Serial Resets

A recent more often read word in commentaries on matter of an economic nature is “reset”. As a term it is unlike, ‘overweight, ‘fast’ and ‘tall’, where people know quite well what it means; it is more like “beautiful’ and ‘rich’, where the one who hears or reads the word interprets it within their own context. Someone might say, “I am so looking forward to the coming reset,” which causes his listener to wonder where he could find an isolated place at which he could escape the consequences of such a world-churning event.

In the absence of clear-cut hard news on the outcome of the presidential election, it seems better to leave that event – or extended process? – until later. An objective observer might say there are two possibilities: either there was massive voter fraud on the part of the Democrats or there is massive perjury on the part of Republicans in their effort to conjure up evidence that does not exist. To speculate at a possible outcome and any repercussions on those at fault in this affair is premature.

COVID is still on an uptick, globally and locally in the US. In this instance, just as is the case with the election, there are two very partisan groups at loggerheads. On one side is the fear that, if not contained, COVID will wreak terrible effects when it progresses unchecked to infect many more people than the seasonal flu. The other side believes it is no more than a stronger seasonal flu and it is only the elderly and compromised who need to take special care not to get infected.

Both sides appear to either dispute the COVID statistics or to interpret these in a manner that supports their point of view. The difference in opinion extends to the accusation of official and other meddling in the reported number of cases and the actual number of COVID deaths. Another case of ‘never the twain shall meet’, but, as so often happens, time will tell - eventually.

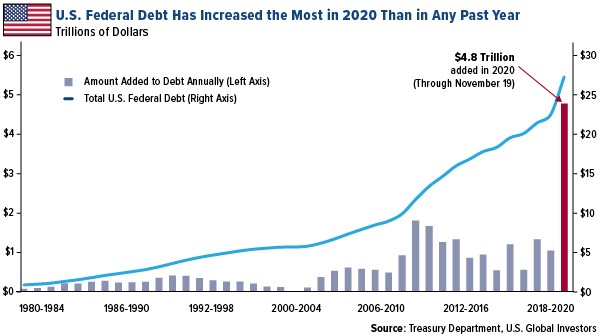

The one reset that I think most reasonable people will agree on the necessity for it has to do with debt. A recent Frank Holmes article had global debt at $277 trillion by the end of 2020 – a significant portion of it arising from the cost of dealing with COVID and the effects of regulations to contain its spread. That amount calculates to $35 500 for each of the about 7.8 billion people alive today and the $27 trillion US Federal debt is nearly $80 000 for each of the about 330 million Americans.

World government debt is reported as $53 trillion by year end, of which the US has a little more than half. Which is not surprising given the way US budget constraints have been disregarded, initially under Reagan and then followed by Clinton (despite his claim of a balanced budget after robbing Social Security) , Bush jr. and Obama – all in pursuit of stimulated economic growth.

That is history; the question is what to do going forward? Many view the remedy as a debt reset, which effectively means debt forgiveness. All people who suffer under their own load of debt are in favour of this one. Life would become much better if all household debt could disappear, including study debt that the government can write off with the flourish of a pen.

Other household debt is mainly owed to the banks and financial system. That will not be as easy to reduce to nothing. Much of it is money deposited by other people – apart from the money created out of thin air by the fractional banking system. If the money had been created with a few key strokes, surely the money can be made to disappear as easily, with no real effect on the world? However, the banks won’t like that at all and doing so would make waves with major and far reaching effects, some of which are bound to be more uncomfortable to many households than the original load of debt.

Can Federal debt be made to disappear with a suitable signature on a document? It is debt due to be paid by taxpayers at a time in the future that is indeterminate and almost nebulous and uncertain. I think government would welcome such an event, a reset of Federal debt back to zero. Not so much with a sense of relief at having successfully dissolved the negative entry on the balance sheet as with excitement at the prospect of larger budget deficits as they face the future with a clean slate.

A debt reset is a ticklish problem, but two other resets being bandied about are of a more complex and extensive kind. The one is the reset of a global reserve currency. This role is currently being played by the US dollar and has effectively been so since the 1940s. The dollar is still the single dominant currency and the only one, as yet, that is available in sufficient volume to support global trade. Will that still be so in 5 or 10 years’ time? If China’s economic growth were to continue, even after effects from COVID, can the world cope successfully with two – probably competing? – reserve currencies?

