A Lukewarm War

The Cold War ended with the dissolution of the USSR and for a long time afterwards the US remained the sole dominant presence in the world. Then two things happened to begin to change the world order. First was the rise of China and over a similar time frame, the US lost traction on the road it had followed since WWII. So far, neither of these trends has gone the whole distance. But as China became stronger while the US splintered into factions, the initial vast difference in their respective global power narrowed. As a consequence, a symbiotic relationship that initially developed between them, has changed to develop more openly antagonistic stances from both countries.

Initial cooperation and interdependence have not disappeared; they are still entangled in a mutually beneficent interdependence, but the global power of China grew and the unified character of the US began to break apart, the relationship developed stresses. Throughout history, tribes, peoples, kingdoms and empires have aspired to be the top dog of their region. For each aspirant, at some point in time, it meant war. It needed to enforce its dominance by battle. In effect this ended with WWII, when the use of a nuclear weapon meant that later conflicts had to be conducted by means that would not bring mutually assured destruction.

After WWII we had the Cold War. The major adversaries each had an own sphere of influence, with minor shooting wars breaking out at their peripheries where physical or ideological borders brought them into contact. But the main opponents refrained from shooting at each other, from turning the Cold War into a Hot one, until the one fell apart because Reagan played the biggest bluff of all time – Star Wars.

Star Wars, as envisioned and promoted, would give the US the Iron Dome against missile attack that Israel has been demonstrating the past week or two. The USSR could not trust the US scientists that were saying it could never work as envisioned by Reagan and its proponents. They either had to build enough missiles to exhaust the defence, as Hamas is trying to do, or complete their own Star Wars program. Neither of which their economy could support…and so Gorbachev et al selected a third option, in effect making peace. Which led to the break-up of the USSR.

The economic entanglement between China and the US changes the way the new battle for supremacy has to be conducted. While ICBMs are still around, these are no longer the main threats or weapons being deployed. The battles also do not employ guns and cannons and tanks, planes and ships; both opponents – with Russia mostly as observer and possibly a potential ally – have long been working hard to develop electronic and digital and biological methods and deterrents should the relationship degenerate into actual warfare. But the main confrontation and the one that is likely to be conclusive, as happened between the US and the USSR over Star Wars, is on the economic front.

As the USSR and the US demonstrated, when it comes to an economic confrontation, bigger is really better. Other factors to contribute to economic victory are innovation, education, unity and commitment. China was of little global consequence when 90% or so of their population were mainly engaged in agriculture. But in the 1980s after Mao Sedong, Deng Xiaopeng changed the nation’s course drastically. Having Hong Kong as example of the success of free enterprise, he started pursuing a similar path for China. Initial progress was slow, in part because of lost momentum in education.

However, by the late 1990s and with the free enterprise zones beginning to flourish, China geared up – assisted by measures implemented during the Clinton years that would shift the bulk of the US manufacturing base to countries with low labour costs, with China getting ready to provide exactly that labour pool. The symbiosis that then developed, made China grow a much larger and richer economy, while keeping US inflation low and increasing its dependence on China.

Recognition that China with its 1.3 billion people presented a threat to the US, has been around for some time and among other things prompted Trump to stand for president and work to bring much of US manufacturing back home. It appears that like so many other Trump innovations this one has also been scrapped, to be replaced by attempts to pressure China with a more aggressive stance in the South China Sea and acting as a patron of Japan and Taiwan in their disputes with China. It remains to be seen how effective this will be when push gets to shove.

The outcome is likely to depend on which one retains or achieves economic dominance during the next 5 years or so. The US workforce – and thus a measure of middle class – is about 220 million out of a population of about 320 million. Of China’s population of 1.3 to 1.4 billion, many live in the impoverished central and western parts of the country. Yet the real middle class, almost exclusively living along the eastern or south eastern parts of the country, already numbered 400 million in 2018 and with the prospect of increasing that number to 550 million in three years – with COVID then happening to certainly shrink that number.

Yet, still, with already almost two times the US work force and with millions that could still be added. China has the advantage of widely developed new infra-structure and modern methods of manufacturing and an educated middle class population keen to be employed in advanced occupations in order to become affluent. Competition to get into university is fierce and the sciences and engineering are favoured. In the US, one finds much of the labour force unemployed even if most of these is not included in the official statistics, while the liberal arts and law are popular subjects to study. Another recent trend is for idle workers to sit at home and spend government handouts rather than look for work.

