The New Normal

About a year ago, when what soon became known as the COVID-19 pandemic had started to spread from its epi-centre in Wuhan in China to the rest of the world, I wrote that 2020 would go down in history, along with 1939, 1973 and 2001, as a year in which the world changed in fundamental ways. So far, this opinion seems to hold true. It is not only the new virus that has triggered a discontinuity in the time stream; late in 2020 the election provided a surprise result that, on what evidence is available so far, is going to extend the discontinuity in new directions. Welcome to the new, new normal.

2021 has also brought something new to the pandemic. The first was the news that the vaccines to protect against COVID-19 – quite a number from different countries – are being distributed. The second was that new variants or mutations of the virus have appeared in the UK and in South Africa, and perhaps in other places as well. Mutations are the reason why different versions of the common flu require different vaccines and now, with news that the AZ vaccine being distributed in South African has failed to protect people against infection, the new virus is behaving much like the seasonal flu.

That implies that soon and in time more generally, there will also be new seasons of a COVID-xx virus circulating in the world to re-infect people who have already been sick. While post-vaccination infections so far appear to cause only light or moderate illness, this might not remain so. This is a troublesome development, in particular since the SA mutation, which has spread to other countries, which includes the US, is more virulent in younger people, who suffered less from the original virus than the elderly or otherwise compromised people.

Another surprise now in 2021 is from the active Left – Antifa and BLM. Antifa was long thought to be the Storm Troopers of the Democratic party, while the BLM was a radical movement with an ‘equality in diversity’ motive. After they jointly marched through Washington DC with a mantra of “Burn it down,” they are emerging as a force acting on behalf of the Far Left. This introduces a third division in US politics, one that swings the balance towards disruption of the existing social order, not the ‘growth of unity’ as the official message for public consumption.

Other than the pandemic and the political order, the economy is also going through much change. The $1.9 trillion relief handout as promised by Biden had a speedy passage through both Houses, with the VP vote to break deadlock in the Senate, as could have been anticipated. This adds about 6% to the Federal deficit, to continue a trend set in 2020 that soon could introduce the practice of Universal Basic Income (UBI) as a fait accompoli, without having to pass any laws through Congress.

