Is It A Swan? Is It Black?

What makes a black swan? A working definition would be the swan is an unforeseen event that has the impact to unexpectedly reroute a majority of major markets in a negative way. If an event was not foreseen, but only affects a single market, it can hardly qualify as a black swan; perhaps only be a black gosling that matures into a swan if the market that was badly affected happens over time to be just the first of the tumbling dominoes. The serial collapse of Bear-Stearns, Lehmans and AIG in which Bear-Stearns initially almost was a non-event that the Fed Chairman thought would be ‘well contained’, is one example. What took place in the UK on Thursday was thought to be such remote possibility it had caught all but the most optimistic, or most fearful, by surprise. Time will tell if it is to mature into a great black swan.

My belief is that it nevertheless is what passes for a watershed event; one in which so many things to which we are accustomed never are the same again. 9/11 is such an event; on a more subtle note, so were the moments when the first Ford, first TV and first cell-phone rolled off the assembly lines. It required time, but these events, and many others of less obvious initial impact, have affected our lives. Whether the unanticipated result on Thursday will qualify as full blown black swan might become evident as early as this week, but over time a final Brexit, if Parliament should act on the popular vote, will radically change global economic and political aspects.

As had happened after the infamous 9/11 and the serial collapses of 2007/8, the behaviour of the markets on Friday revealed the central banks of the world collectively, with the US Fed prominent, had intervened to ensure as best they could that damage would be contained so that conditions would remain as normal as possible; without revealing how slender and vulnerable the pillars of debt on which so many great economies are balanced had become. So far they have been very successful in concealing this fragility; it is economists and others from the way out fringes who warn that those pillars are beginning to bend; as I have been doing for a decade or more.

Will they be again successful? It is an election year and as we have seen repeatedly for some months (much longer, in fact), despite less than buoyant economic news, US markets simply are not allowed to display bad news regarding the economy. The controlled slide on Wall Street on Friday clearly was designed to a) prevent a panic and b) to restrict the overall decline as much as possible. Pacifying comments over the weekend about how easy it will be to deal with the new situation and expecting much buying on the SP500 futures market early on Monday will not be a surprise and this possibly will help return markets to what passes for normalcy nowadays.

Unless. It would be a mistake to disregard the fact the mentioned slender pillars of debt might show cracks after Thursday; cracks that first enlarge into small and then into larger fissures, until the first pillar under a major financial institution or even a sovereign debt collapses. Then what happened on Thursday would be more than the arrival of a black gosling, but of a whole gaggle of grown-ups.

On COMEX, the first hours of trading on the new day – after Asian buyers had gold briefly above $1360 – was a tug of war between buyers and forces of suppression. The chart below shows the decline in the price after the early spike. On Saturday, the COMEX report revealed that the gold open interest had increased on Friday by a massive 59,397 contracts. This, after adding about 9,000 open position the previous two days.

Because of the extensive ramifications a strong and sustained bull market in gold – that drags silver along! – will have on other markets, starting with the US dollar, it is beginning to look as if the next few weeks will see the swans landing.

