If Something Cannot Continue Indefinitely

..it will stop. (Herb Stein an economist on Reagan’s panel in the 1980s). Now why would anyone blessed with good intelligence consider it necessary to formulate a Law that is as pure common sense as one which states, “If you stop breathing, you will die.” It would be foolish to propose this one as a Law; it will be treated as a joke. Yet Herb Stein’s Law is still relevant about 40 years later, not a joke; despite the degree to which its validity is being disregarded and ignored to pursue short term gains.

These comments are specifically aimed at Wall Street and the machinations that lie behind its near constant stellar performance of achieving serial all time highs in all three main equity indexes, the most recent of which was on Friday. Given the trend, it would be incorrect to have written, ‘. . . the last of which was on Friday’, since there is no indication as yet that Stein’s Law is having any effect on the stock market. It is thus near certain Wall Street could set new highs this week or next.

The Fed is talking about tapering their funding of the economy to return it to what is a more normal mode. A year or two ago the mere mention of tapering saw the markets over-reacting, Wall Street in particular. This time, the Fed’s whisper of reducing its QE programme had Wall Street hitting new all time highs. It is clear that stock market has now drifted into a liquidity induced coma where the life support IV of funds from the Fed and the Treasury – the latter in the process of releasing one more $trillion to what has gone before – buffers stock prices against all shocks.

But this is not the only current trend that is at risk of suffering the consequences of what Stein had said near forty years ago. The real and artificial QE of the Fed that is now at least a decade old is another. The boom in the house market that had started in the second half of the 1990s came to a bad end 10 years later on the back of the Big Banks’ shenanigans with the mortgages. Now the booming liquidity has set off a new bull market with house prices screaming higher. What will happen when money gets scarce again and the market peaks and retreats – to leave a multitude of house mortgages under water and the prospective owners unable/unwilling to serve them?

Of course the longest running market operation that really fits Stein’s law is the long lasting effort to contain the price of gold in order to protect the US dollar. In principle, this practice has to stop when metal reserves no longer adequately support the supply needed to deliver gold and silver against contracts that stand for delivery. But the Big Banks are using alternative means to meet demands for the metals. The newfound EFP (exchange for physical) contracts used to satisfy investors standing for delivery are in effect promises for delivery that are not allocated to specific bars. Redeeming the EFPs – presumably to obtain ownership of the actual metal - has onerous tax implications that are likely to keep investors happy with their paper gold and silver, thereby reducing the pressure on limited reserves.

The Banks also receive support from the US Mint, which have scaled down production of silver coins in particular – despite its mandate to produce enough coins to satisfy demand – presumably because the metal is more expensive than the ‘official’ Comex contract price. Given reports of high demand for coins, not minting silver coins release a good deal of silver that can be employed by Comex for delivery.

Both metal prices closed on a strong note last week despite the positive NFP news. If that trend continues this week, with gold and silver making good gains without large increases in their OI, this could be a sign that intervention in the market is tapering lower. Of course, we then have to wait for the important expiration of gold and silver December options and conversion of the futures near the end of November to get confirmation. The possibility still exists that higher prices during November fattens up the metal bulls for slaughter in three week’s time, as per the standard formula.

The volume of dollar printing during the past two years sooner or later must have an effect on the dollar strength. The US is now paying for imports as fast as these can be shipped and hopefully off-loaded with not too long a delay. The dollars leaving the country have the advantage of creating demand for Treasuries, but in turn this is bound to create other problems of a more strategic nature for the US.

Meanwhile Covid-19 remains in the background as the 800lb gorilla in the room. The number of new cases remains high and could increase now that winter is approaching – with indication from other countries, such as the UK which has more than 90% of its population vaccinated, that a high vaccination rate does not decrease new infections.