In brief, this describes some of the pertinent factors that will determine the outcome of the increasingly lukewarm condition of the battle for global supremacy. From the US side, much of it is being fought via the mass media and official statements; as if the statement ‘the world is as it is reported’ will achieve success in the confrontation with China as it did in the election battle to unseat Trump. I presume the Chinese are doing the same thing, but that they are also working hard to bring more than slogans and pronouncements to the face-off with the US.

Whether the developing lukewarm war will proceed to become a hot shooting war is not on the cards at the moment; a symbiotic relationship is almost like Siamese twins. A twin would be stupid to kill the other. However, when seriously provoked it is not so uncommon for a person in a rage to throw self-preservation overboard to land a blow that would incapacitate an enemy. Let us hope that sanity will prevail.

Basel III

The proposed Basel III ruling that bans the ability of banks and others to knowingly allocate the same ounce of metal to multiple clients is attracting much antagonism from those who favour or practice such fraud. My speculation as the reason for this new measure finds its origin in an objective of the Basel guidelines – summed up as intended to reduce the probability of a collapse of the financial system, because of a failure by a large bank or banks that could topple the first of many dominoes.

Given the semi-official practice of suppression of the precious metal prices, first of gold and then of silver as well, two things happened: first, large banks which perform the suppression have developed large short positions and second, there is a growing necessity to meet increased demand for the metals by hypothecation of up to 100 times, according to Jeff Christian. This created a vulnerability that can be exploited by an enemy with sufficient ownership and control of gold to influence the metals’ market prices. China might well be in such a position and circumstances could motivate them to use gold and/or silver as a covert economic weapon.

If this speculation happens to be close to the mark, the attempts to block the measure will not succeed at all. Consequently the end of June will be an interesting time for the US banks involved in the price suppression, with similar UK institutions then in the know about what lies ahead for them at the end of the year. Roll on July!

