Is it? Or isn’t it?

Wall Street under pressure with the DJIA down 394 points and the biggest one day decline since the Brexit surprise. Is this going to “IT”, the start of the Big Bear? Or are the PTB going to go all out this week to clap the paddles to the stock market to get its bullish beat pumping again? Undoubtedly, they will attempt to do so. So the real question should not be what is going to be done, but will there be success?

At time of writing it is not yet clear why Wall Street slumped. Is it the North Koreans with their nuclear warheads that suddenly gave the West a bigger scare than when they did the same things some time ago? Is it inside knowledge that a major bank will announce over the weekend that it was rescued at about 5% of its closing price on Friday, as has happened before some years ago? Or is it just another of the ‘usual’ hiccups in the DJIA, similar to half a dozen or more during the past decade, that is simply a brief way station on the way higher?

Lots of questions, with this week expected to bring some answers. The time when it was possible to use fundamentals for market direction is long past. Changes day to day vary, with probabilities biased towards bullish when one considers the DJIA or the US dollar or Treasury yields – even the official statistics on the economy display a long term bullish bias, despite widespread concern about the fundamentals. While markets are kept bullish to ensure a happy feeling on Main Street, the economy has to appear growing, but not so strongly that the Fed will actually have to do what is near a daily warning: i.e. that rates will rise at the next FOMC meeting.

US Economists and other commentators on the economy allied to the establishment for decades used to explain how command economies in Russia and in China were on a path of self-destruction. Then, before it really happened, both these countries realised the trend and bootstrapped themselves out of the economic mire. Yet these same commentators have failed to notice – or out of loyalty just kept quiet – about a similar trend to a command economy in the US that is already far advanced.

Could it be the Fed wants to demonstrate that they can achieve what the Russians and the Chinese failed to accomplish – to establish a flourishing command economy where everyone enjoys the good life? If so, they are not doing so great, so far.

At time of writing it is a day of remembrance for Americans and many other people. One can only hope it does not repeat.