Corporate profits are still high, yet the average PE on the Dow30 has reached an eye- watering 42.6 and 39.3 on the S&P500. Much of the profitability comes from increases in end user prices, which means inflation has not yet become transitory. Herb Stein’s Law in effect applies fully where physical limits and constraints apply. Many trends are subject to rational and reasonable limits other than the physical; the management of household and national debt, for example/ There experience has shown an increase without limits results in ugly situations that should be avoided if at all possible.

However, experience has also shown that when the inflation bogeyman has broken loose it becomes increasingly difficult to rein him in; inflation feeds on itself. Volcker had to do it in the late 1970s and it is a painful process requiring double digit interest rates. That would not be practical in today’s circumstances and it is not known what else could really work; nothing that probably will not cause an even greater disaster. Changes in official policies to conform more to global imperatives, such as the matter of climate change and decreased use of fossil fuels now on the agenda, add further restrictions on the available options to counter unfavourable trends.

However, at centre stage in the current circumstances stands Wall Street at a too high level for economic conditions. All is not well in the economy; probably sooner rather than later a time of reckoning will come about and this time the Fed is not as free to act as it had been in March of 2009.

Some distressing news about the vaccines are here and here for interested readers.

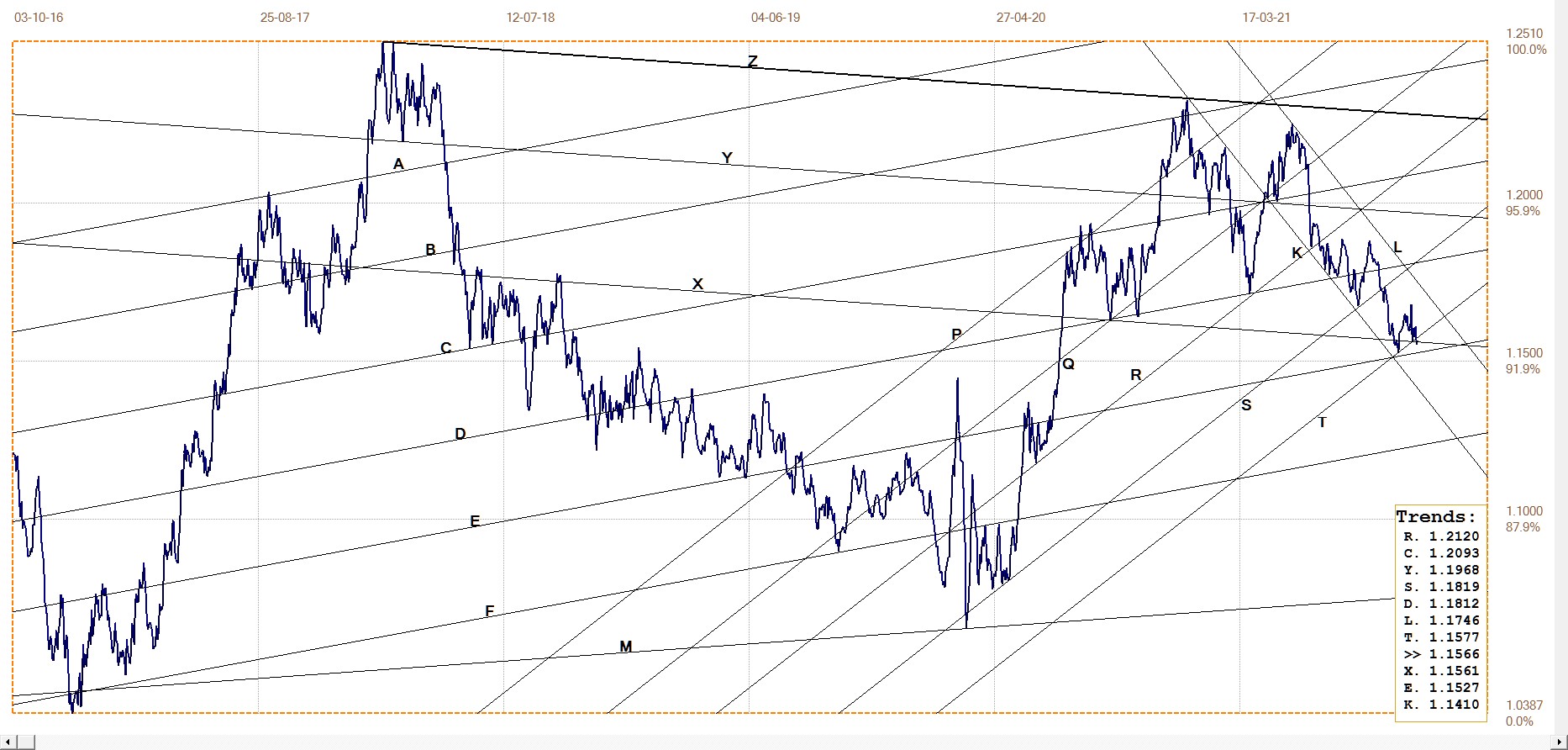

Euro–Dollar

Now, after a marginal break below channel ST, the euro is again testing the support of line X. It acts as a sign that the new dollar strength is still largely intact. A break below line X has the support along line E as a backstop, but even so the euro seems vulnerable at the moment. Under the current circumstances a stronger dollar is most welcome for the US; it acts as protection for both Wall Street and the Treasuries.

The euro could rally again off line X, but it would have to recover into its bull channel ST before a stronger euro will become a realistic option.

Euro–dollar, last = $1.1566 (www.investing.com)