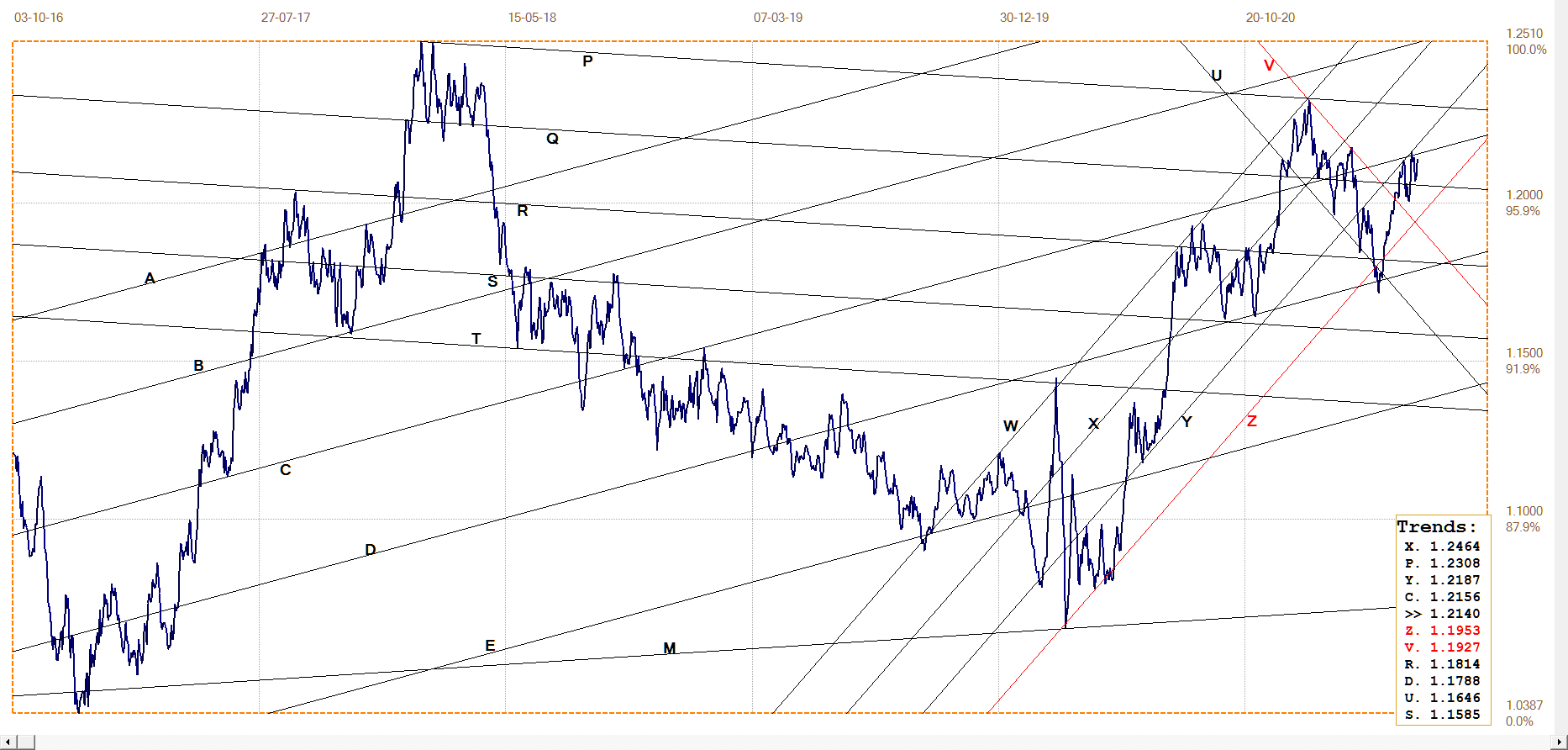

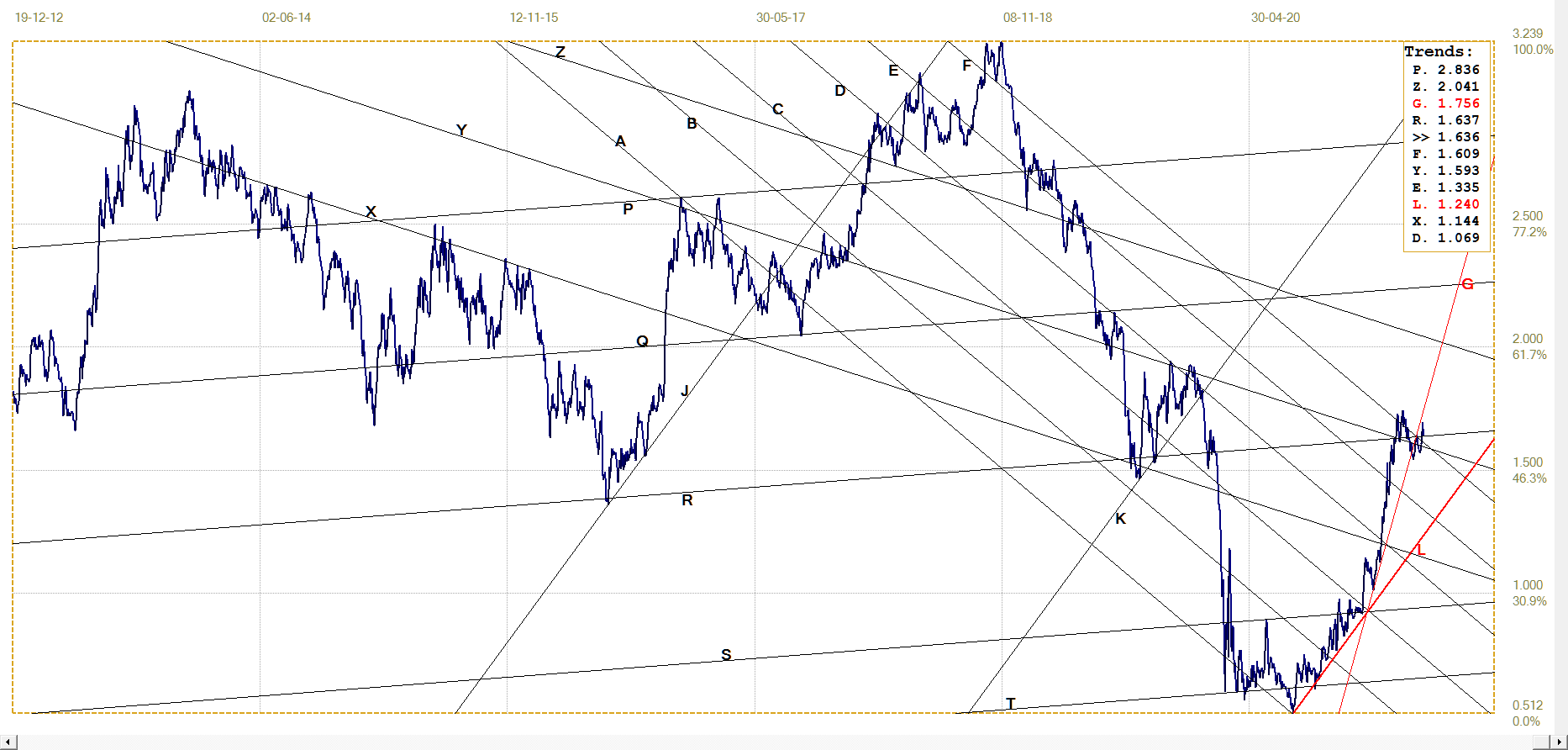

Euro–Dollar

The last rally in the value of the dollar had the euro breaking briefly below its bull channel YZ to also dip below the shallower bull channel CD. The euro recovered from the brief breaks lower to return to channel YZ and reach the top of that channel and then hold below line C. This also resulted in a break above its bear channel UV.

Since first reaching the key resistance at line C, the euro has reversed lower on two occasions, once breaking below the shallow bear channel PQ. Last week, the euro again gained some ground, but has to do more for a new challenge on the resistance at line C – perhaps to make it a case of third time lucky?

Euro–dollar, last = $1.2140 (www.investing.com)