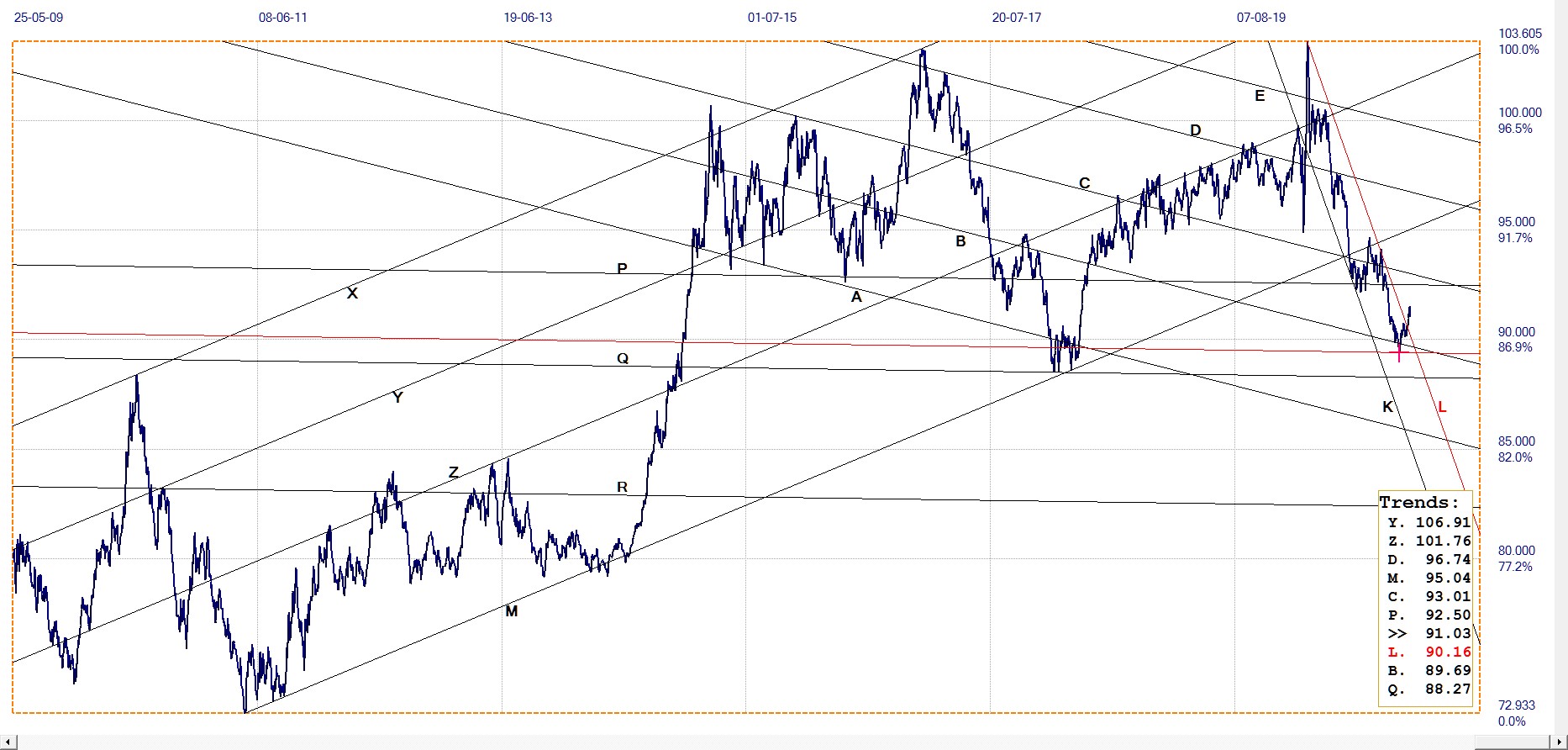

The usual economic law of supply and demand suggests that with increased printing of dollars during the past year – which is speeding up as time passes – the value of the dollar should decline against a basket of currencies. The decline of the dollar as measured by the dollar index that had started at 103 in March 2020, did resume in November last year when the possibility of a $600 – then $1200 – relief payment was mooted. The dollar held for some time at line P at 92.50, but fell steeply once the principle of a new relief fund was accepted.

Now that the ante was upped to $1.9 trillion – about $1400 per person – the new normal came into play and the dollar improved from its low of 89.409 after a break below line B to Friday’s close at 91.03, which has taken it right out of the narrow and steep bear channel KL. This surely is an example of the new normal spreading its wings into the economic domain and the exchange rate arena.

Called a ‘stimulus package’, which adds a positive slant to it, this amount of money is close to 10% of the pre-COVID GDP – a really big stimulus. At least it sounds a lot better than calling it “COVID household rescue” or, heavens forbid, a “survival fund,” thereby to cast some doubts on the change in the White House.

Yes, the economy is affected by COVID and despite the vaccines being distributed, it will take time to achieve the kind of herd immunity that the experts predict once enough people have been inoculated. It will take time to get the economy back up to speed and that success might be put at risk if new mutations of the virus are not susceptible to the vaccines and the pandemic continues, one wave after another.

I am by nature an optimist, else I would not have kept most of my savings in the precious metals for the past two decades. However, we have reached a stage in the economies of the west where we are hovering close to the brink of economic and financial downfall, largely of our own making.

Governments set an example for business and households of instant gratification as the ideal to strive after and that taking on debt is the way to achieve this. Political expediency was the driver of government and quarterly bottom lines and keeping up with the Joneses – and with the latest technology – drove the corporates as well as the middle class. Then COVID came along and far too few of them had reserves or savings to survive the hardship it – and the new regulations – had caused.

All of us, in most countries of the west, now find ourselves in a hole that we have dug ourselves in pursuit of the ‘good life’ to which we were destined, as if it would never end. Then in 2020 it did and now we have to dig ourselves out of the hole to begin anew; hopefully having learnt a few lessons along the way that will stick a lot better than the similar lessons we all should have learnt in 2008/9. A tough life for lower and middle class or worker and employee households will be the new normal for some time to come, with taking on more debt on the agenda for perhaps most such households in order to sustain their standard of living or – in many cases – to simply survive. 2021 may not turn out to be an improvement on 2020.