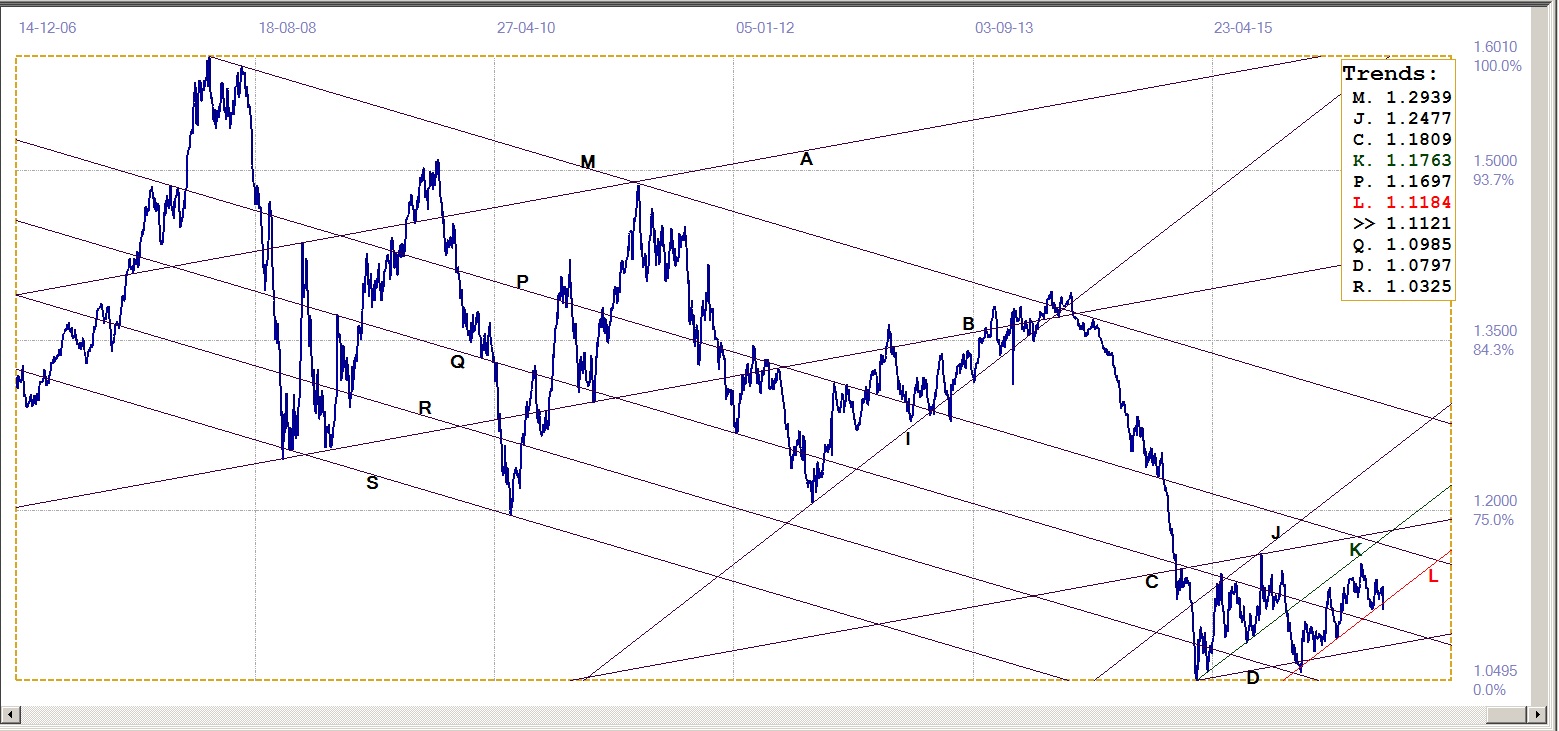

Euro-Dollar

Euro-Dollar, last = $1.1121 (www.investing.com)

Brexit has a knock on effect on the EU and the euro dropped well below the support of line L ($1.1184) before recovering partially. It now remains to be seen whether the slightly bearish close below the bull channel will be temporary only, or a sign of further weakness to come. A recovery back above line L during this week would be a resumption of the recent dollar trend, but is not given high odds unless the effect of Brexit has wider repercussion in the US.