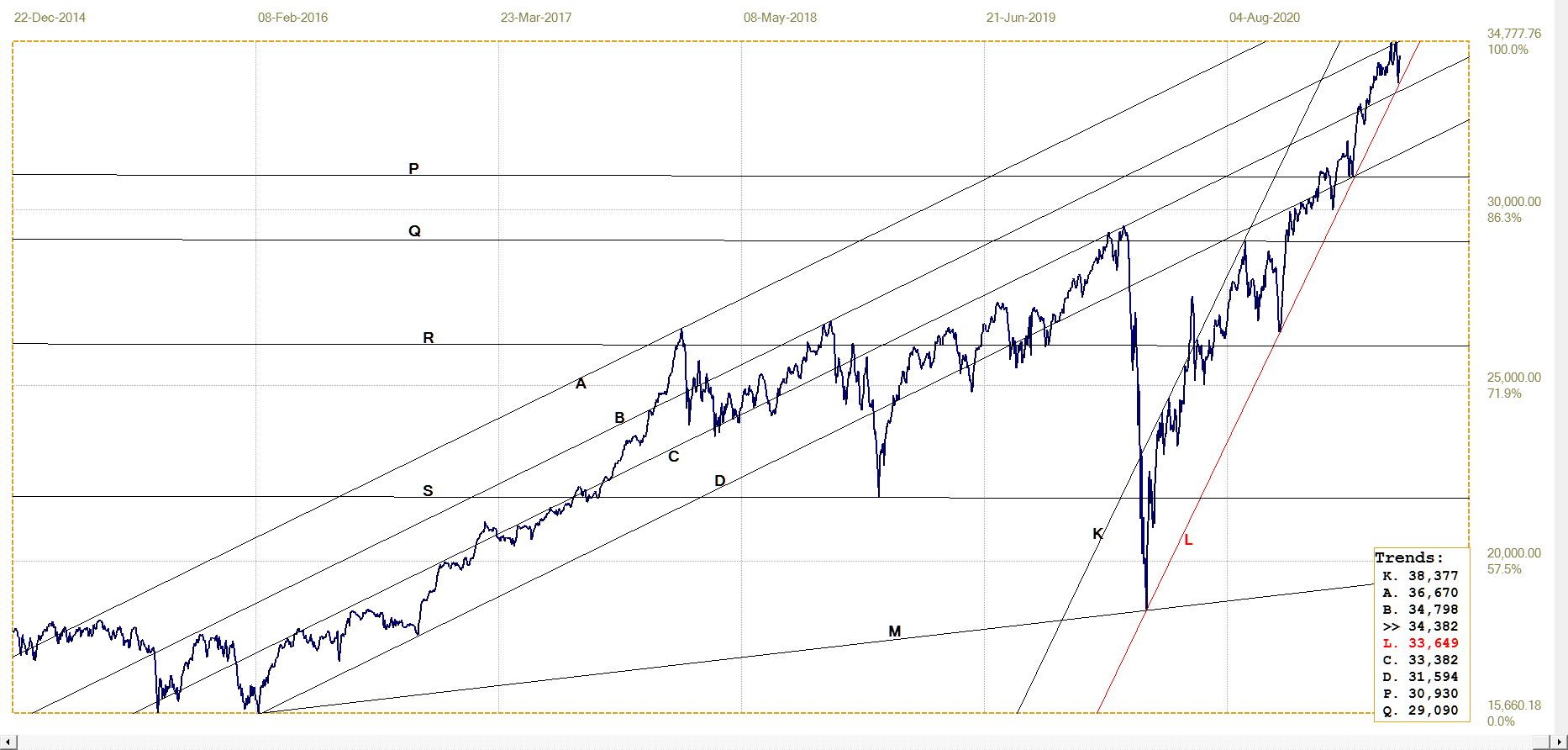

DJIA daily close

DJIA. last = 34382.13 (money.cnn.com)

The DJIA has resumed its rising trend to move higher out of a period of consolidation, only to suffer a steep reversal lower again, back to look for support at the bottom of the steep bull channel KL. It was starting to look as if Wall Street was succumbing to a bear attack, when – as is happening nowadays – the bearish position on the futures market suddenly reversed again to turn violently bullish as soon as trading opened on the floor.

On Thursday, the futures rallied from a position deep in the red to end the day with a gain of more than 400 points. Friday saw the rally extend for a total gain of about 800 points to make nonsense of bearish expectations. This week should reveal if there was a sudden fundamental change in the prospects for the economy to justify a new bullish mood, or whether it was only a pre-emptive move to stall any bear trend.