Gold and silver were both creeping higher on Friday and are continuing the trend in the pre-open period on Monday. On the preliminary COMEX report the gold OI was down by 7350 contracts on Friday – the short position apparently improving a little – while the silver OI gained 1300 contracts. While gold fell proportionately less than silver – probably because of the REDDIT squeeze that had accelerated the price of silver more than that of gold – the silver price is recovering faster. This could also be the effect of traders and investors having more understanding of the total silver short position.

While the REDDIT squeeze attempt fizzled out as soon as the market was attacked with massive selling, so that many of the buyers were squeezed out in return, most day traders might have decided that a silver squeeze is not within their power, as big as it is; they are mostly relative lightweight traders that employ silver proxies and options rather than taking on silver futures and standing for delivery, which is the key to success.

However, the fact that the day traders and small investors had emptied the vaults of US retailers of silver within a day or two, must have brought home the fact that silver supply is indeed limited. That would motivate investors with deep pockets to consider hitting the Cabal where it hurts – taking delivery on COMEX. Perhaps, if this is so, we might see early signs of a change at the end of the month when the March active month begins.

Euro–Dollar

Euro–dollar, last = $1.2042 (www.investing.com)

The firmer dollar had its effect on the euro, which remained softer late last week, to close at the bottom boundary of steep bear channel UV. Early on Monday the dollar strengthened further. If the firmer dollar trend lasts through the day to end with a break below the steep channel, the technical outlook for the European currency will remain negative. That event could precipitate a move lower to $1.183 at line R.

