This Time The Delaware Was Not Crossed

The crossing of the Delaware in midwinter on Christmas Eve of 1776 was General Washington’s major commitment to take the revolution to the enemy. Now, a little more than 245 years later, a similar opportunity for a similar inspirational action presented itself to keep the USA on the path that was chosen by Washington and the Founding Fathers. That step was not taken; the reason can only be guessed at, but it would greatly surprise if the results this time around proceed along the same historical path as the first time, which in time made the USA the most successful and powerful country in the world.

The 2020 presidential election was a fork in the history of the US that I had written about before. The result elected to go down a path that is expected to diverge in a substantial manner and in more than one way from that on which the US has been for the past almost quarter of a millennium. The future suddenly has become less certain, more ill-defined and more likely to produce surprises of different kinds.

In the past, reasons have been found to deviate from the hard-coded precepts of the US Constitution. Now, in the wake of the 2020 election, it is difficult to view the USA other than as a ship in a storm of global proportions after it has lost its rudder and with its 250 year old anchor cable broken. Now an untested ideology has taken over the bridge, which puts the US at the mercy of international winds and currents more than ever before. With a president that could be subject to foreign blackmail.

There was a time when Americans of Jewish persuasion formed a solid core of the Democratic Party and also when Saudi Arabia was a major partner that stood by America and the critical importance of energy and the petro-dollar. Within the first ten days of the new dispensation both Israel and Saudi Arabia have been warned that they no longer occupy such privileged positions in US foreign affairs. A similar message is being received by South Korea.

It is far too early to speculate about what the future might hold, except to state that the available evidence strongly suggests that all that has happened is a result of a near globally orchestrated and now successful coup on the USA. One can only guess at the reason why Trump did not cross his Delaware. His trump cards were his 2018 XO regarding foreign intervention in a US election and the Insurrection Act, which required the backing of the military should there follow an insurrection when Trump invoked a state of emergency after the discovered election fraud.

Where Washington had faced the Crown’s mercenaries from Hesse in Europe, the coup masters mustered their own army in Washington. It would seem the Generals who were backing Trump decided that Biden in the White House was a better option than an all-out civil war and they deserted the president – and the Constitution – when it really counted.

Time will tell, whether it was a wise decision for the generals to renege on their oaths of loyalty to the Constitution. The breaks with the past mentioned in the second paragraph above imply the next few years should become very interesting.

The situation with the COVID-19 pandemic is getting murkier than ever. It was reported that shortly after Biden was affirmed as president, the WHO announced the infection data of the pandemic in the US was “adjusted” to present far greater infection – and death ? – rates than actually occurred. The media pointed fingers at Trump’s managing of the epidemic in the US, despite that the states were in control of their own counter-measures. Will the WHO, now that they have their man on the bridge, begin to ‘adjust’ the statistics the other way, to favour a new management of the pandemic? This while the virus is mutating with the possibility that, as for the normal flu, a new vaccine will be required for new variants of the virus.

There is no doubt that the new policies regarding monetary and economic affairs – and much more – in the US will have significant effect on prices of gold and silver as well as many other aspects of the financial world. It can be expected that – for the near term at least – there would be increased flow of funds from the Treasury and from the Fed to individuals, households and small businesses suffering from COVID because of measures to restrict the epidemic. The money supply is likely to increase at a high rate, which should benefit the prices of the metals and the crypto currencies.

Investors in all major markets need to consider revisions to their strategies in light of probable major changes to the structure of the financial world as it has existed so far. Little of substance has been revealed about these changes to come, except that these can be expected to reflect a major change in the dominant ideology and that the effects will be felt in the US and on the international stage.

Clarification: While I am no fan of Trump the person, I accept and approve of what he was trying to accomplish. I fear that unless some miracle happens, the US will become a new country during the years ahead; a country that I would not like to call “home.” My thanks to Midas for accepting and publishing what I write.