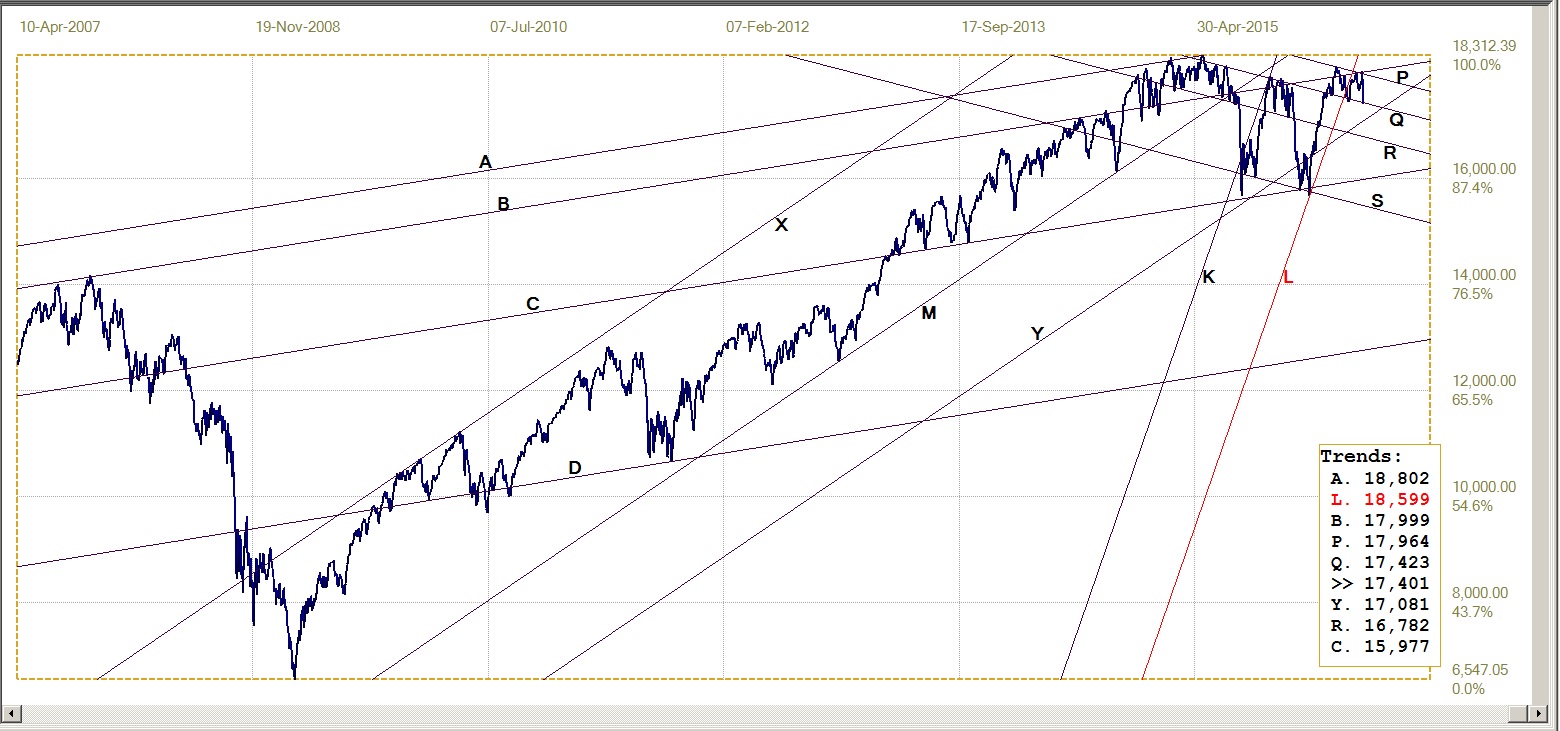

Dow Jones Industrial Average (DJIA)

Dow Jones Industrial Index, last = 17401 (money.cnn.com)

On Wednesday the close at 18011 was only a little above the resistance of lines B (17 999) and P (17964), too small to be a definite bullish signal. Then, after early warning from the futures of a 1000+ point sell off, firm support from an unknown buyer had the DJIA descend in controlled step by step fashion to close near its low for the day, but 400 points better off than what the futures initially indicated.

This week the market has to continue with price discovery – probably contaminated by some intervention – to find the correct level given all the fall-out from the Brexit vote, which is still tentative until the UK parliament has indicated whether they will abide by the results of the voting. Whether the level where the market settles will be temporary or serve as a base for the longer term, time will tell.