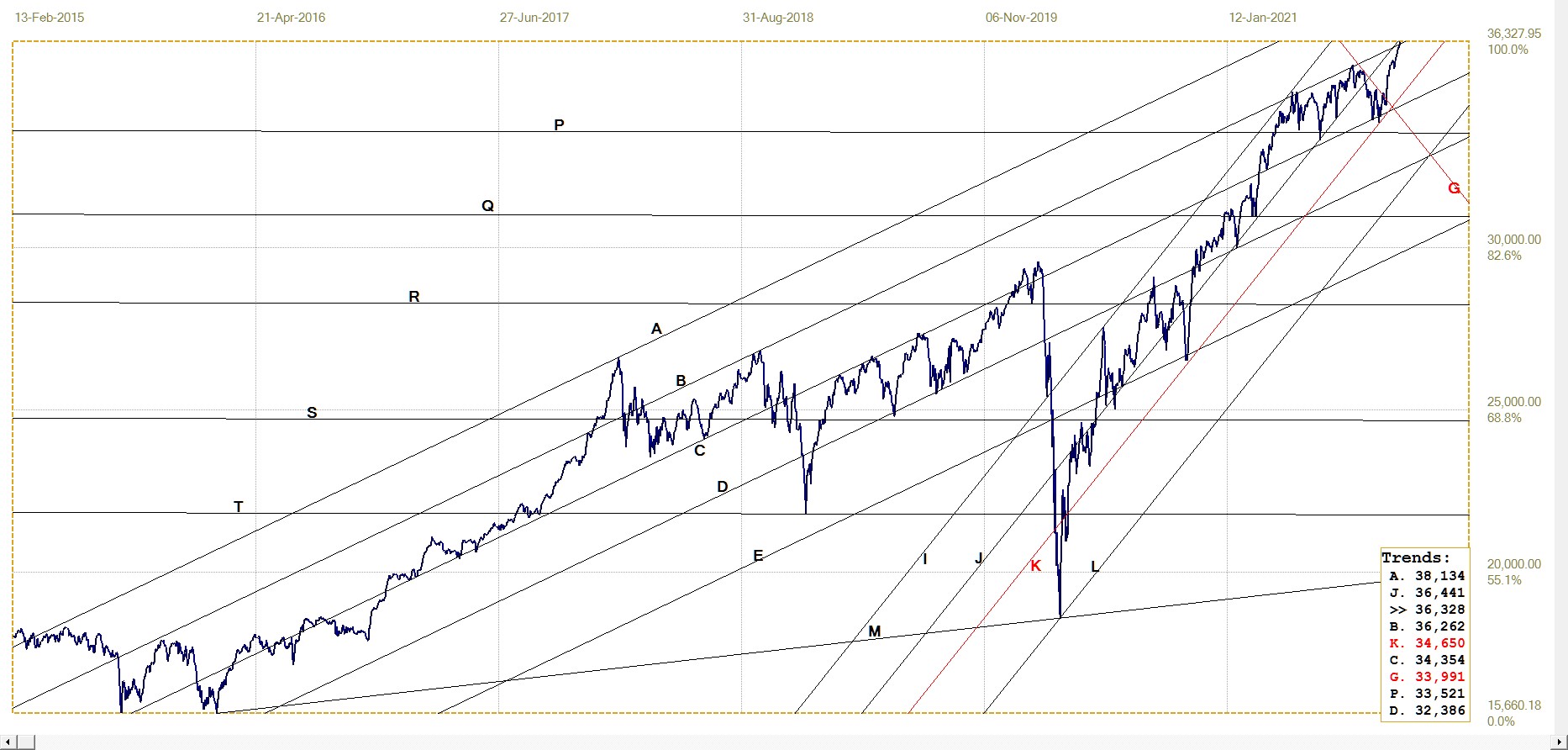

DJIA daily close

On Friday the DJIA closed at yet another all time high. With the Dow30 PE at 42.6, one can guess room for more increases are limited. If money printing continues, the stock market can spike still higher, but that would then signal even higher inflation to come. On the other hand, a significant correction now, should it happen, would be more difficult to stop and turn around than it was back in 2009, even if the amount of money this will cost today will be less than what had to be printed 12 years ago.

DJIA. last = 36327.95 (money.cnn.com)

Gold London PM fix – Dollars

Gold price – London PM fix, last = $1801.85 (www.kitco.com)

The price of gold had been worth no more comment than a “Ho-hum” for some weeks now, at least until Friday when the price jumped more than $20 to close the week well above the $1800 mark. The London PM fix held within downward facing megaphone UVW at $1808, but the close in US trading was about $10 higher on a break above the megaphone. If the gold price can hold and extend that level in the week ahead to add to the recovery, November might not be a too bad months for the yellow metal.