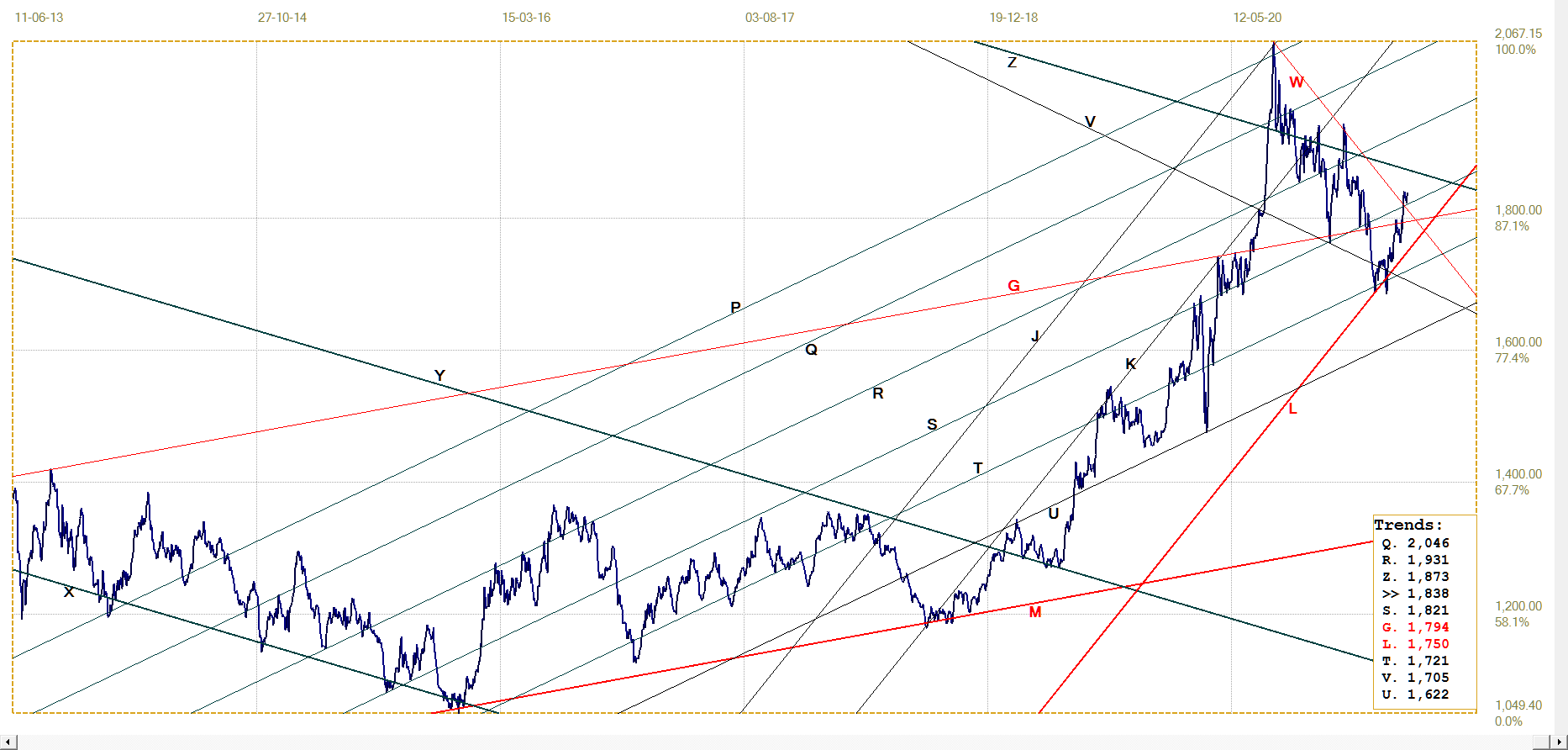

Gold London PM fix – Dollars

Gold price – London PM fix, last = $1838.10 (www.kitco.com)

The post April sell-off rally is finding it difficult to recover beyond the cap that is in place in the mid $1800s. The break above the descending resistance along line W has held so far, as did the break into bull channel RS. But that is as far as the price of gold is allowed to go.

During the past two weeks since the end of April, the Comex gold OI increased from 464 460 to 514 070 (preliminary) on Friday which saw a gain of 9539 contracts. The total increase is almost 50 000 contracts, or 500k ounces. Suppressing the price at this time can become expensive if the price should suddenly take off for some reason.