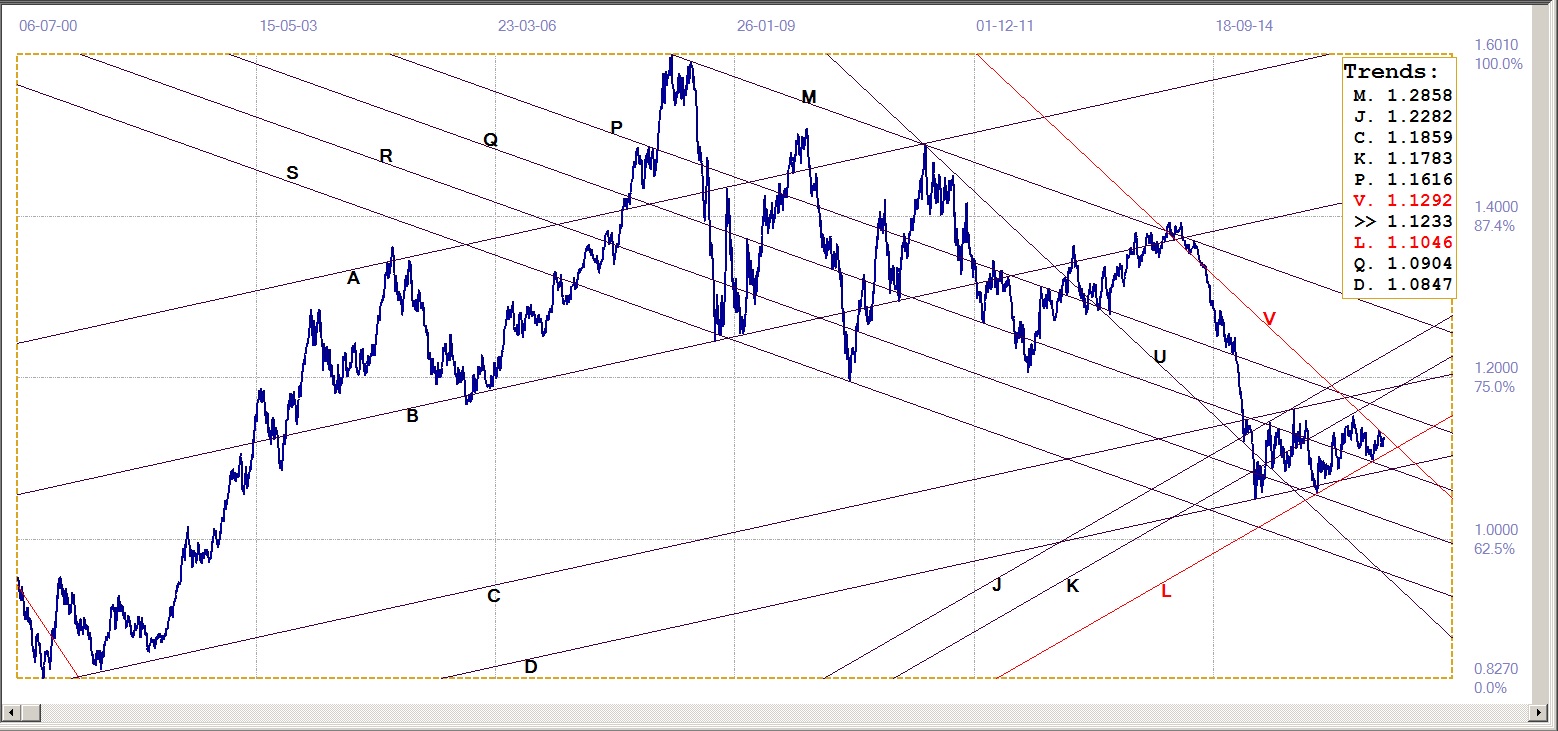

Euro-Dollar

The post-summer season has started and the rebound off line L ($1.1046) seems to favour a break above channel UV ($1.1192) to resume the bull market. Of course, a surprise event in Europe could throw a spanner in the works to result in a break to below channel KL and a new bear phase. However, given that the dollar started the new season with weakness, a bullish euro appear to be more likely – with a break above the resistance at line V to confirm.

Euro-Dollar, last = $1.1233 (www.investing.com )