DJIA daily close

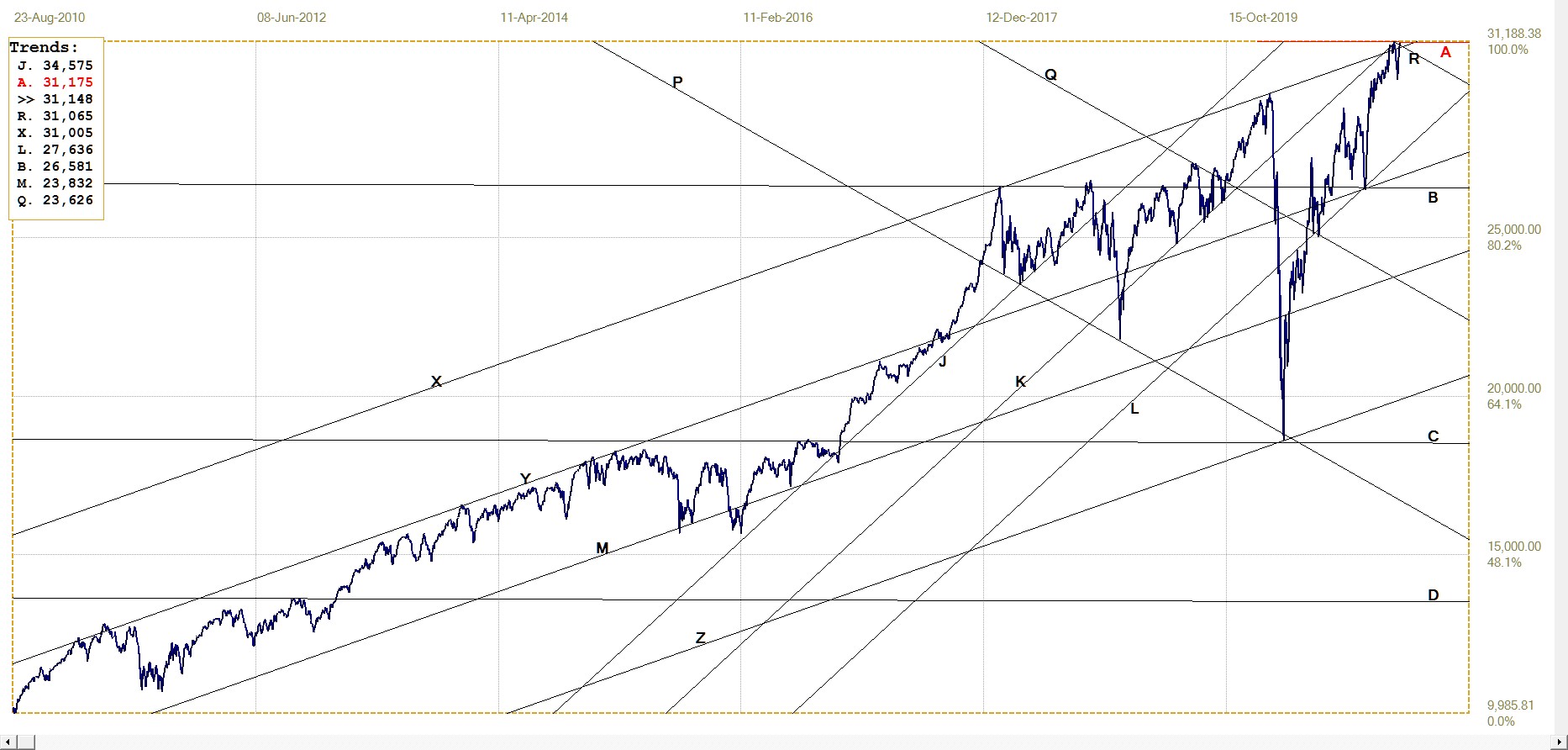

Different from the week before when it was weak, the DJIA ended last week on a high note after a rally that lasted the whole week. The close was only about 40 points below the all time high and discounts the fact that the economy is struggling to get going again. Could it be that expectations for good corporate results at the end of Q1 have investors now bullish again? Perhaps because workers are queuing for jobs they can be hired at lower wages, while many consumer goods are scarce and prices are rising? Or is a prospect of $1.9T ready to flow into the cash registers boosting the stock market? Perhaps all three of these considerations?

DJIA. last = 31148.24 (money.cnn.com)