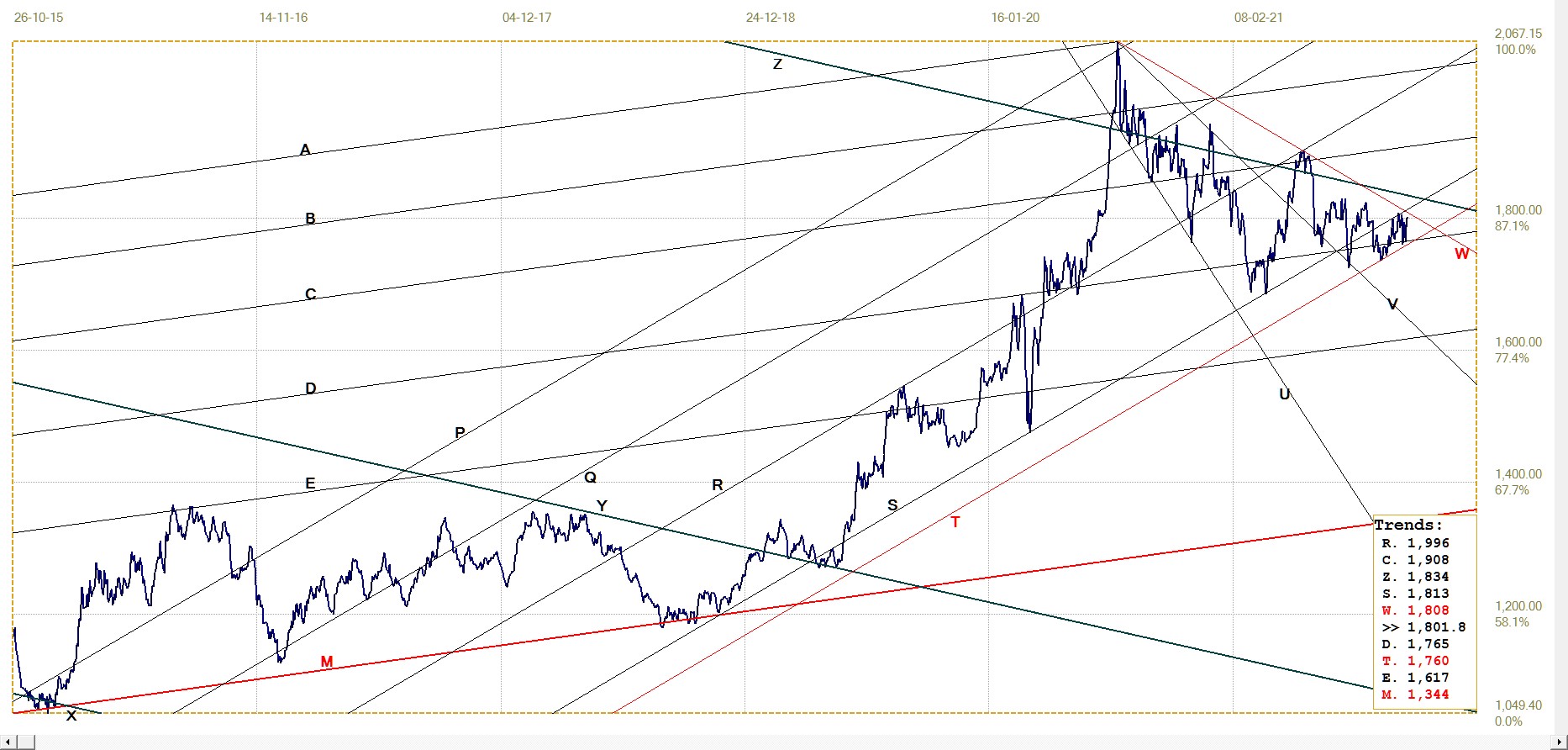

Euro–gold PM fix

The weaker euro last week favoured the euro price of gold, which also received a boost from the better dollar price on Friday. The recovery back into bull channel RS is a positive signal which needs to be confirmed by further gains to remain within that channel. A break to above line Y would be a bonus.

Euro gold price – PM fix in Euro. Last = €1562.92 (www.kitco.com)

Silver Daily London Fix

The price of silver as per the London fix managed to break above the $24 level on the last two trading days of October, but then failed to hold that break into November. After losing 40c by November 3rd, the price edged higher again, to reach a London fix at $23.82 on Friday. During US trade silver joined gold in a surprise rally that had silver at $24.15 at the close. The price has to improve on that performance this week to inspire any confidence.

Silver daily London fix, last = $23.82 (www.kitco.com)