To an ignoramus in these matters like I am, more likely to happen is a new artificial reserve currency that consists of a basket of the major currencies. To ensure fiscal discipline on the member countries in the basket, their commitment to the basket could be weighted in terms of the price of gold in their native currency. The more profligate that their printing of money becomes, the more they have to submit to the pool on which the basket is based.

Hopefully something of that kind could be established in time to prevent some kind of deadlock in the global financial system and also without guns and bombs getting involved in the dispute. This one won’t be as easy and simple as the disappearance of much of the debt, and national sensitivities will probably come into play on all sides before the problem is resolved.

Then there is a third reset of much greater importance to most people alive today on a global scale. It has been spoken about in various lofty forums and speculated about in think tanks and is the subject of a range of conspiracy theories. I often quote Stein’s Law and it also applies here. Google ‘global population growth’ under ‘images’ and the result will show a series of charts extrapolating population growth the end of this century. Interestingly enough, most show a reversal lower late in the century, at populations that range from about 9-10 billion people to 14 billion.

Rumours are rife in various circles that there are plans afoot not to wait for near natural forces to restrict population growth 50 and more years from today, but to take the necessary steps to ensure that ‘peak population’ happens much sooner. It is held by some wearers of aluminum hats that COVID-19 happened to be either an unsuccessful attempt at achieving peak population right now or is a dry run for a later, more virulent virus that will do the job – obviously with a prepared immunity for the conspirators.

Such a population reset, presumed to be complete with imbedded ID chips, would have different effects on the world from a natural one. A planned one would cull the elderly and other people less fit to serve the new ‘Masters of the Universe’ who will hold control. They will want to keep people alive with skills to keep the wheels that support their life style turning. If population declines because of a reduced birth rate the situation will get worse over time as the population ages more and more.

These conjectures of course presuppose that Mother Nature will not take care of the problem of over-population – as another school of believers look forward to in the hope that the faithful will be exempt from the culling when Nature triggers the solution to too many people. Whether it will be a new ice age as the sun dims into sleep for 25-40 years or whether one of the major volcanoes will blow its top in a manner that induces a ‘nuclear winter’ lasting a number of years is irrelevant. It could even be global warming that causes weather not conducive to production of food that unleashes a global famine to cut us back to size.

If one mentions ‘reset’ in your presence, it is best to first determine what kind of reset is under discussion before either agreeing or disagreeing with him or her.

In a more down to earth sense, all of the above review has little bearing on what is happening on Wall Street. COVID also is of no consequence; neither is what then will happen with the presidential election. Nothing counts except that whenever there is selling on Wall Street, more buyers enter the market and keep moving prices higher. According to Stein, this has to be a trend that cannot continue indefinitely and will stop. The higher it goes, the less likely that it will stop and happily settle sideways.

The long awaited December option and futures expiration finally arrived, only to be wet squib thanks to the severe suppression of the metal prices that had so many of the anticipated profits disappear down the drain – that is, the profit anticipated by buyers of the options and future vanished, to reappear as credits to the sellers. Is the CFTC going to investigate a case of ‘market manipulation to obtain personal and unfair advantage’? Or will the question be asked in court on behalf of class action?