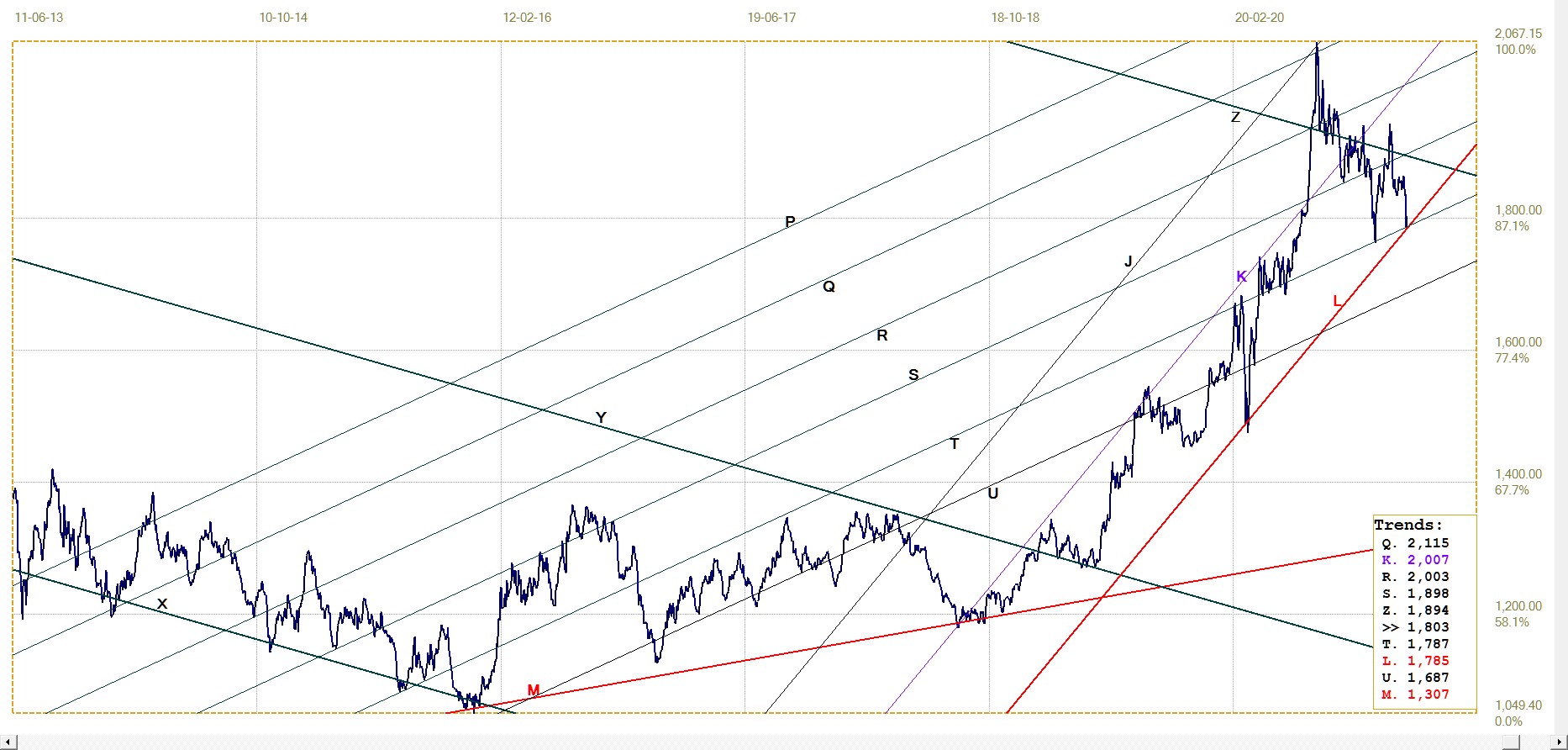

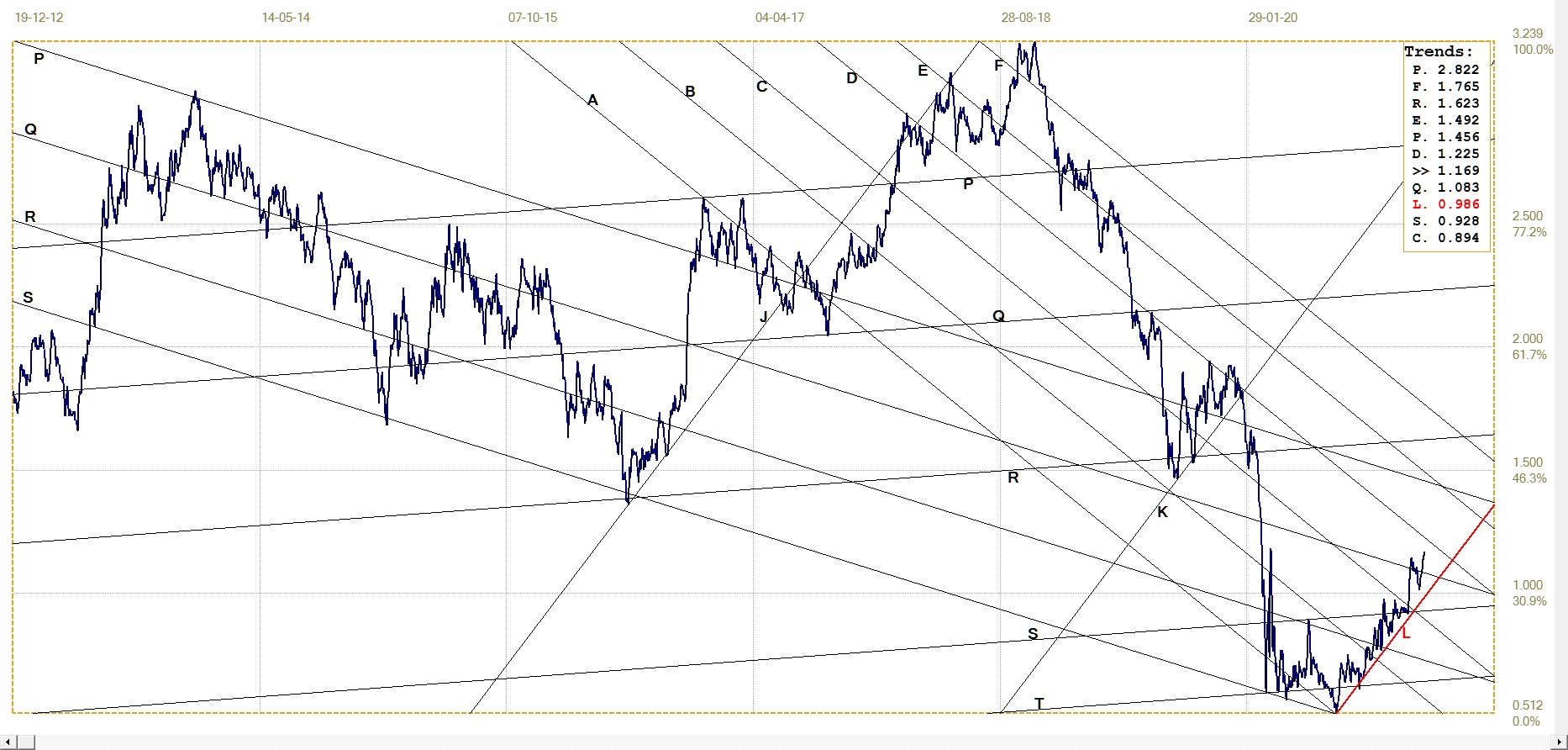

Gold London PM fix – Dollars

Gold price – London PM fix, last = $1802.80 (www.kitco.com)

The new post REDDIT attack on the price of gold on Friday ended at line T and the bottom of the symmetrical channel JKL. With the price currently in early trading on Monday at $1830, after the Friday PM fix at $1802.80, the future for gold shows a yellow glint of a new sunrise.

We do know by now that Mondays typically do not start well for gold, but so far the early selling in Asia has not had any lasting effects. Perhaps here too a good many investors have realised that the Cabal could be vulnerable – if only for silver. Yet, if silver is to begin a sustained rally, the gold will follow. Investors predisposed to gold may also begin to accumulate in the hope that the two precious metals soon are to resume their interrupted joint bull market.

Euro–gold PM fix

Euro gold price – PM fix in Euro. Last = €1499.87(www.kitco.com)

The second break below megaphone PF is again holding at line C. The prospect that the price will reverse high off that support is looking quite good at the moment – with early strength in the dollar as well as in the price of gold, these two factors work together to boost the euro price of gold – a combination of trends not often seen at the same time.

It still would require sustained trends for the euro price of gold to break back into the megaphone and also above the resistance of line G. Not impossible, but not too likely in the near term.