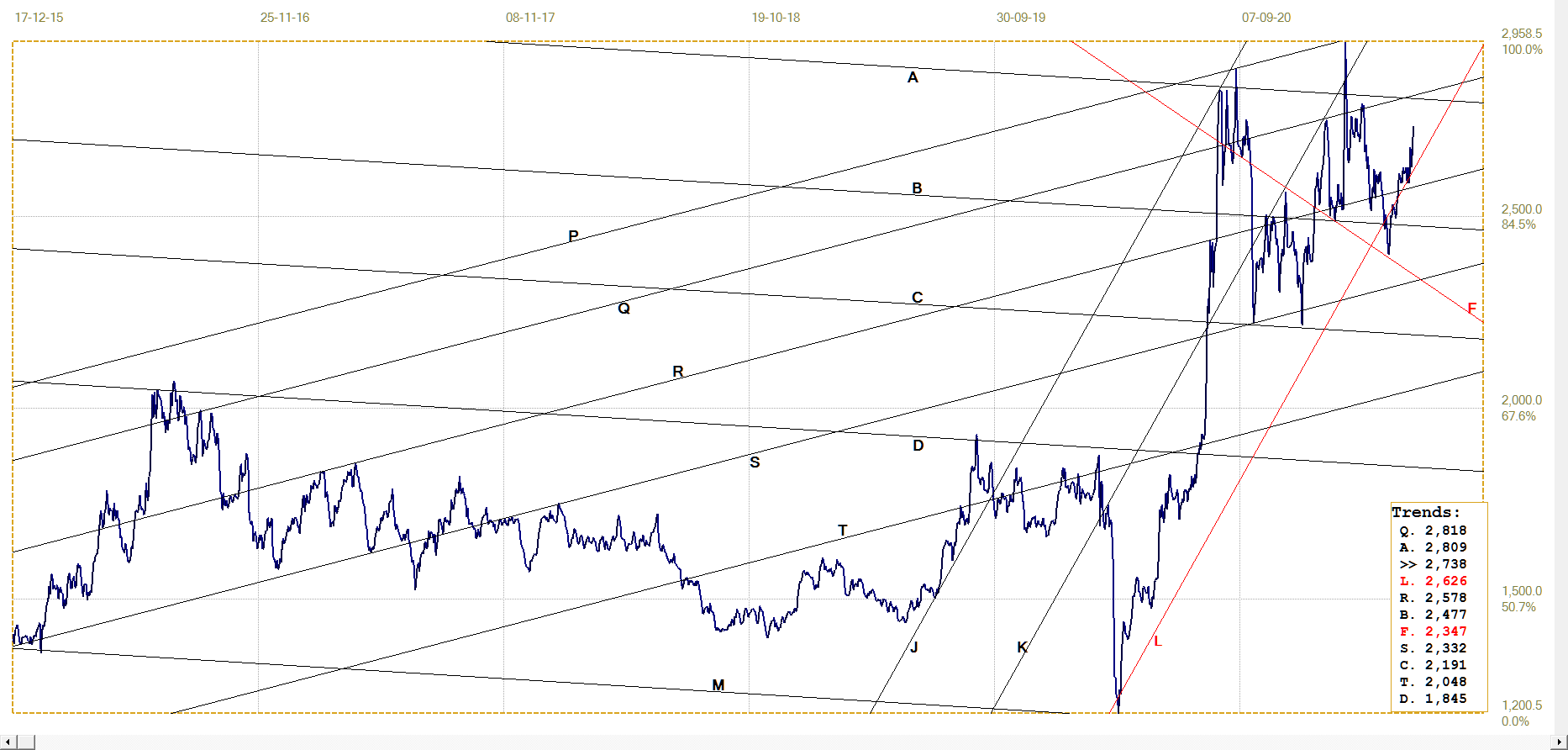

Euro–gold PM fix

With the euro holding firm against the dollar and gold under a cap, gold priced in euro is doing little – neither gaining nor breaking back to again test support of bull channel JKL. At least not yet, so far, following recovery into channel KL after a brief break.

Similar to the dollar price of gold, there has been a break above descending resistance to signal a bullish bias for the euro price of gold. Technically, therefore it looks as if the ruling trend should continue higher, which anticipates the dollar price to resume its rising trend.

Euro gold price – PM fix in Euro. Last = €1513.68 (www.kitco.com)

Silver Daily London Fix

The silver OI on Comex ended the month of April at 161 569 contracts, decreasing by 4853 contracts on that last day of the month. On Friday the preliminary silver OI was 175 701 for a two week gain of more than 14 000 contracts and with a gain of 412 contracts on Friday. The further suppression of the silver price following the April month end equals about 878.5 million ounces of silver.

At $27.50/oz, the value of the OI stands at more than $24 billion. The increase since the end of April is about $1.9 billion. Adding the value of the 50 000 new gold futures since April, or about $9.25 billion, brings the added potential cost of price suppression since April at a gold price of $1850 to more than $10 billion. The Cartel must be pretty sure they can control the price better than they could do during May last year.

Silver daily London fix, last = $27.23 (www.kitco.com)