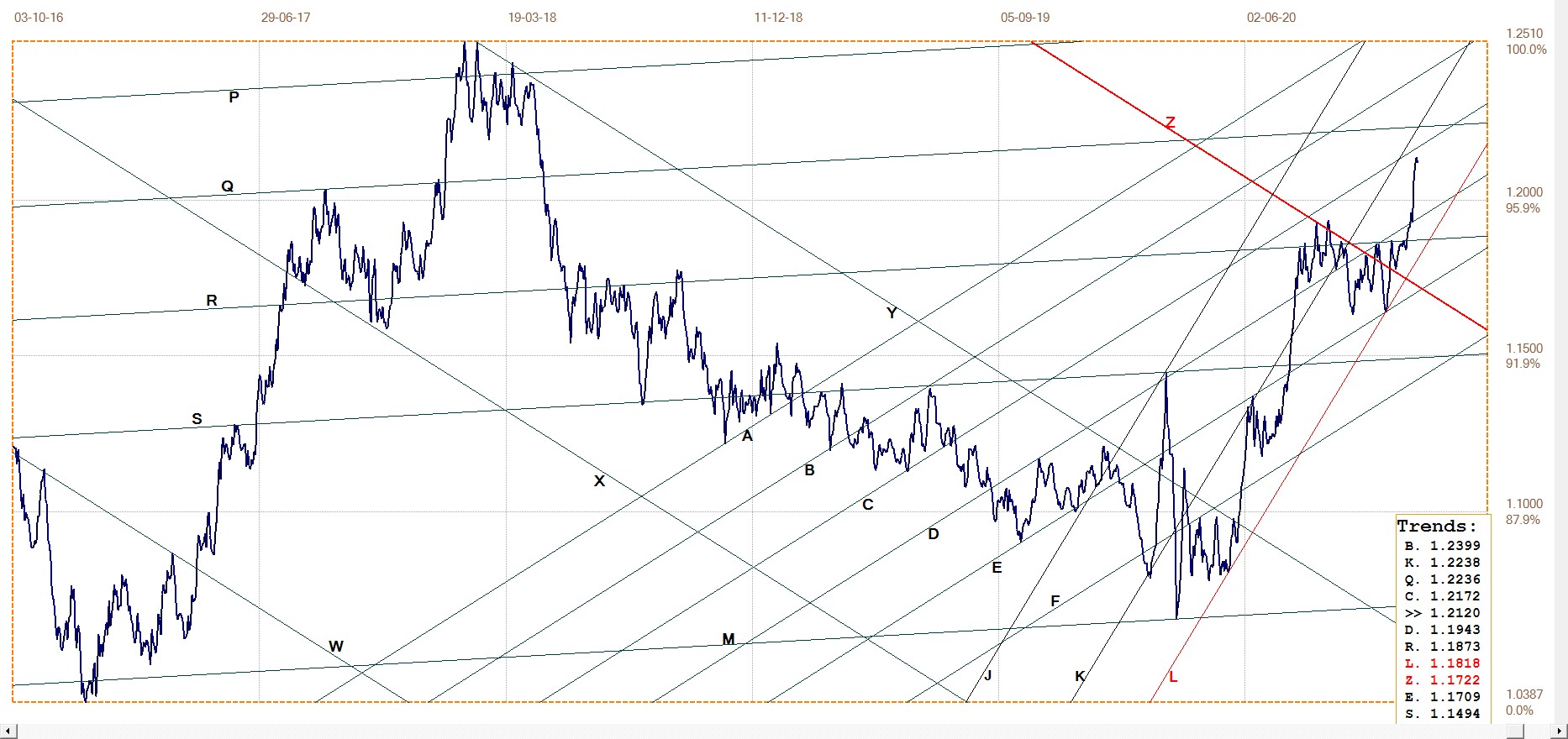

Euro–Dollar

Euro–dollar, last = $1.2120 (www.investing.com)

Elliott wave analysts will be anticipating a fifth, corrective wave for the euro soon. Perhaps it will start off line Q ($1.2236)? For the time being, though, the above analysis shows the euro installed in bull channel JKL ($1.1818) and ending not all that far below line K ($1.2236) for a break into the upper half of that channel. The dollar clearly is under pressure now that the euro finally has broken above the key resistance at line R (1.1873).