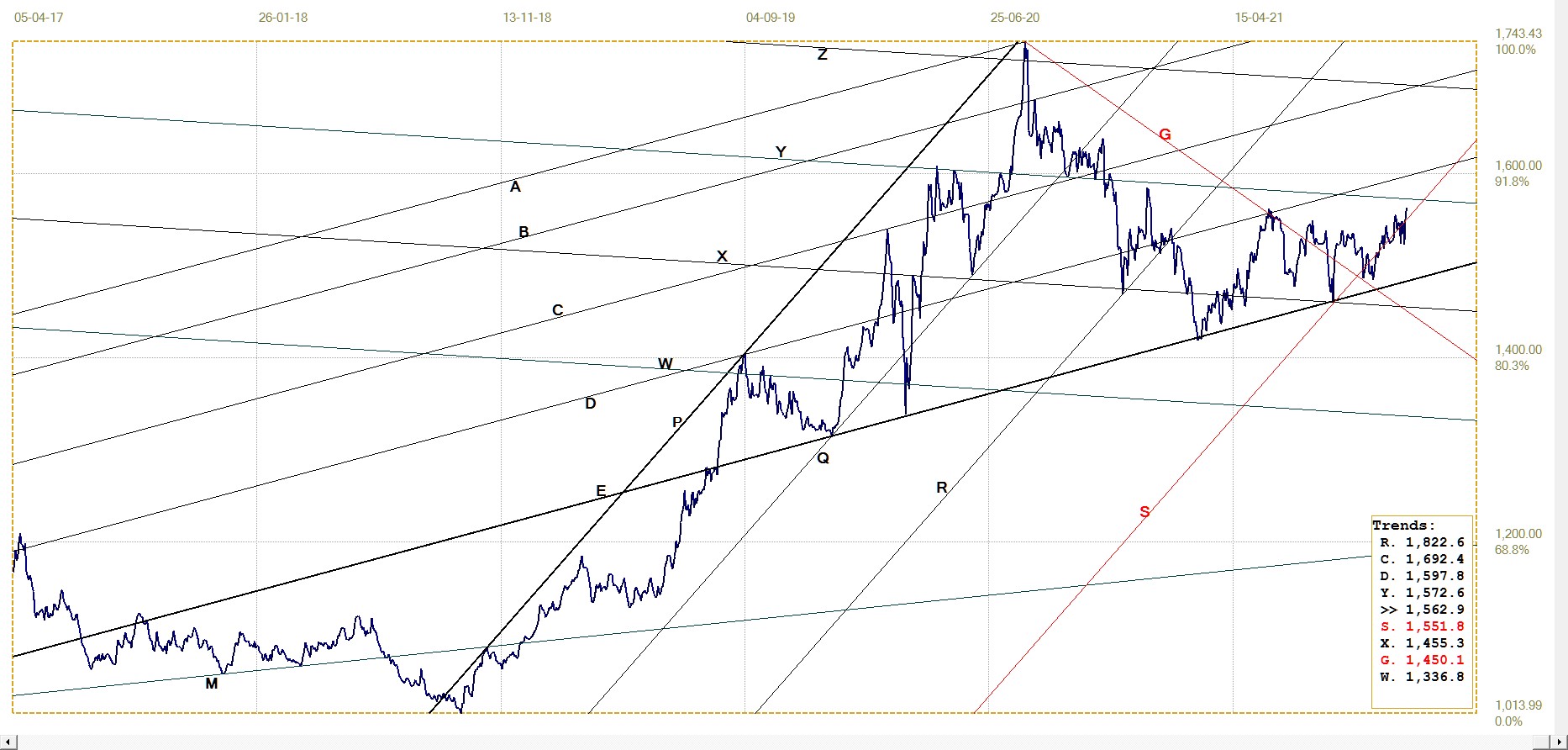

U.S. 10–year Treasury Note

10–year Treasury note, last = 1.455% (Investing.com )