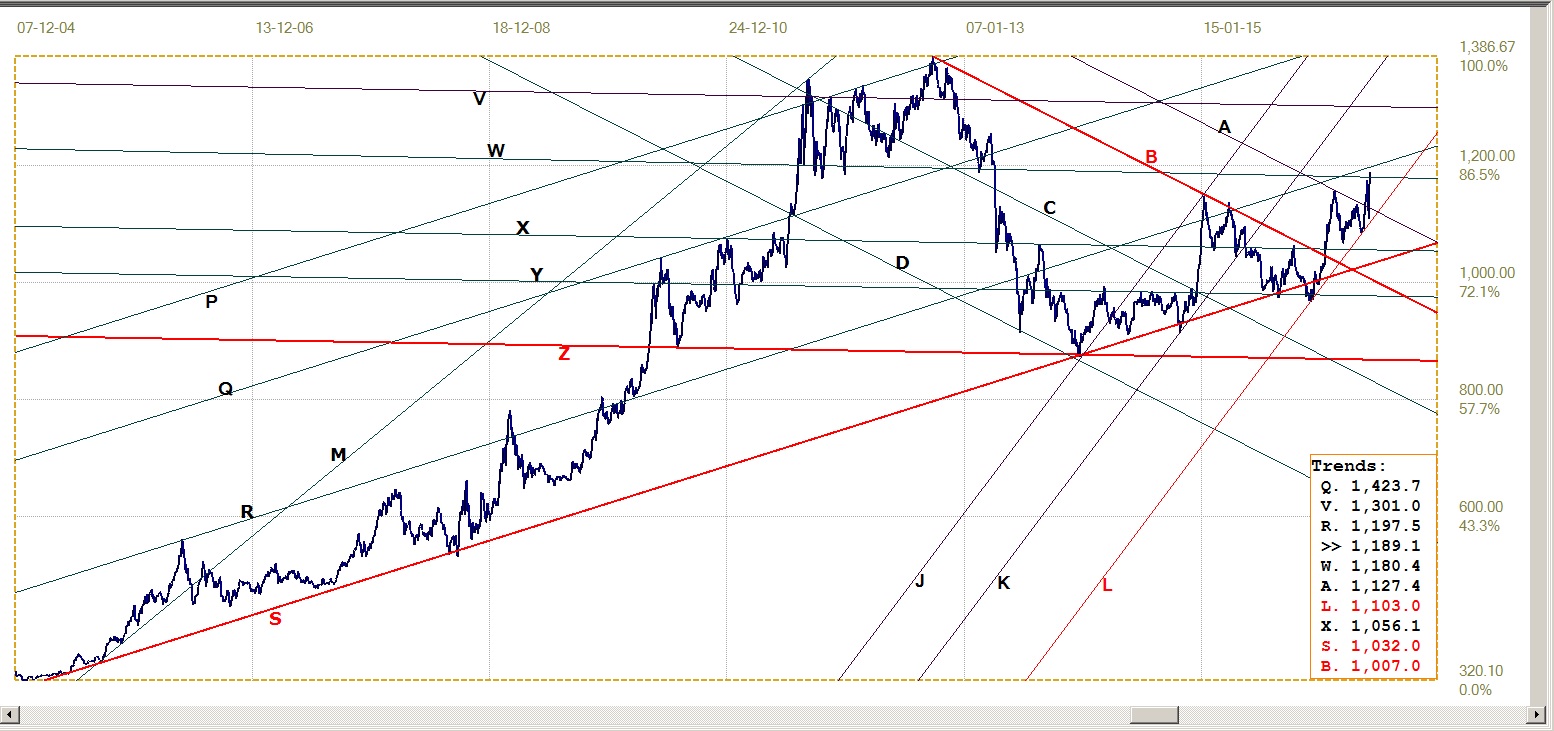

Gold PM Fix - Dollars

The price of gold started last week under some pressure that was reported to be due to disappointment in the PM market that the Brexit vote would go against the UK leaving the EU. Then, Thursday night as the vote started to swing the other way – as more rural votes were counted? – gold and silver spike steeply higher, carried by a sudden tsunami or euphoria. Of course this spike probably over-shot a realistic top, but the earlier intra-day chart and the 60 000 added to open interest shows Friday’s battle royal between buyers and sellers.