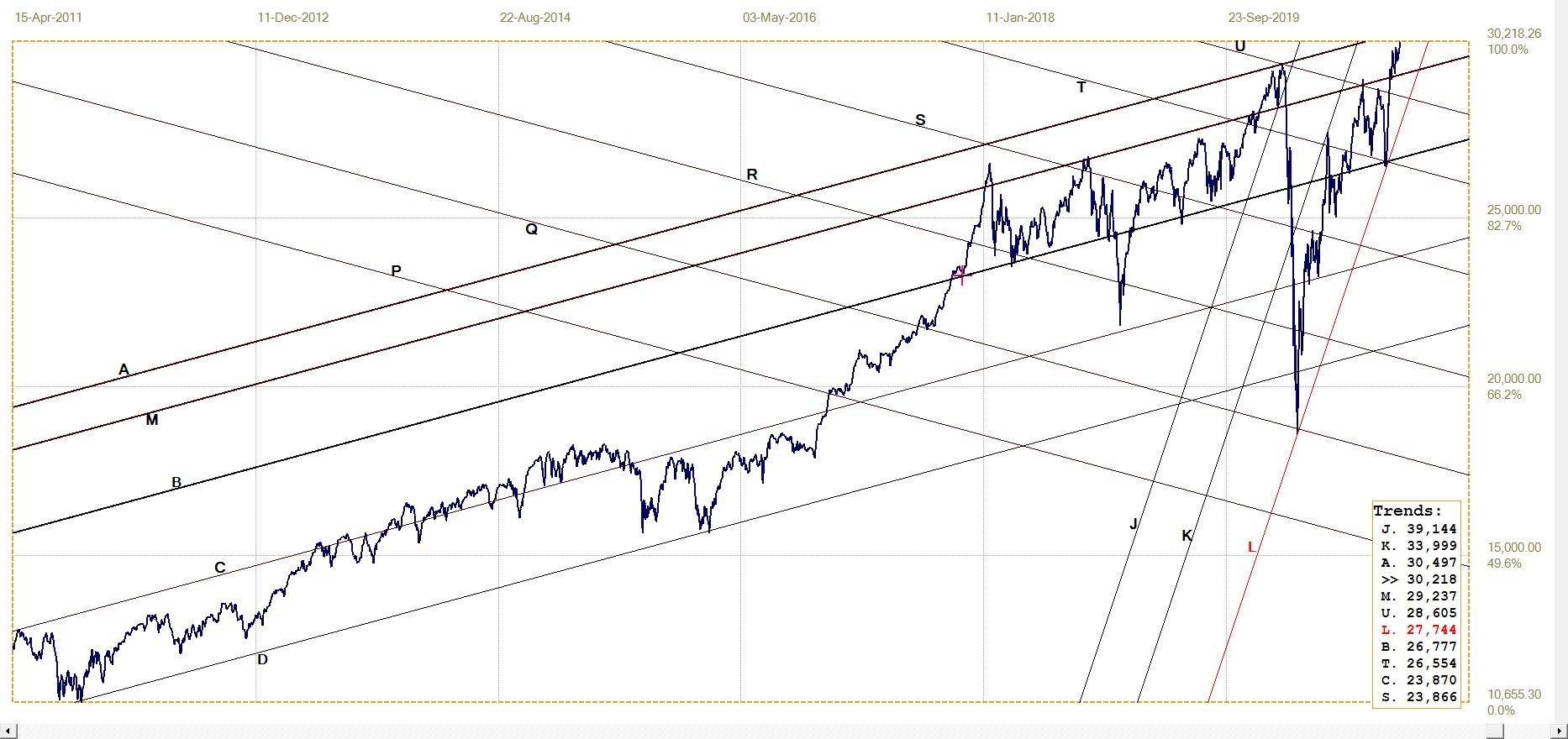

DJIA Daily close

On Friday, the DJIA again closed at a new all-time new high. With the break above the 30 000 level, it is again getting close to the top boundary of the medium term bull channel AD (30 497). All recent indications of the sustained rally despite all the fresh uncertainty about COVID and the continuing efforts to prove voter fraud in the recent elections, are of no interest to the people intent on getting a fresh foot – or another two feet! – into Wall Street.

Can it be credible that corporations will deliver better results than reflected in a 28 PE on the S&P500 given the effects of COVID and with the interest rates perhaps having bottomed and rising? It should be interesting to watch how this turns out – a sustained bull market somehow or the imminent Crash that so many pundits have been warning about for quite some time.

DJIA, last = 30218.26 (money.cnn.com)

