-for-tat move, the US government introduced a bill allowing others to seize Russian oligarchs’ yachts. Markets today are vulnerable and exposed. It will only get worse.

US Spends More Than It Earns

America’s reluctance to put boots on the ground is understandable, particularly in an election year. American history shows that its military involvement often ends badly, from the retreat from Afghanistan to Korea to Vietnam and the Middle East debacles. The common denominator is that wars cost big money. Afghanistan’s price tag alone was $2 trillion. History is littered with countries that went to war leaving behind big debts whether they were the victors or losers. In the 1920s, Great Britain was once the superpower of the world and the global centre of finance. But that pre-eminent position was squandered by waging and winning the first and second World Wars which left the victor a debtor nation. As London was the financial centre of the world, Britain borrowed and borrowed but eventually had to abandon the gold standard and as a result, sterling soon lost its reserve status to be replaced by the US dollar since America was Britain’s largest creditor. The depression soon followed and now a half century later, China has become the largest creditor to the world, whilst America has become the largest debtor. The tables have turned. History shows that war debts often play a major role. Of interest is that at one time wars were financed with gold because neither side knew who would end up as the victor. However debts were always paid, even after the bankruptcy of the Weimar Germany and Great Britain. Ironically America is the largest gold holder in the world because much of the gold held at Fort Knox once belonged to its citizens and other nations like Germany and Britain.

And today America has few options, particularly because they are dependent upon foreign money to finance their consumption. The US dollar is correlated to the amount of its deficits. The dollar declined between 1960 and 1970 and the Bretton Woods system collapsed. As its twin deficits rise, the dollar must fall again. America in becoming the largest debtor in the world is vulnerable to outsiders dumping dollars. America’s financial hegemony is at risk with costly economic and security consequences, undermining its currency. Given the escalation of the Cold War and the struggle for a new world order, it would not take much for a Beijing-centric bloc to “sanction” US debt. After all, geopolitics determines economic relations. It has been done before. China and others have decided there are other alternatives, or truths. The dollar is not forever.

The yuan has withstood the geopolitical turbulence because it is an alternative to the Western dominated financial system. For many years, China has been nurturing its own financial system and Russian energy deals are already outside the US dollar-based international financial system. Noteworthy is that Saudi Arabia, recently invited China’s Xi to talks amid strained relations between Riyadh and Washington over human rights. The world’s top oil producer Saudi Arabia is in discussions with the top oil consumer to price oil in yuan to avoid using dollars. In 1973, President Nixon struck an exclusive “petrodollar” deal with Saudi Arabia with surpluses encouraged to invest in US debt. That agreement helped fund America making the dollar a global currency as the dollars soon replaced gold. Today, that dollar façade is crumbling as Saudis accept “petroyuans” for their oil.

The Golden Rule Still Rules

The United States for the first time since World War II faces adversaries in Europe and Asia. And to be sure, sanctions and financial isolation have nudged Russia and China closer together, and to seek refuge in that ultimate currency, gold. In February, there was rumours of a “whale” type sovereign buyer who accumulated enough gold to cause a short squeeze that helped push gold above $1,900/oz. Russia is the world’s sixth largest holder of gold with about 2,300 tonnes worth $153 billion accounting for roughly 25% of the bank’s official reserves. Although the West has frozen half of Russia’s war chest except for gold, Russia has more gold than dollars. China is already the largest consumer of gold and is the world’s largest gold trader. China is also the seventh largest holder in the world. Together with Russia they hold half of US reserves. There was a time when gold was money. Other central banks too have been buying gold as an alternative to the dollar. Today, in this uncertain world, gold is back in fashion.

History shows that currency debasement and debt accumulation sows the seeds for future inflation. The US has a serious problem with its massive twin deficits. Easy money has caused a structural, rather than cyclical repricing of inflation, a rare commodity supercycle. Just as there is now a need for the West’s security architecture to be reconfigured, so there is the need to protect wealth. We believe as long as the Fed postpones raising rates, the more painful the correction and, amid expensive energy, skyhigh inflation and financial spillovers, gold is a good thing to have, particularly when central banks must deal with Russian defaults while rescuing their institutions, markets and investors caught up in a debt trap as the liquidity tide moves out. Given the gargantuan size of stock and bond portfolios today there will be the need to be hedged against the inflation risks and thus the sheer size of investment demand for commodities and gold will exceed supplies.