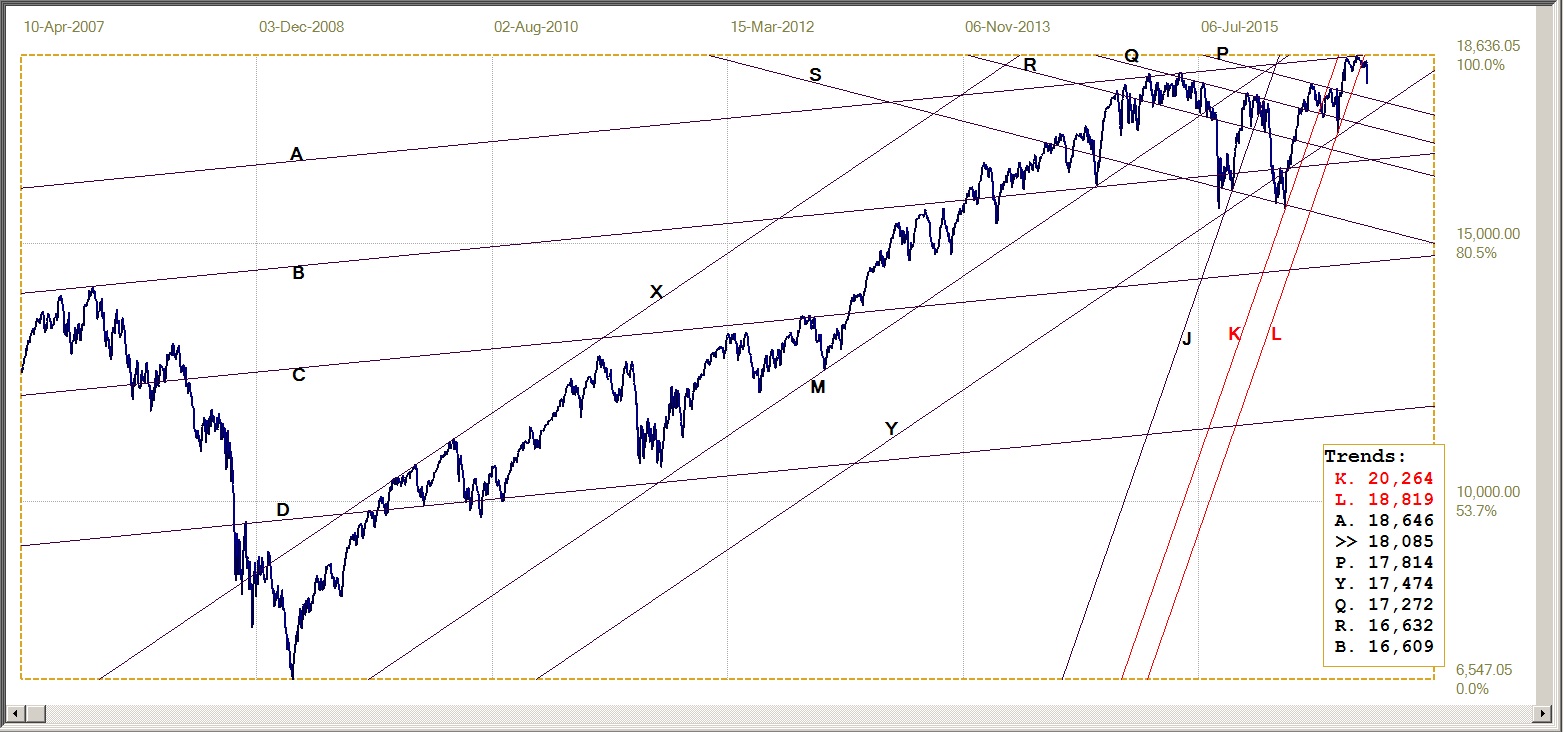

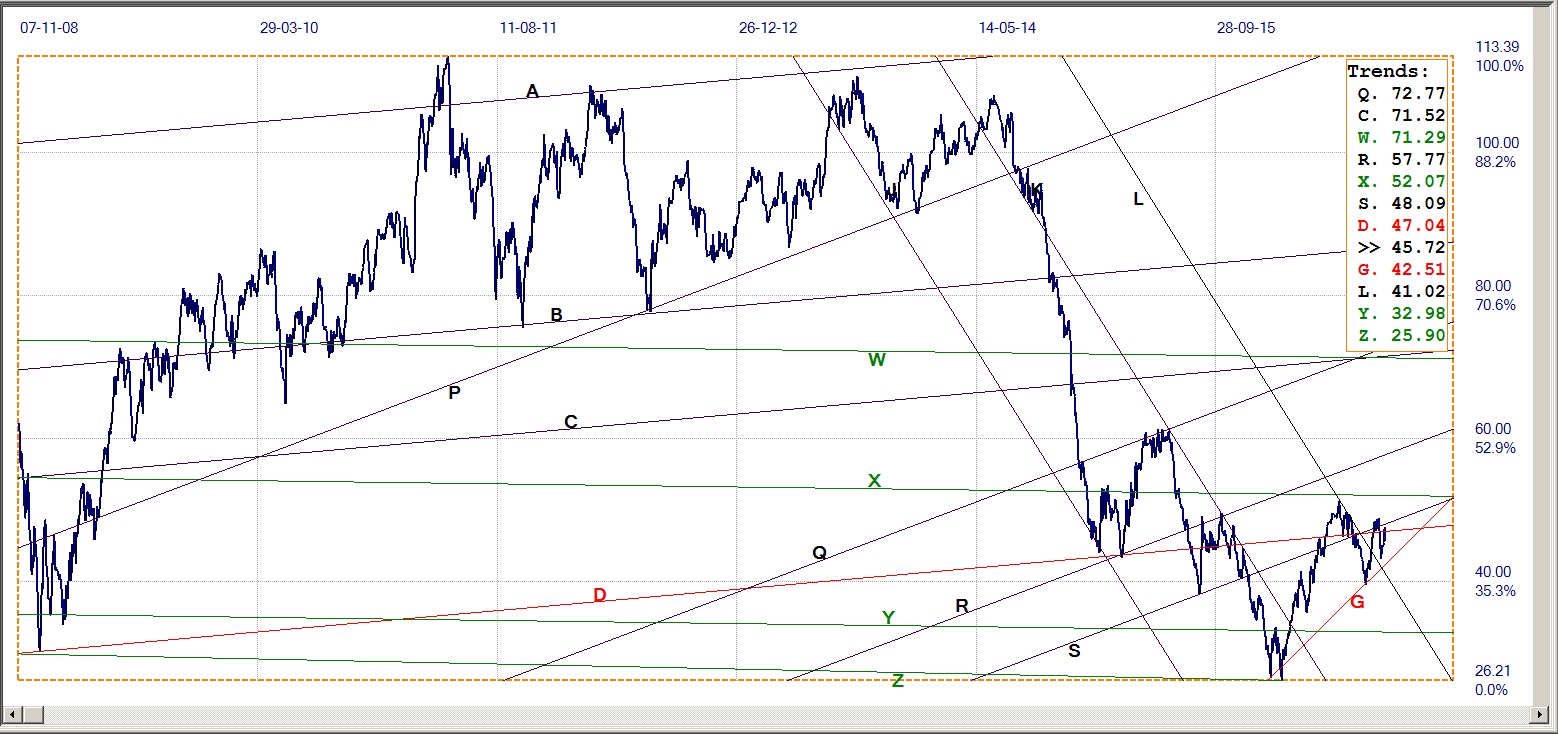

DJIA

DJIA, last = 18085.45 (money.cnn.com)

The DJIA completed the close double top along line A (18 646) and then struggled to remain in touch with support at the bottom of steep bull channel KL (18819). It proved not possible to do so and was followed by Friday’s steep