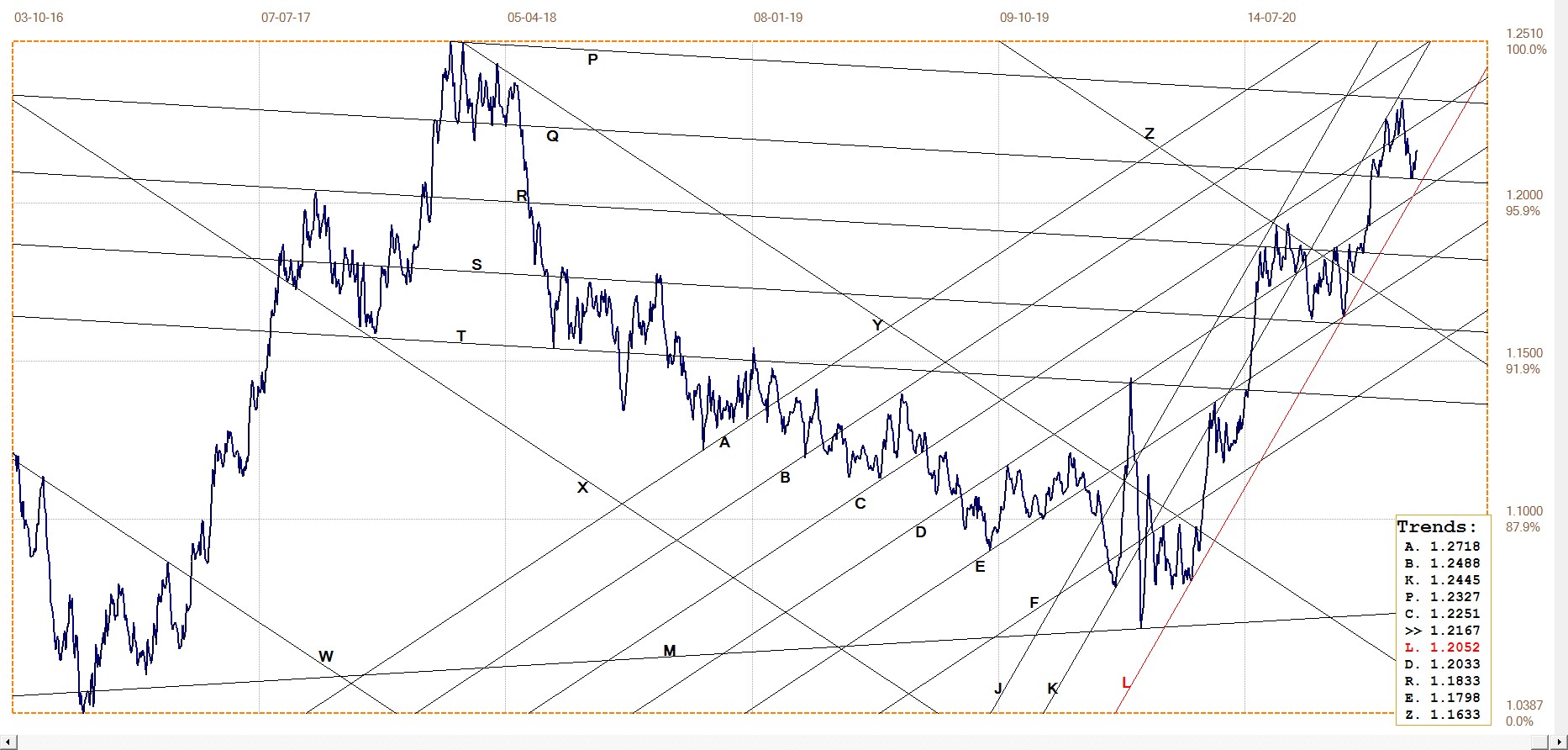

Euro–Dollar

It is always exhilarating to see a steep trend in a price reverse as steeply right at a trend line in an analysis that has been in place for some time. The euro did exactly that when it topped out at line P and scuttled lower to reverse again right at line Q.

This keeps it well within bull channel KL, in line with the general expectation that the dollar is soon to resume its bear trend. Europe has its own problems, but the upheaval in the US and probable changes in economic policies associated with the change do not favour the dollar.