To date, the surge in gold to near all-time highs has outpaced a strong dollar and the rise of real rates which we believe is due to a systemic shift in inflationary expectations. Combined with the record level of debt by the US government, amid its profligacy and growing concern about US dollar hegemony, gold is favoured as a traditional hedge to the uncertainty. It is also a good index of currency fears. Without confidence in the dollar, the world has no replacement reserve currency. Gold is an alternative to the dollar, a good index of currency fears. We continue to expect a near term target of $2,200/oz. Gold’s bull market has only just begun.

Recommendations

Gold flirted with all-time highs as panic set in the markets caused by Russia’s invasion. But the prospects of peace, hawkish Fed rhetoric and a drop in oil caused a pullback. Still, gold has broken out of a two-year range and we believe is poised to make record highs. Our view is that investors will turn their attention to fundamentals and a worsening inflation picture will underpin gold. While the markets expect on uptick in key lending rates, the geo-political uncertainty and the Fed’s reticence to take a stand in an election year will temper any sudden surprises.

Inflation has hit the gold mines but the increase in price of gold has more than offset the increased costs. Significantly other than Yamana, debt is not a problem and the industry has and will generate strong free cash flow. In fact, many have paid down debt and are returning value though share buybacks and dividends. This is a group with terrific Graham and Dodd fundamentals of low price/earnings multiples, solid balance sheets and above average dividends. Yet the gold industry is underweighted in most portfolios. That will not last.

We believe that the sector should be overweighted because the shares are undervalued. The industry itself are believers becoming active M&A participants with Agnico’s acquisition of Kirkland Lake, Kinross’ bid for Great Bear Resources and Rio’s $2.7 billion bid for the minority stake in Turquoise Hill. The common denominator is to replace depleting reserves – it is cheaper to buy ounces on Bay Street than to spend money and explore. In-site reserves are a bargain.

As such we continue to recommend among the seniors, Barrick Gold and Agnico-Eagle. We like B2Gold and favour developers like Dundee or McEwen Gold. Among the players that might become find themselves as part of the M&A action, we like Centamin, Eldorado and Lundin Gold which are potential pawns. However we would use IAMGOLD, New Gold and Yamana as sources of funds.

Agnico-Eagle Mines Ltd.

Agnico Eagle consummated its $10 billion merger with Kirkland Lake and within weeks, Kirkland’s former CEO Tony Makuch resigned. His sudden departure was a surprise and was likely due to "cultural differences" over Agnico’s corporate ways versus a free-wheeling culture at Kirkland. Nonetheless, Agnico expects to produce 3.3 million ounces of gold or so over the next few years at AISC $1,000/oz. We speculate that Agnico's conservative style management reflects the decision to switch Macassa’s underperforming battery autonomous fleet to a hybrid diesel system because of the potential risks underground. The world’s third largest producer now has six cornerstone assets, producing more than 3 million ounces each year with reserves of 45 million ounces. A strong balance sheet and expectations of up to $2 billion in synergies over the next decade will easily fund, total capex is estimated at $1.4 billion with development capital at $700 million. Agnico has a strong balance sheet, experienced management and a pipeline of projects in Canada, Finland and Mexico. We like the shares here.

Barrick Gold Corp.

The world’s second largest gold miner, Barrick Gold posted strong results due to stellar performances from the Nevada Gold Mines Joint Venture where reserves increased by 9.4 million ounces contributing to an overall increase of 150%. The company enjoys a strong balance sheet and will repurchase up to $1 billion of its shares over the next 12 months in the belief that its shares are undervalued and a better buy than what is out there. In Tanzania, after difficult negotiations with the government settled, the mines produced 500,000 ounces. Lumwana in Zambia was a contributor and is a long-life copper producer. Should Barrick restart Reko Diq in Pakistan, it would produce 200 million pounds of copper at $1.00/lb and 100,000 plus ounces of gold, likely by the next decade. Construction at the Pueblo Viejo JV in the Dominican Republic is 26% complete and will be commissioned later this year. Despite returning $1.4 billion to shareholders last year, Barrick was net cash positive for the second year in a row. We like Barrick here for its organic growth, foundation of six high-quality gold mines and execution capabilities. Buy.