decline of almost 400 points. First confirmation that the move lower is not merely a small blip in the sideways to still bullish market, would be a break back below the support at line P (17814) to return to bear channel PQ.

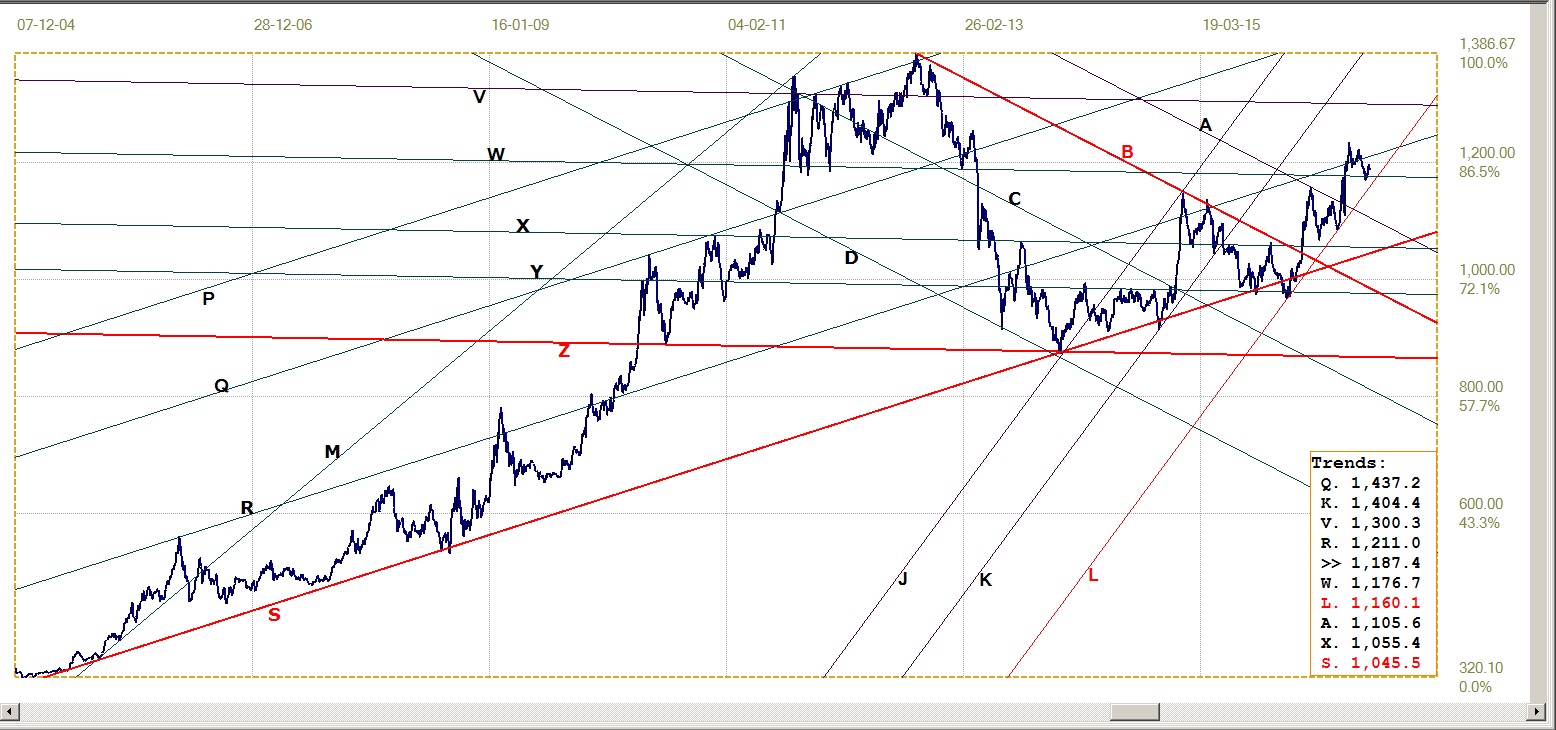

Gold PM Fix - Dollars

Gold price – London PM fix, last = $1330.85 (www.kitco.com )