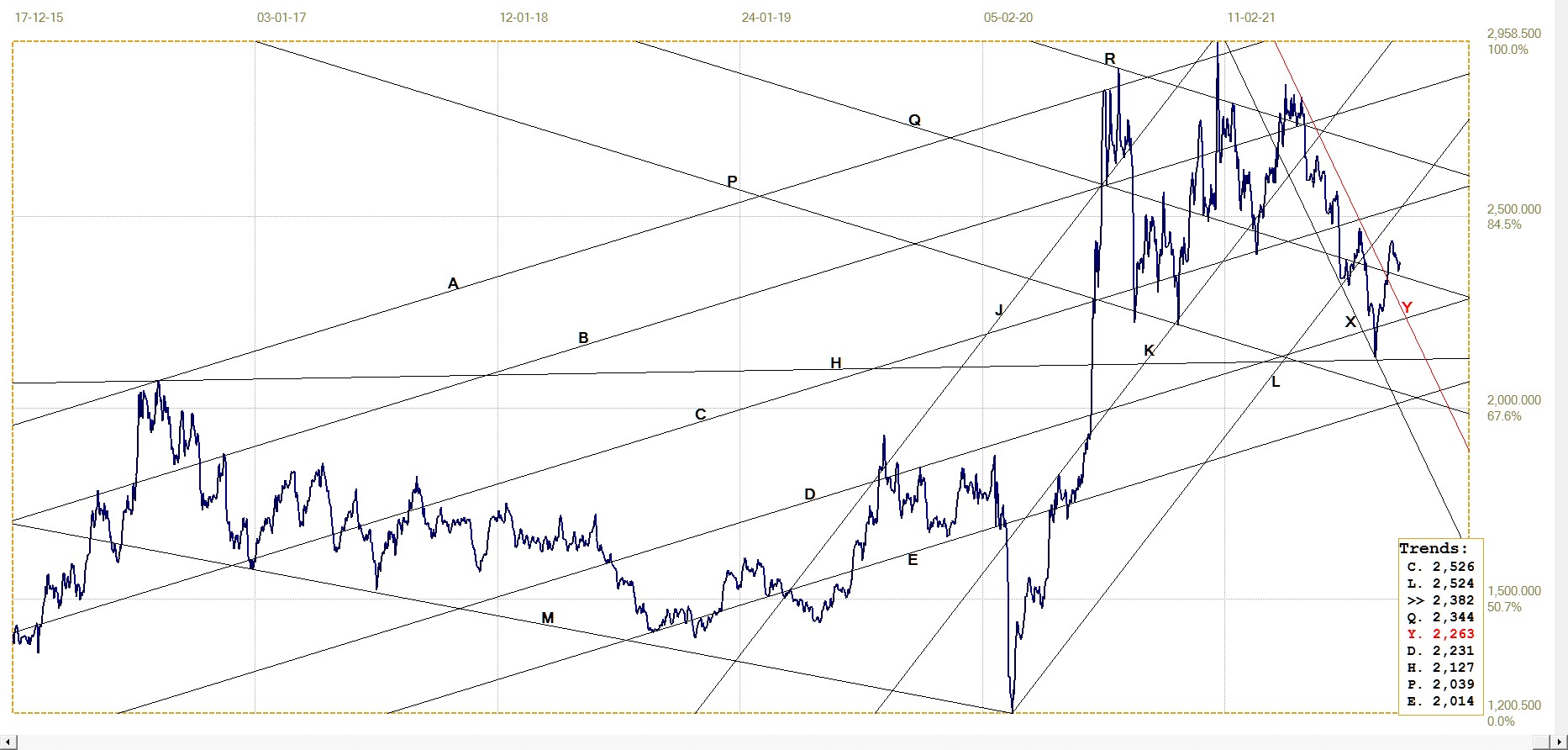

Whether it is in reaction to the firmer dollar or a change in expectation of what the inflation rate will report, the rally in the bond market is counter-intuitive in terms of what could be expected for the longer term on the basis of fundamentals. Given the volume of money printing and the increased issuance of Treasuries, the reversal lower from just off line A by the yield on the 10-year Treasury note is a surprise.

The new break below channel KL so shortly after having recovered from an earlier break lower, as well as the break below line Y, promises lower yields while the breaks hold. It remains to be seen if the move anticipates a lower CPI report this month.