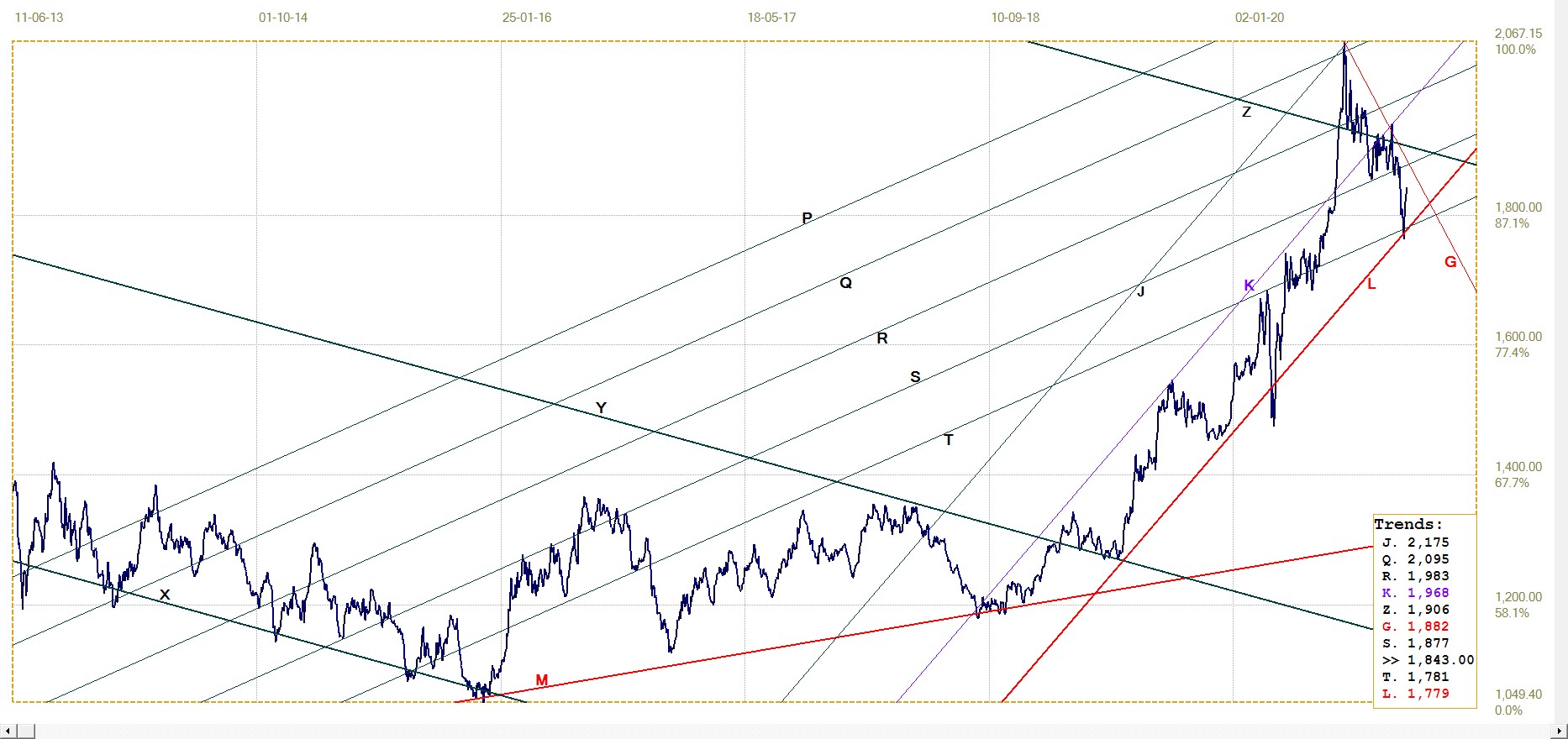

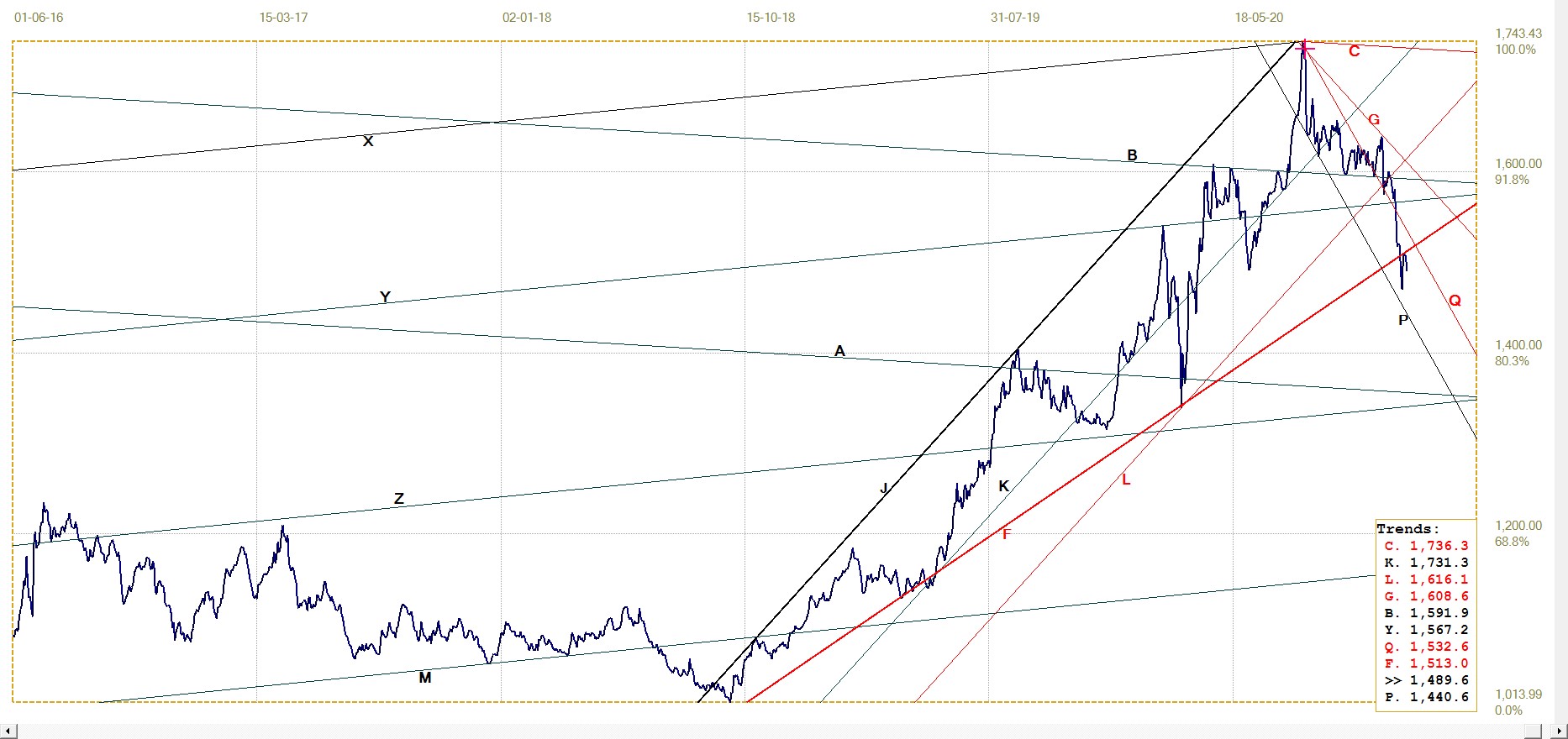

Gold London PM fix – Dollars

Last week, the London PM gold fix just failed to hold to bull channel JKL ($1779), but has rallied since then now that the December COMEX expirations are history. Technically, the new rally is tentative until there is a break above resistance at line G ($1882), with further confirmation to come on a break above line Z ($1906). The price of gold still has a long way to go to set a new high. Could it be that the attack on the metals that started in August had the very large positions in the December COMEX options and futures as the primary threat to neutralise?

Gold price – London PM fix, last = $1843.00 (www.kitco.com)