September is reported to be the best month for gold over many annual cycles. The reason for this could be the combination of the end of summer, when the doldrums season is over and people return to the realities of life, and because after OPEX, FBD and NFP at the beginning of September there is quite a gap to end November before there is again a major delivery month for silver and gold, if I understand the CME tables correctly.

That creates an ideal situation for short sellers to create a very lucrative situation – selling contracts in a consistently rising market to suck in the bulls, fattening them up and then leading them to slaughter in die December abattoir. At the same time building up stocks of the metals to ensure that December will see a massive attack on the prices with ample reserves to make that possible.

It is therefore expected to see a break above the $1350 price ceiling and also above resistance at line Q ($1358) to confirm the trend. It might be a little too optimistic to expect a break above the next resistance, at line B($1466) or even a return to the older bull channel by breaking above line V ($1476), before the end of 2016; but that possibility should not be left completely out of consideration.

Gold PM Fix – Euro-Gold

Both the gold price and the value of the euro improved last week. A stronger euro places the euro price of gold under more pressure, but as the chart shows, the price of gold has outperformed the euro against the US dollar – with the result the euro price rebounded from just off the support of line W (€1177). Line W is repositioned so that it is now close to the centre of channel VX, which is the more appropriate location for a preferred gradient.

This more positive outlook after the rebound higher has to be confirmed with a clean break above the resistance at line R (€1211).

Euro Gold Price – PM Fix in Euro, last = €1187.4 (www.kitco.com)

Silver Daily Fix Chart

Having reversed higher off support at line Z ($18.36), silver is still holding clear its key support at the lower boundary of bull channel KL ($17.82), similar to what the euro price of gold has done. It is nevertheless still quite a distance below a possible recovery back into the previous and steeper bull channel of which line V ($20.99) was the lower boundary. Should the rising trend continue, as is expected given the discussion of the gold price for this time of the year, the rising trend should confirm with either a break back above line V or a break above resistance at line C ($21.15) depending on how steep the rising trend happens to be. Line R ($22.67) – support of the large pennant that had developed earlier – a is however the main resistance that has to be penetrated to set the new bull trend firmly on course.

The behaviour of the silver open interest during the recent extended attack on the price of silver holds good promise for the future. While there was a sell-off as longs closed their positions, providing short players with some profits and reducing their overall short position, the open interest soon picked up again and is now just more than 10% below the recent all time highs. The threat this poses to the shorts is not really diminished from what it had been and could easily increase again during the coming months.

Silver Daily Fix, last = $19.41 (www.kitco.com )