Euro–dollar, last = $1.2167 (www.investing.com)

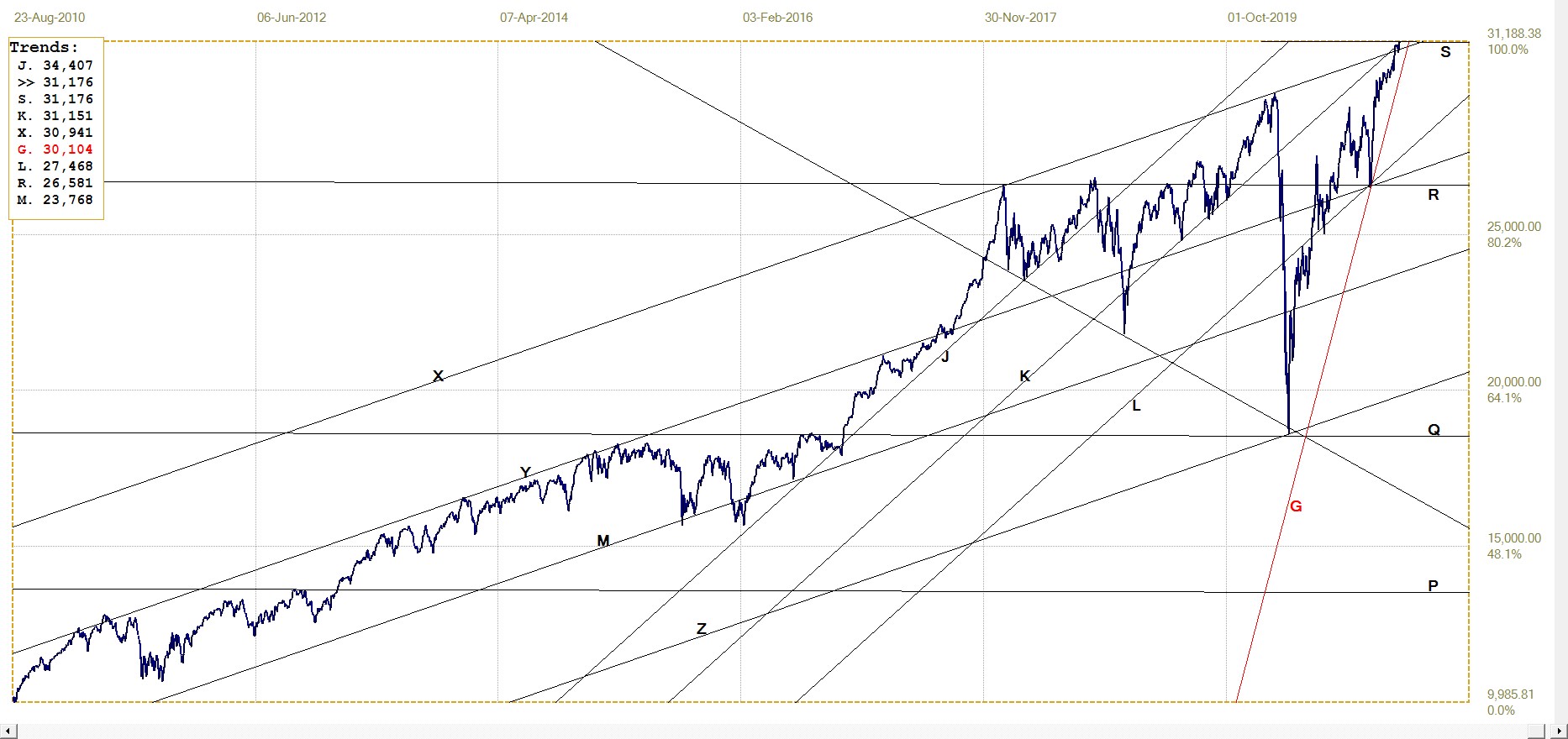

DJIA Daily close

DJIA. last = 31176.01 (money.cnn.com)

The chart this week shows a steeper medium term bull channel than before. The DJIA has broken marginally above this channel, but, while making a new high, it is not (yet?) accelerating after the break higher. After the weak showing on Friday, this week should reveal what 2021 holds for Wall Street.