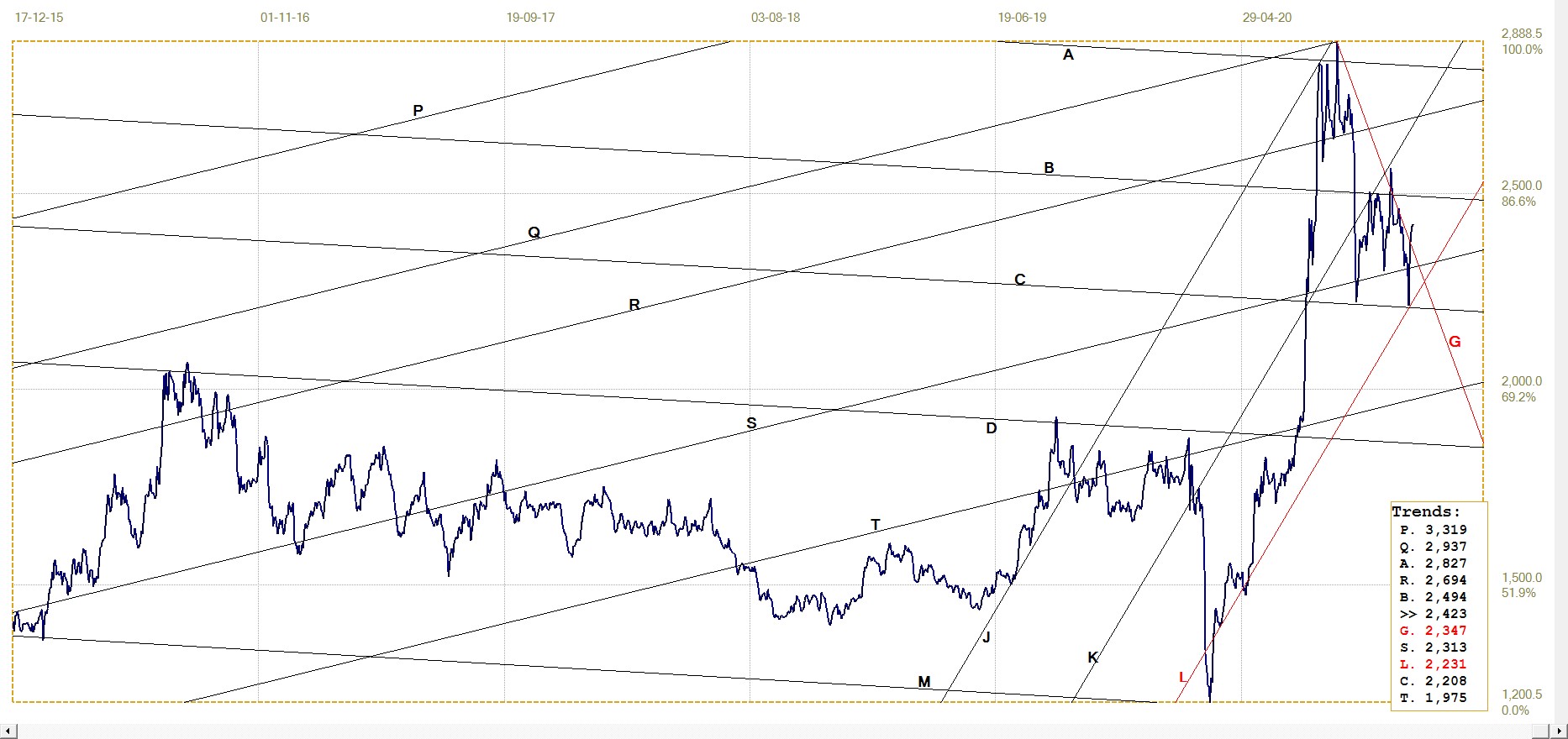

Euro–gold PM fix

Euro gold price – PM fix in Euro. Last = €1489.63 (www.kitco.com)

The bullish performance of the euro against the dollar had the effect to counter the mild rally in the dollar price of gold and prevent a break back into the megaphone JF (€1513). The reversal off line F has to reverse again and then break higher to be more bullish for investors in Europe and re-ignite their interest in gold. With gold no longer as much in favour after the four month attack on the price as it had been at the time of the recent May-August rally, the dollar price will have to speed up some to help the euro price recover into the volatile megaphone.