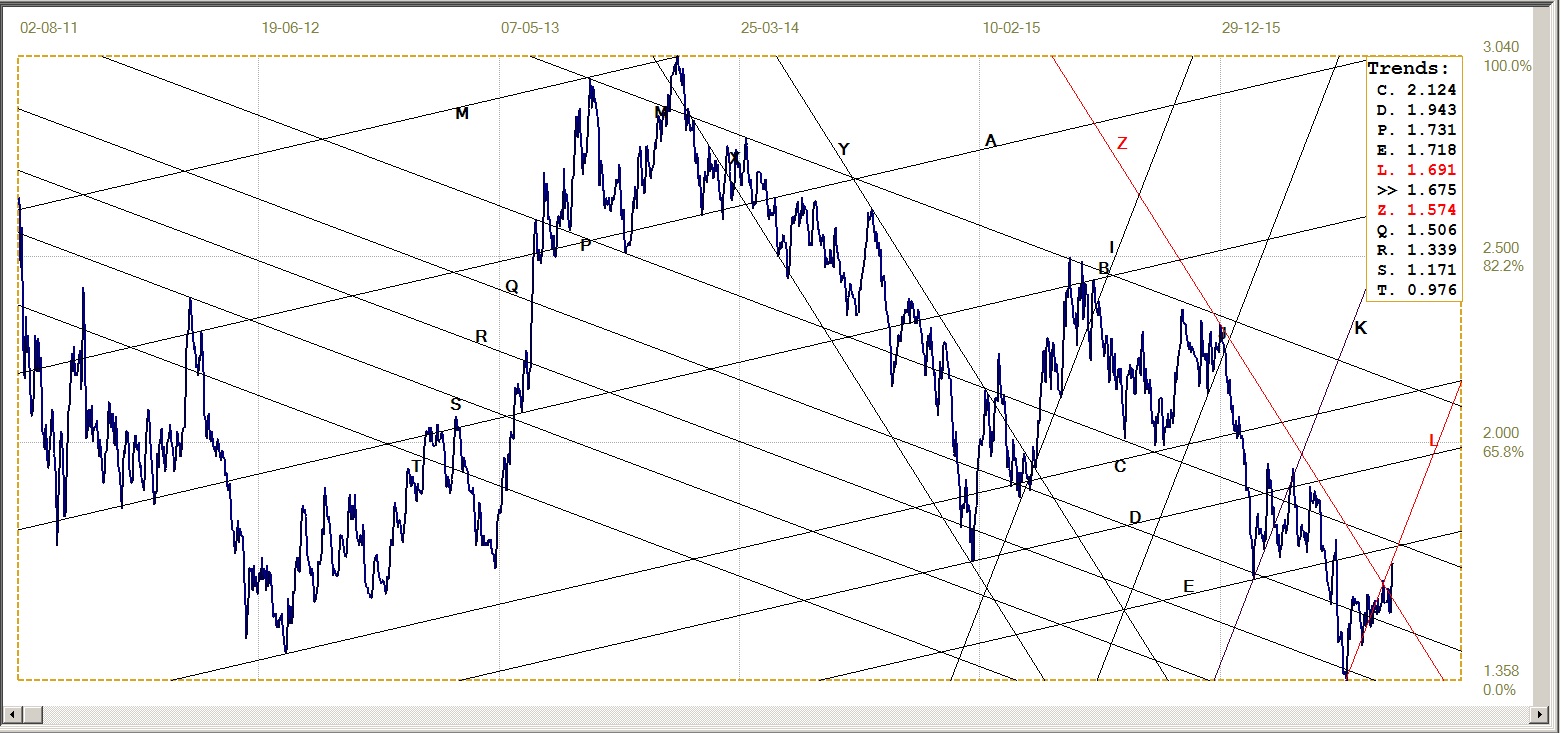

U.S. 10-Year Treasury Note

The yield on the US 10-year Treasury Note moved higher out of a previous volatile consolidation phase only to settle in what became another consolidation around the slightly higher level near 1.6%. This kept it at first close to the lower boundary of steep bear channel KL (1.691%) and the top of bulls channel YZ (1.574%). Early last week, when the threat of a technical break above support from line Z became imminent, the market suddenly turned bullish to remain well within bull channel YZ. By Wednesday the yield was down to 1.539% and it looked as if the bull had made a come back.

The low value on Wednesday was the end of the rally. Thursday saw the yield close at 1.616%, back in the range around 1.6%. It is not clear whether whatever event triggered the swoop up to 1.675% on Friday saw already having effect on Thursday before the Friday sell-off, or whether it was merely a return to the 1.6% range.

The move higher on Friday is the highest yield since the Brexit associated rally on 24 June and, with the situation in the UK and in global markets relatively stable, it is what happened on Friday that spooked the market. This week should show – as for Wall Street and the dollar – whether the new bearish instability is here to stay or whether it is no more than a bearish flash in the pan.

U.S. 10-Year Treasury Note, last = 1.675% (www.investing.com )

West Texas Intermediate Crude. Daily close

The effort two weeks ago to hold above the new support at line D ($47.04), slipped late last week to have the price of crude bottom just short of the support at line L ($41.02) and rebound higher. With daily swings in both directions, crude managed on Thursday to get back above the support of line D, only to have the market shake up on Friday send the price down to $45.72 again.

With this fall in the price, crude has a bearish to sideways bias at best while holding below the resistance of lines D and S ($48.09). Support is at line G ($42.51), well below Friday’s close, but still within reach of a further sell-off.

WTI Crude – Daily close, last = $45.72 (www.investing.com )

©2016 daan joubert, Rights Reserved

chartsym (at) gmail(dot)com