West Texas Intermediate crude. Daily close

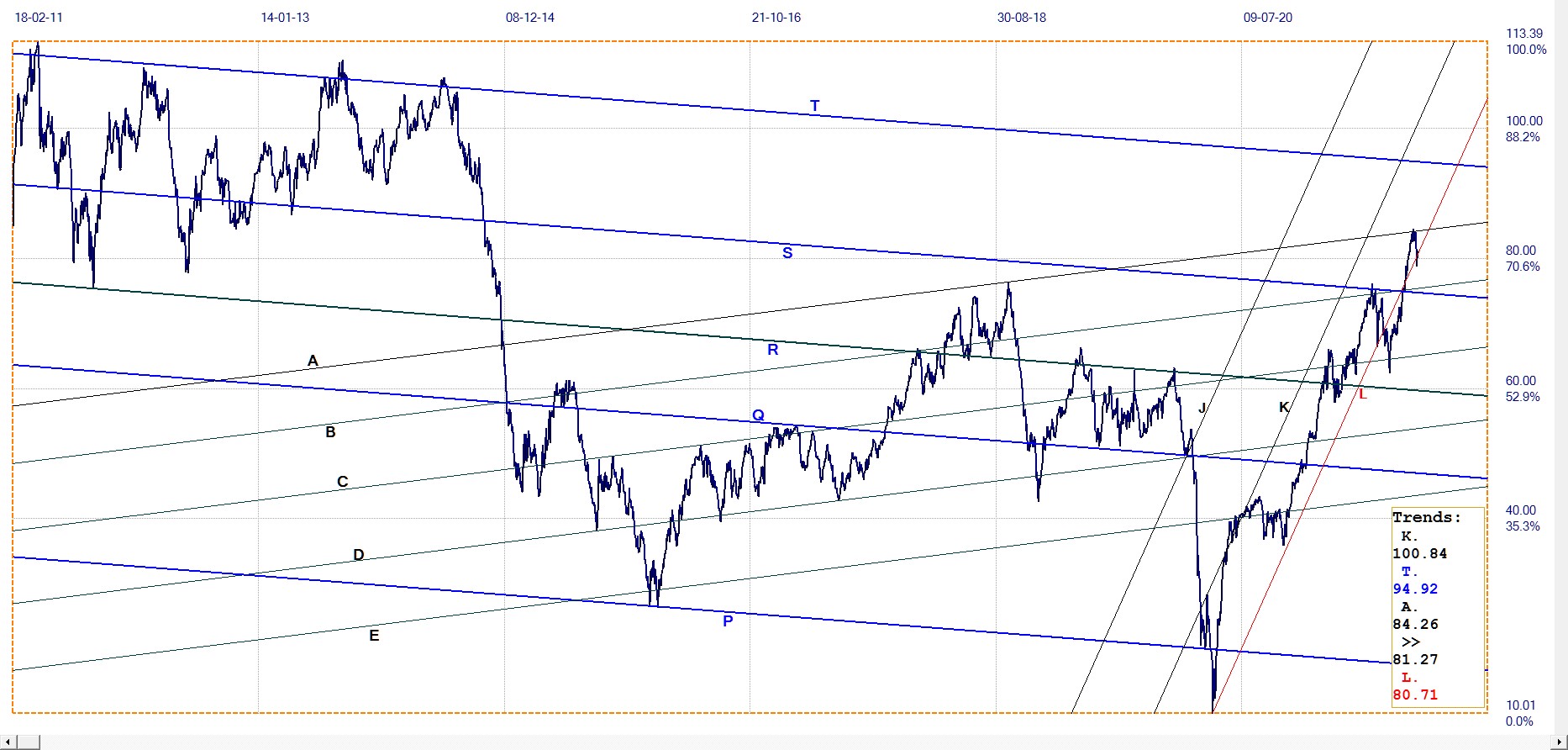

WTI crude – Daily close, last = $81.27 (www.investing.com)

Line A is a strong technical barrier and the reversal lower could have been expected, but not to the degree of also breaking lower from steep channel KL, even if the break is only marginal so far. This week should show whether what happened resulted only from a little over-enthusiasm in the energy market or if a new bearish trend is being established.

© 2021 daan joubert.

********

More from Gold-Eagle