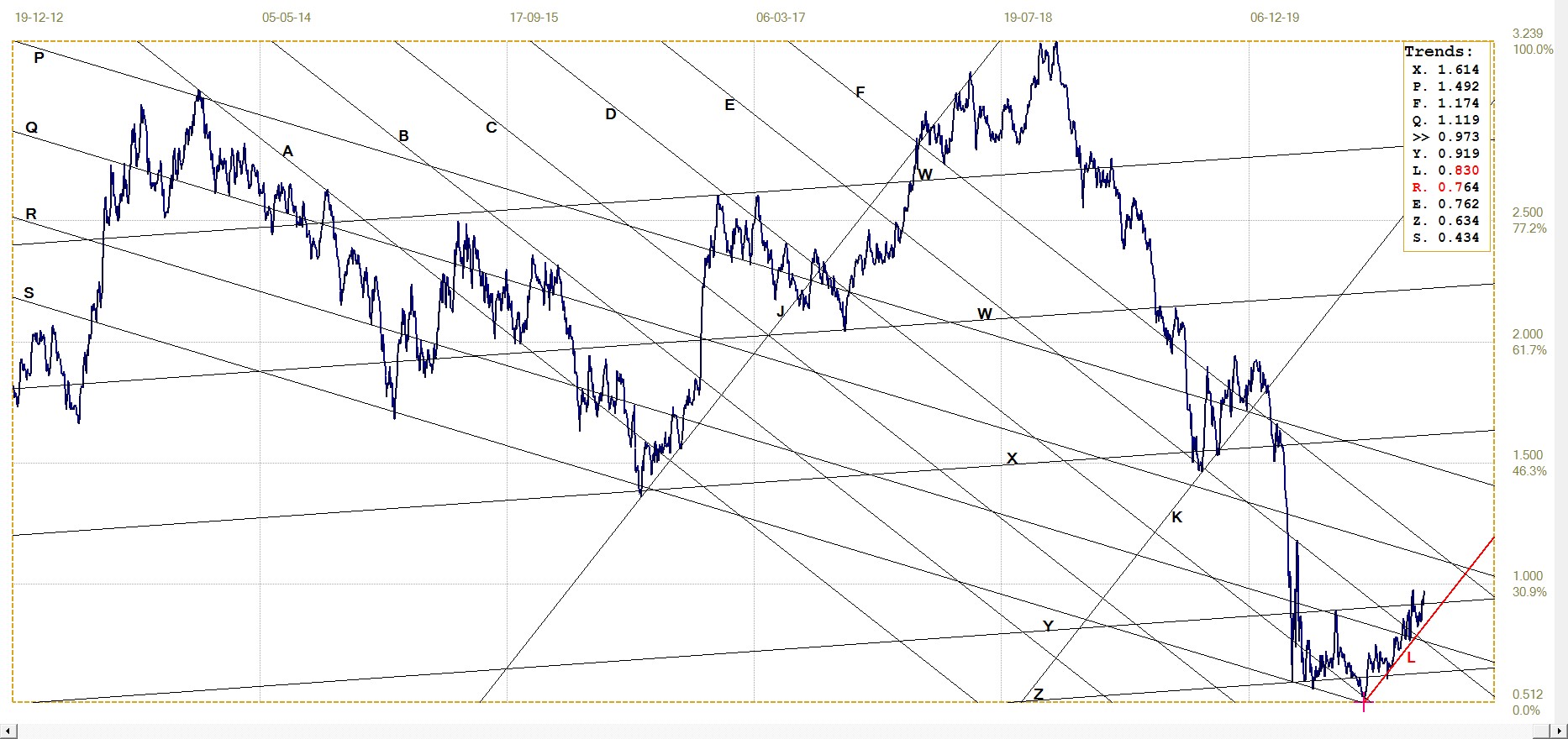

Silver Daily London Fix

Silver daily London fix, last = $24.225 (www.kitco.com)

After rebounding off line C ($22.08) at the end of the recent attack, the silver price has again managed to break above the descending resistance of line G ($23.47) – an early positive sign that the rally could continue higher. Line B ($24.94) is the next level of resistance and is backed up by the $25 round number.

It is difficult to consider a $100/oz or even much higher price for silver after seeing how easy it had been to pull the price back by almost 25% to $22 from its recent high near $30 in order to sink all the option and future positions that were bought subsequent to the break above line C – or that were added to December positions on Comex. The long term bulls who have sat on their December positions from before mid-July must really feel terrible to have seen their profits later blow away like smoke as the price of silver was propelled lower month after month.

Surely what happened, followed by the start of a recovery so soon after November 30, must present some evidence for a class action suit for compensation.

U.S. 10–year Treasury Note

The break above line Y (0.919%) at first failed to hold when the yield pulled back as if to test line L (0.830%). It reversed high a little short of that line and has now again broken above line Y to end a little short from making a double top. At the moment, and with awareness of the effect of a double top, it looks more as if the rising trend is to extend, or at least remain above lines Y and L for the near future.

It seems possible that the bond rally is over, after the yield on the 10-year Treasury note spent all the time since the end of February below 1%. If so, the new question becomes how high it will – or can – go before it will impede economic growth and cause other debt-related troubles..

U.S. 10–year Treasury note, last = 0.973% (www.investing.com )

West Texas Intermediate crude. Daily close

The new analysis has the price of crude holding near resistance at line Q ($45.63). A break higher at this resistance then has to deal with probably stronger resistance at line Y ($48.42). Currently, the price of crude is already about 20% higher than when it broke above line C at $39 a scant three weeks ago. The more expensive crude is beginning to combine with the rising interest rates mentioned above, to act as brakes on economic growth. Perhaps not yet to any great degree, but if the two trends continue, voices of concern are bound to be heard.

********