Friday’s PM fix nevertheless is a new recent high, again extending well above line Q ($1291) and also the $1300 level. Line V ($1346) is the bottom of the previous and steeper bull channel that had failed to contain the price. A quick recovery back into that channel will be confirmation that the initial steeper bull trend is back on track.

Gold price – London PM fix, last = $1315.50 (www.kitco.com)

Gold PM Fix - Euro

The euro lost ground against the dollar as a result of the Brexit voting. That helped the euro price of gold to recover back above the resistance at lines A (€1127) and W (€1180). Further weakness for the euro this week is possible should Europe be considered much weakened by the UK possibly departing the EU community in due course after the negotiation period. Should it combine with a firmer dollar price of gold, the near future could see the euro price of gold breaking above resistance at line R (€1298) to give a buy signal of some importance in the current analysis.

Germany in particular among other European countries have been buying PM metals at a much higher rate in recent months and what happened on Thursday may well give wider impetus to the safe haven buying in Europe, joining China and India and other countries. The odds that gold in dollar terms will help drag the euro price higher are therefore thought to be improving.

Euro gold price – PM fix in Euro, last = €1189.1 (www.kitco.com)

Silver Daily Fix Chart

Silver daily fix, last = $18.04 (www.kitco.com)

On Friday morning, silver had its first London fix above the $18.00 level since early in 2015. As the day continued, silver followed gold lower and it later settled quite a bit below the level of the fix. Nevertheless, followers of silver now know that $18.00 is not an impenetrable barrier, even if the time of the fix is before its usual time of price suppression after Comex has opened later in the day.

The steep channel UV ($17.16) is the original steep bull channel followed earlier in 2016, until the big raid in May broke below its support to bring channel KL ($16.36) into play. After the rebound off line L at $15.98 at the beginning of June the steep recovery has now broken back into the steeper bull channel to raise prospects of a more steadily rising trend for silver.