B2Gold Corp.

B2Gold will produce one million ounces with one of the lowest AISC at less than $900/oz. Despite changes in the Mali government, B2Gold's flagship Fekola operations was unaffected. Importantly B2Gold’s Menankoto exploration permit allows for the consolidation and updated development of the Anaconda deposit, utilizing the nearby Fekola mill. We also expect an update on the 50% owned Gramalote joint venture this year which would cost $900 million to build. Not a problem since B2Gold has $673 million of cash and an undrawn $600 million revolver and cash flow of $625 million plus this year. We like B2Gold for its growth potential.

Centamin PLC

Centamin had a strong quarter and enjoys no debt, no hedges and a balance sheet with $257 million of cash. Centamin’s Sukari Gold mine is the largest gold mine in Egypt and the mine has gone underground at an average grade of 6.45 g/t. Centamin produced 415,000 ounces and will produce between 430,000 to 460,000 ounces this year at AISC $1,300/oz. Capex of $215 million includes solar and the construction of a paste-fill plant. The company expects to add 3 million ounces to its reserves which would extend mine life another 10 years. Centamin will spend $40-$45 million on exploration on its large permit ground of 160 km.2 We like the shares here for its upside potential.

Centerra Gold Inc.

Centerra produced 308,000 ounces last year from its two mines and expects to produce about 400,000 ounces this year. A new technical study at Mt. Milligan in BC will be released in the second quarter. At Öksüt in Turkey, the company halted production due to the detection of mercury at its recovery plant but it is too early whether the suspension will adversely affect earning guidance of $250 million in free cash flow for this year. The company remains in negotiations and a settlement along the lines of swapping each other's interest is likely. Still, partially over the nationalism of flagship Kumtor in the Kyrgyz Republic make up for the loss of production, Centerra acquired the Goldfield District Project in Nevada for $206 million which is a potential heap leach operation similar in size to Öksüt but requires a feasibility study. Nonetheless, with the loss of its flagship, we think the shares are dead money. Sell.

Eldorado Gold Corp.

Mid-tier Eldorado expects to produce about 475,000 ounces this year but gave little insight on their Greek Kassandra assets – no wonder they are a hidden asset. The newly commissioned HPGR circuit is expected to increase Kisladag’s heap leach mine output but really is more of a harvesting operation. At Olympias in Greece, fourth quarter production was a modest 15,000 ounces and the company is looking for a partner to joint venture its Greek Skouries expansion. At home, Eldorado plans to boost output with the completion of the decline at Lamaque in Quebec which connects the Sigma mill with the Triangle underground mine. We like Eldorado as a potential takeover tidbit.

Kinross Gold Corp.

Kinross shares were hard hit when the Russians invaded Ukraine because up to 20% of its assets are in Russia (Kupol, Dvoinoye and Udinsk). Notwithstanding that the mines in Far Eastern Russia have been operating for almost 25+ years with few problems, management has put its Russian assets on care and maintenance for an indefinite period. Kupol’s underground mine is a good cash machine generating $440 million last year. For many years Kinross has been attempting to diversify from its Russian assets but its acquisition record has been poor from the continuing problems at Tasiast in West Africa to the now outrageous acquisition of Great Bear Resources’ Dixie project for $1.8 billion, a project in Red Lake Ontario without a NI-43-101. It seems Kinross is jumping from the frying pan into the fire. Kinross at one time owned Fruta del Norte in Ecuador where it spent over a billion dollars but has nothing to show for that investment after ceding control to the Ecuadorian government. Today Lundin Gold is the beneficiary of that largesse. Kinross also passed on their minority holding of Victoria Gold’s Eagle mine which is a 300,000-ounce open pit producer in the Yukon. We think the shares are dead money. Sell.

IAMGOLD Corp.