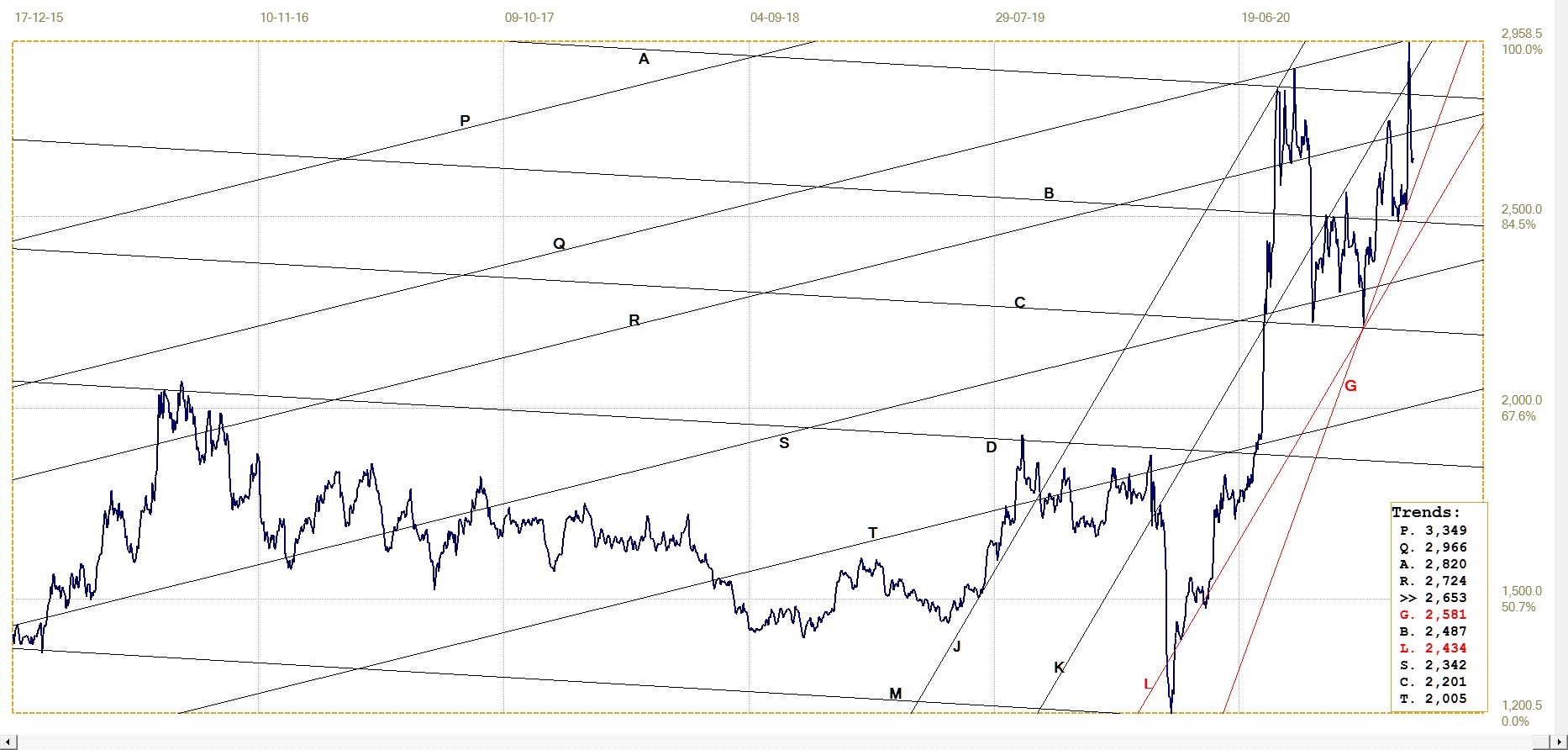

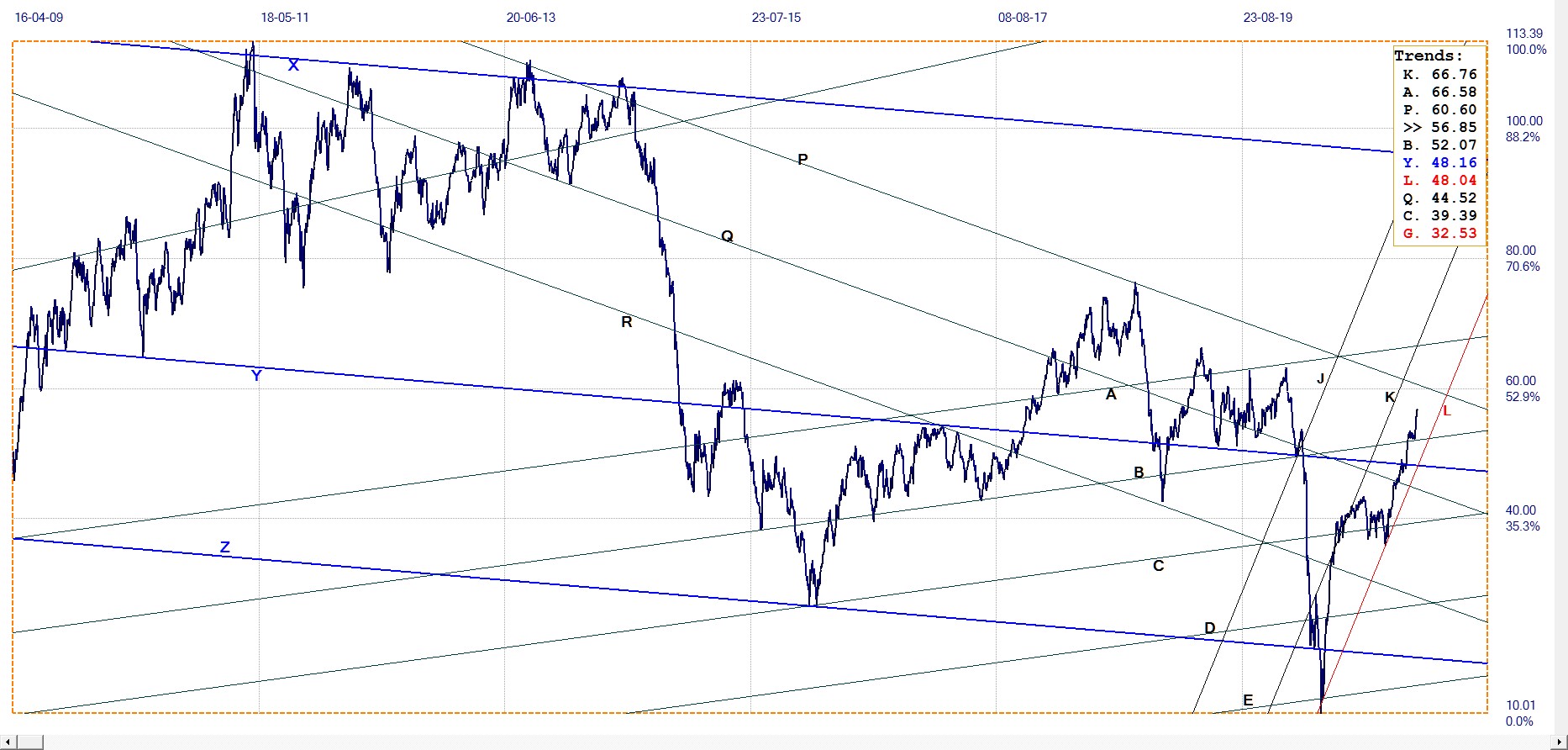

Silver Daily London Fix

Silver daily London fix, last = $26.53 (www.kitco.com)

The REDDIT event had the price of silver spiking higher to reach line Q a second time, to establish a new intermediate high for the rally. The steep reversal lower when the price was attacked last week reached almost as low as where the REDDIT rally had started, but at least held above steep support line G.

On Friday the London fix was at $26.53. The Monday London fix will not be known until tomorrow, but with silver currently above $27,30 – still before US markets open and before the usual early morning attack - it does look as if the rally now is resuming; with a long way to go to set a new intermediate high! But most markets have become volatile, and so anything could happen.

U.S. 10–year Treasury Note

After the break lower below line Q three weeks ago, the yield failed to hold the break and soon reversed to break higher again. Now that it is back above channel QR again and still holding clear of the steep support of line L, to hold in bear channel KL, the price is holding in a tight range; as it has done while trying to break above the sideways channel ST.

The bearish trend could be the result of the excess supply of treasuries during 2020 and now the additional $1.9T of which much will be reflected in 10-year Treasuries. Alternatively, with the focus no longer as strictly on bringing back manufacturing to the US, the continued reliance on imports could mean higher prices in due course and the risk of inflation – whether or not the Fed then responds with higher rates.

U.S. 10–year Treasury note, last = 1.169% (www.investing.com )

West Texas Intermediate crude. Daily close

WTI crude – Daily close, last = $56.85 (www.investing.com )

Before the price of crude broke higher above channel ZY, it held just below line Y while trying to affect the break. When the break happened, a steep move higher soon had the price breaking into channel BA, while holding well within the steeper bull channel KL. The price then clung to line B for three weeks before it resumed the rally last week, to close on Friday at a new intermediate high.

Crude remains in a bullish mode while holding – and extending – above line B and also holding in the steep channel KL. As mentioned last week, the move higher may be in response to expectations of future scarcity now that the Keystone project has been iced while exploitation of oil in nature reserves and wilderness areas has now been curtailed by an executive order. Even with the economy struggling along, supply of oil could become a problem – more so if the economy does improve.

********