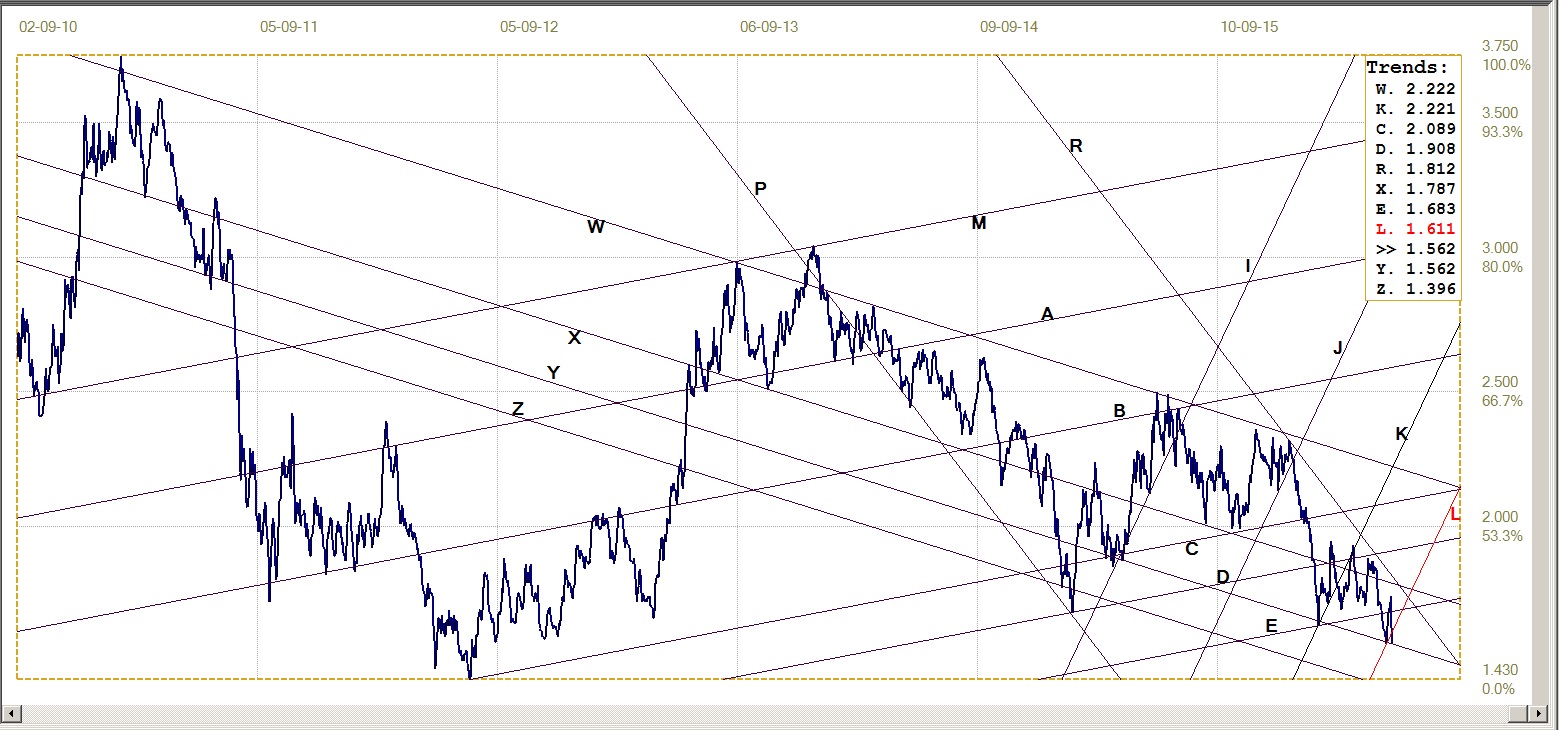

U.S. 10-year Treasury Note

U.S. 10-year Treasury note, last = 1.562% (www.investing.com)

The 10-year ended May with a bearish trend, but despite a firmer Wall Street there was a steady flight to the traditional safe haven right after the first day of June. The yield on the 110-year drifted steadily lower, ending on 9 June on market support at line E at 1.680%. That was when the DJIA retreated again off 18 000 and a flight to safety started that carried the yield below line E.

On Friday, after the Brexit vote, the yield spiked lower to reach as low as 1.406%, before reversing higher again. This is a new all time low yield – or maximum price equivalent – for the US 10-year Treasury note, lower than the previous all time low at 1.430% in July 2012 and is a measure of the degree of panic that reigned in the bond market. There must have been many large players, long of the market, who saw visions of a short squeeze in the large debt sector of the financial derivatives market – something that was perhaps developing to result in the sharp downward trend in the 10-year yield since the beginning of June.

If that is so, then the short squeeze could still be on after what happened Thursday and Friday.