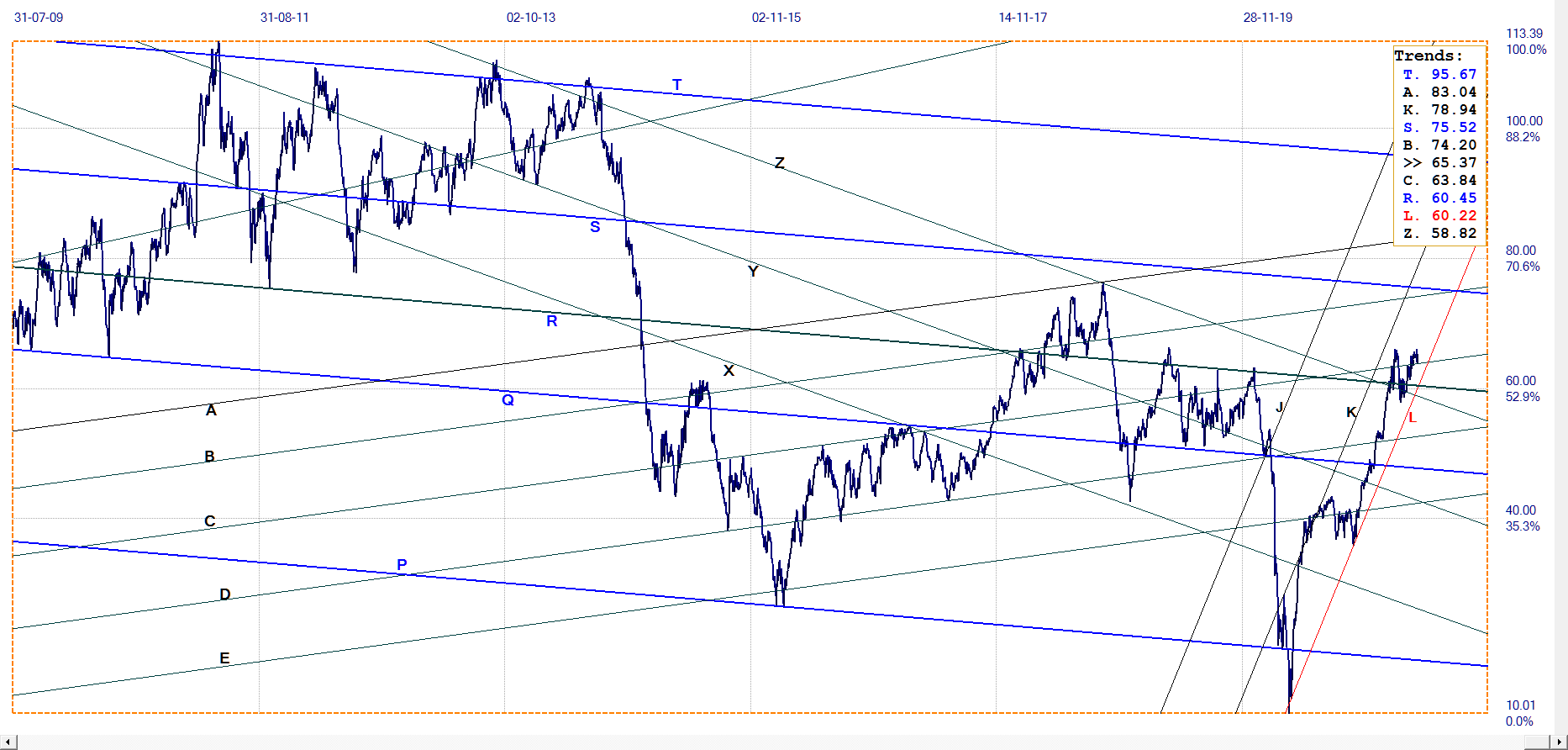

U.S. 10–year Treasury Note

U.S. 10–year Treasury note, last = 1.636% (www.investing.com )

Again there is nothing much to say about the yield on the YS 10-year Treasury note. Except, perhaps, to comment that the yield has become remarkably range bound and quiet despite all the warnings of higher inflation already in place and much more to come. Despite the break above the longer term bull channel XYZ to free the yield to move higher, it has stuck sideways as if loath to extend the trend.

It is almost as if there are forces at work to silence the inflation watchdog – or at least to mute its barking – before it wakes everyone up to what is happening.

West Texas Intermediate crude. Daily close

WTI crude – Daily close, last = $65.37 (www.investing.com )

Much the same last comment on the 10-year yield also applies to the price of crude. It, too, has broken above a significant channel enabling it to trend higher, but it is also stuck in a sideways trend. Should there also be some interference in the normal market price discovery here, the motive would be less silencing a watchdog than the attempt to prevent the cost of energy spiraling higher – with widespread effects on the cost of a whole range of products and services.

With inflation already on a tear, adding gas to the flames would not be a good thing.

*********