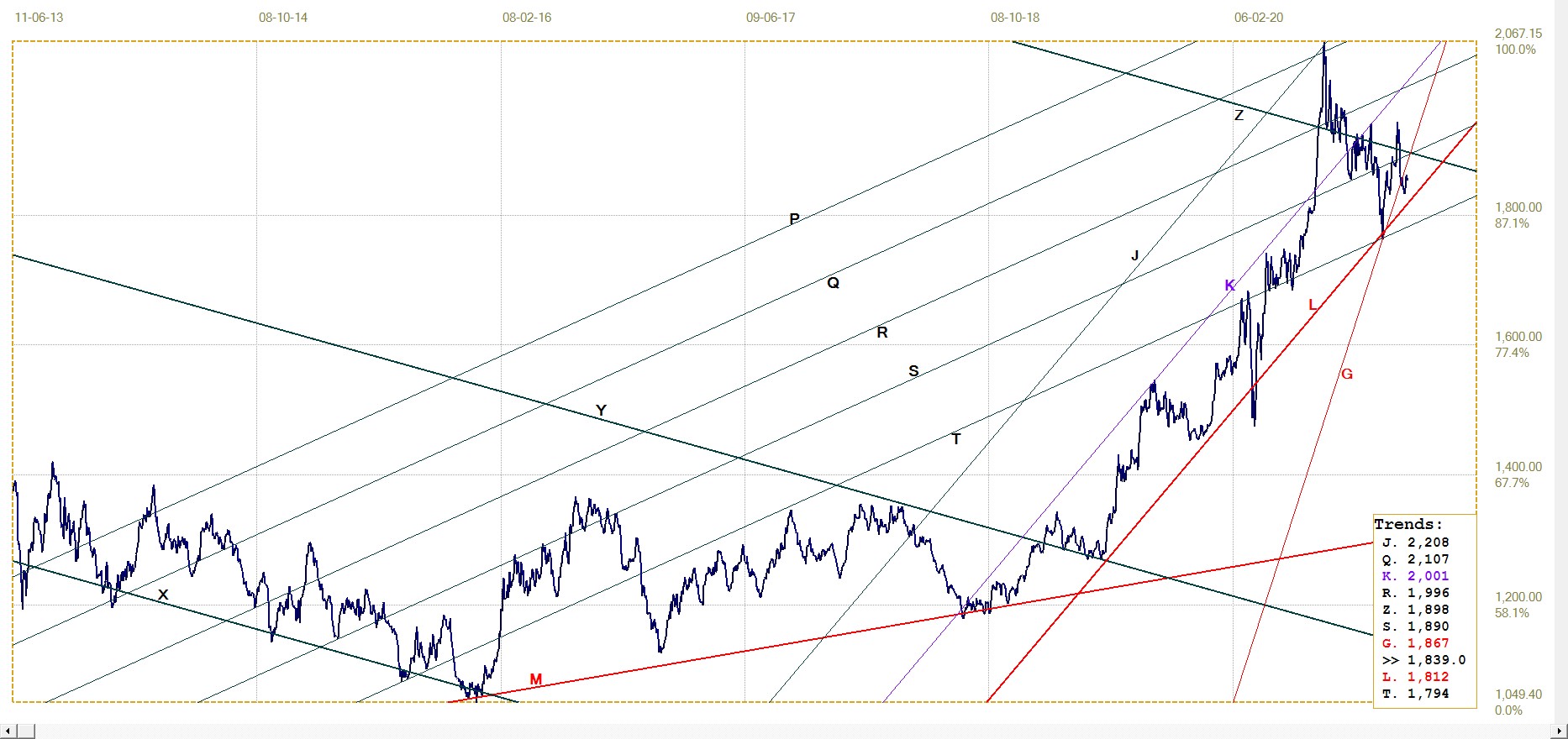

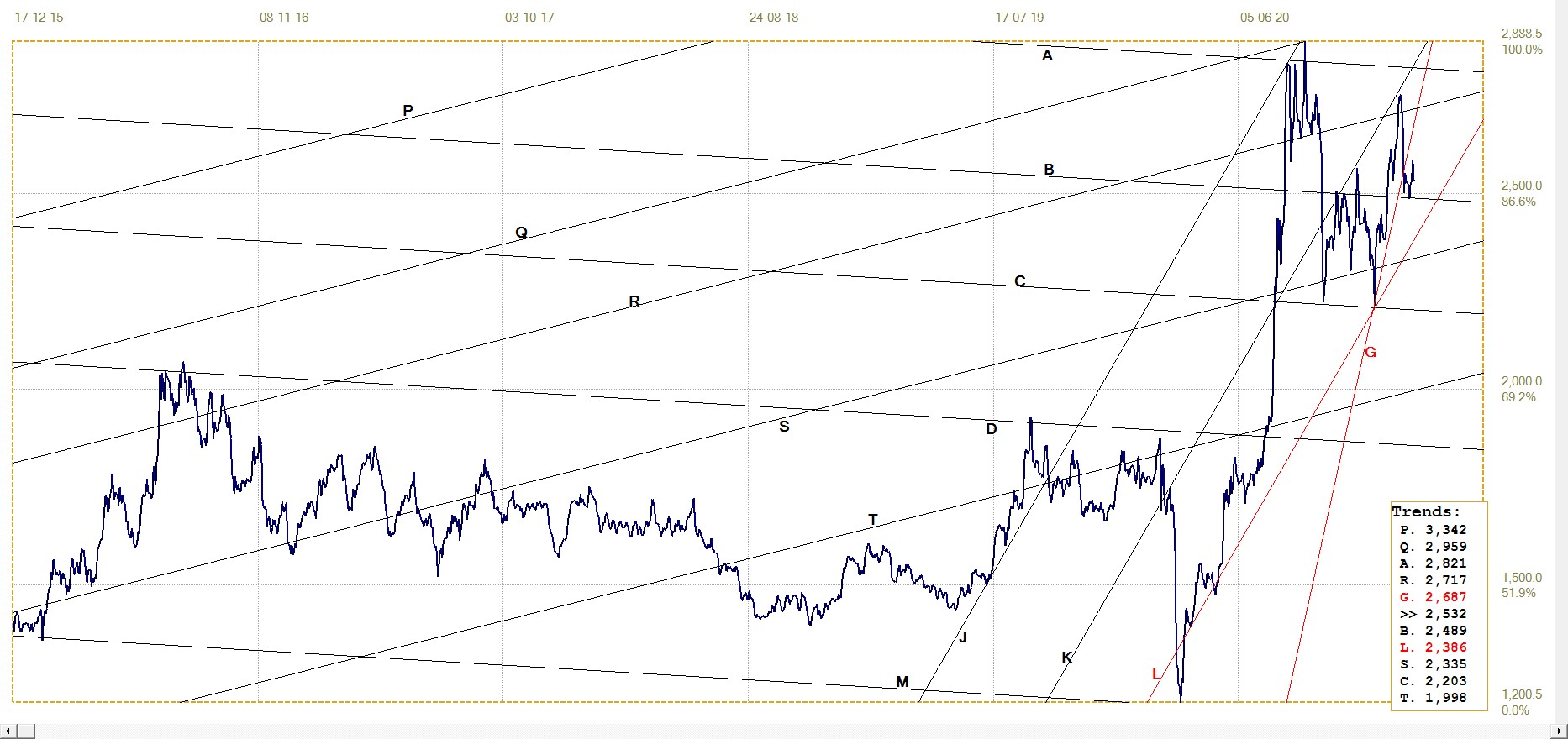

Gold London PM fix – Dollars

Gold price – London PM fix, last = $1852.70 (www.kitco.com)

The steep rally of lines T and L that coincided with the strong performance of the crypto currencies clearly sowed panic among the Big Banks. Their immediate and violent reaction had the price of gold as per the London PM fix breaking back into channel YZ and also below the steep support of line G. So far, though, bull channel KL still holds, which is a positive sign.

It has been assumed the primary reason for control of the PM prices is protection of the US dollar. Given the amount of new Federal debt during 2020 and a probability that this trend will continue in 2021, a desire to protect the dollar will call for more sustained effort. Can this succeed indefinitely? Readers with long memories should think of the time when the British pound was in trouble and much effort went into its protection. That was the time when Soros knew what had to happen and scored a billion pounds from being right.

The question to consider is whether the pockets of the Fed are deep enough to keep the gold price stable against the forces that will muster when the hint of a collapse in the value of the dollar begins to approach certainty and gold recovers its glitter.

Euro–gold PM fix

Euro gold price – PM fix in Euro. Last = €1521.81(www.kitco.com)

The breaks below megaphone PJ have held accurately at the bottom of bull channel PQRS, with the gold price barely managing to neutralise the stronger euro. So far so good, but a break back into the megaphone is now sorely needed.