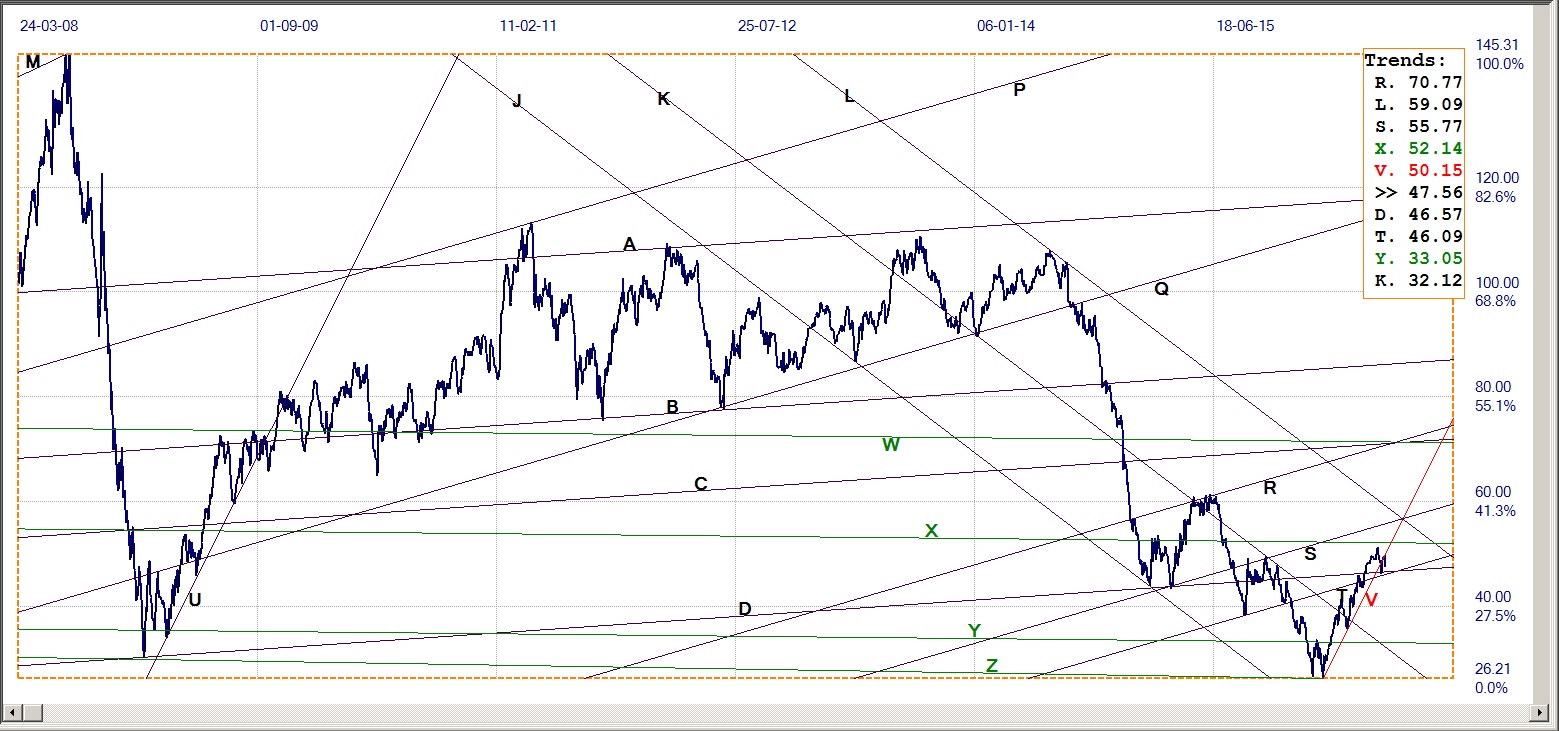

West Texas Intermediate crude. Daily close

WTI crude – Daily close, last = $47.56 (Investing.com)

After the failure to permanently hold the recent rally above the $50 level, signs that demand is still less than the supply, kept the price of crude back to below $50/bbl and in the process broke below the steep support of channel UV ($50.15). Events in the UK and in Europe may not have immediate or direct effect on demand for WTI crude, but the rebound off support at line D ($46.57) that challenged the resistance at line V failed to extend towards the end of the week.

The break lower that is holding so far, is bearish for the near term, perhaps longer. It now all depends whether support at lines D and T ($46.09) can manage to hold.

©2016 daan joubert, Rights Reserved

chartsym (at) gmail(dot)com