IAMGOLD had a change in management with the sudden departures of Chair Don Charter and President Gordon Stothart under pressure from an activist fund. The board too was upgraded but it might not be enough. The changes came as joint venture Côté Gold is not only half completed but is overbudget. Rosebel in Suriname is losing money and will require $1.2 billion to make it work. At Westwood, the company is also losing money on every ounce they produce and thus IMG’s two mines cannot support the huge expenditures at Côté Lake. At Côté there still is a need to spend up to $750 million dollars which would stretch its balance sheet. IMG produced 600,000 ounces but at a whopping AISC $1,700/oz. Essakane produced 400,000 ounces and remains the crown jewel but sustaining capital is about $165 million. With reserves declining at Rosebel (2P reserves down 23% from last year) and production declining, we believe that the cash on hand at $545 million is insufficient to complete Côté. The company also did an expensive gold sale prepayment contract in 2021 for 150,000 ounces at less than the price today. The shares remain a sell.

Lundin Gold Inc.

Lundin Gold had a positive year at Fruta del Norte in southeast Ecuador producing 429,000 ounces at AISC of $762/oz with free cash flow of almost $50 million in the last quarter. The company had enough cash flow to advance a 11,000 meter exploration programme so there should be news this year from Barbasco and nearby Puente Princesa. Moreover, the south ventilation raise is almost complete which will improve operations. Fruta del Norte was commissioned in 2020 and is among the richest mines in the world at 10.6g/t with throughput to increase from 3,000 tonnes per day to 4,200 tonnes per day. The mine was completed on time and on budget. At yearend, Lundin had $263 million of cash against $740 million of debt requiring only sustaining capital of $40 million, so the mine will be a cash cow, producing about 445,000 ounces this year. We like the shares here.

Newmont Corp.

Newmont's cash flow for the quarter was $860 million with free cash flow a whopping $2.6 billion for the year enabling the company to return $1.8 billion to shareholders. The company estimates production at 6.2 million ounces this year. Newmont has $5 billion of cash and $1 billion of liquidity but did not replace its reserves at 96 million ounces last year. However Newmont will make up for the shortfall this year with the acquisition of the balance of Yanacocha from Buenaventura, one of the largest gold mines in South America. The acquisition consolidates Yanacocha but $2.5 billion must be spent on a processing facility which is expected to produce 500,000 ounces a year from the sulphides, adding 2.7 million ounces to Newmont’s reserves. Newmont has 12 operating mines, two joint ventures with the majority of its mines in secure jurisdictions. At Boddington in Australia, the mine finally showed improvement after having problems earlier in the year with its autonomous haul truck fleet (AHS). Of note is that for every $100 increase in the gold price above $1,200, Newmont expects $400 million of free cash flow. Nonetheless we prefer Barrick here for its superior growth profile.

New Gold Inc.

New Gold had a poor quarter due to lower output from underperforming New Afton and Rainy River. Material from the Intrepid zone decline in the second half of this year will help Rainy River to produce 260,000 or so ounces. However, of concern was that AISC increased to almost $1,400/oz in the quarter. Copper output was lower. New Gold has $482 million in cash, offset by $491 million in debt. New Gold will produce a flat 295,000 ounces at AISC of $1,500/oz and will lose money again. Sustaining capital of $180 to $225 million is required because of catch-up spending at the B3 zone. We would avoid the shares.

Yamana Gold Inc.

Yamana had a decent year due to the Jacobina Phase Two ramp-up which produced 230,000 ounces this year. Production from flagship El Peñón was flat because it is a maturing operation. Yamana produces about a million ounces a year but its mines are mature. Reserves were flat at 14.6 million ounces grading 0.56g/t. However joint venture Malartic has potential upside over the next few years. Yamana has $525 million of cash, up from $460 million but long-term debt stands at unhealthy $773 million. Costs are aided by copper and sliver by-products, particularly at El Peñón and Cerro Moro helping AISC at $1,000/oz. We prefer B2Gold here.

John. R. Ing

Please refer to the Legal Section of our website (maisonplacements.com) for our Research Disclosures for an explanation of our rating structure at https://maisonplacements.com/research-reports/

*******