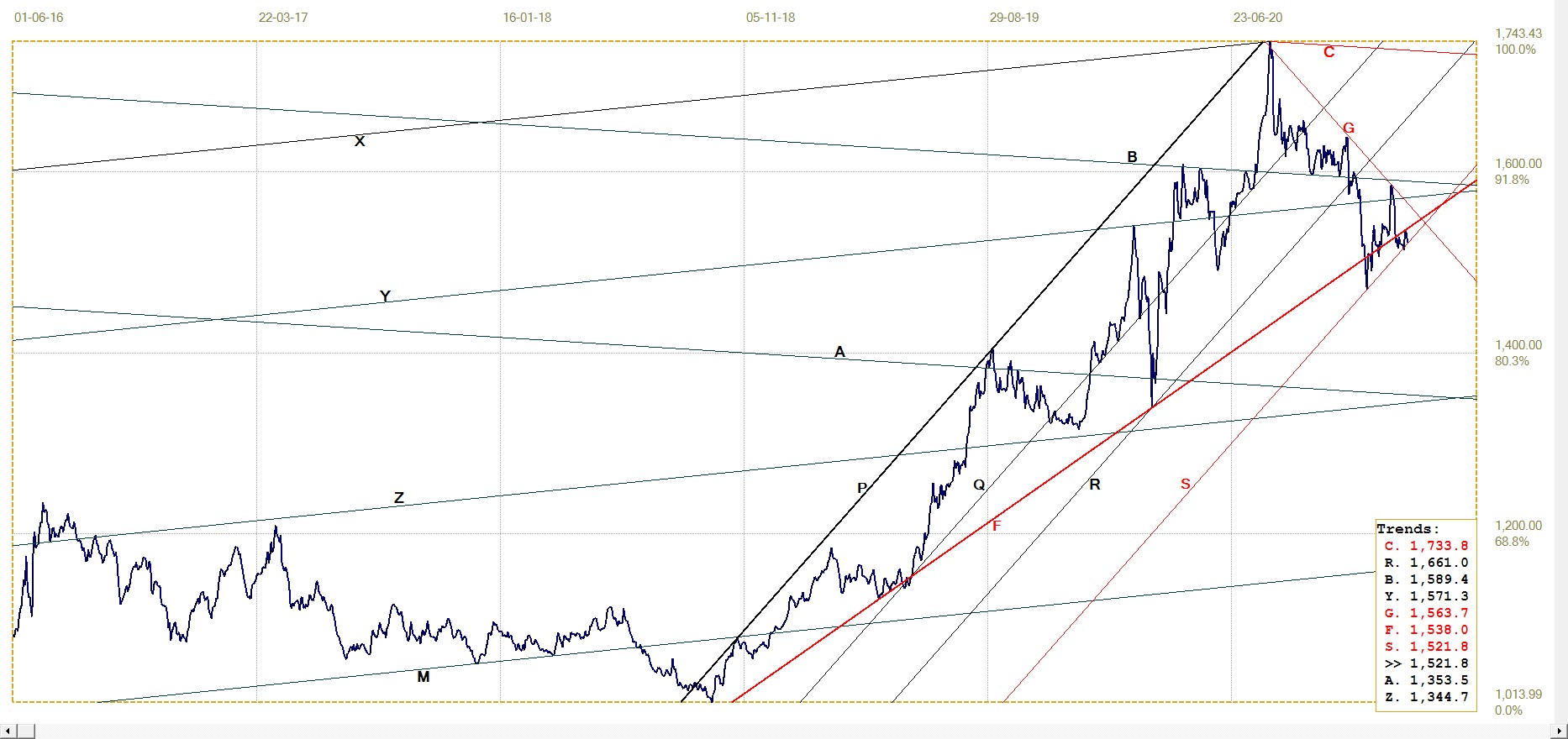

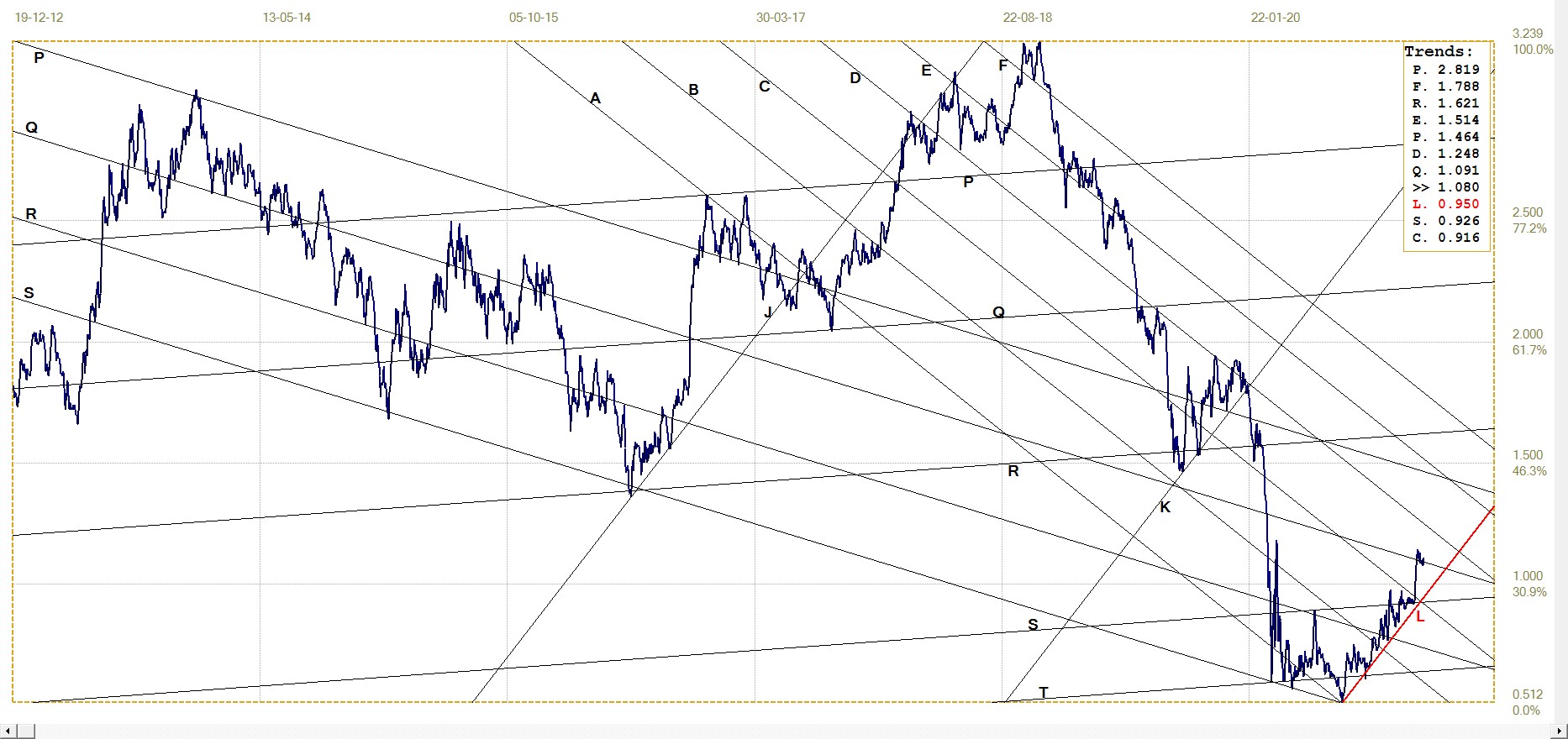

Silver Daily London Fix

The silver chart presents another example of a steep trend reversing as steeply right at a significant trend line; this time also after a break blow steep support, yet remaining within the established steep bull channel. The reversal at line B is more promising than the previous reversals at line C, but there is still a long way to go – with resistance at lines R and A – before silver can claim a new rally high.

Nevertheless, despite the two deep bear spikes, the silver chart currently shows a lot more promise than that of gold after having recovered twice following the major attacks to ensure the profitability of the Cabal’s short positions on Comex. Or was it to reduce the losses they were facing on options and futures? As for gold, the open interest on Comex has not declined to any great extent and the risk should the PM prices explode higher remains.

Silver daily London fix, last = $25.32 (www.kitco.com)

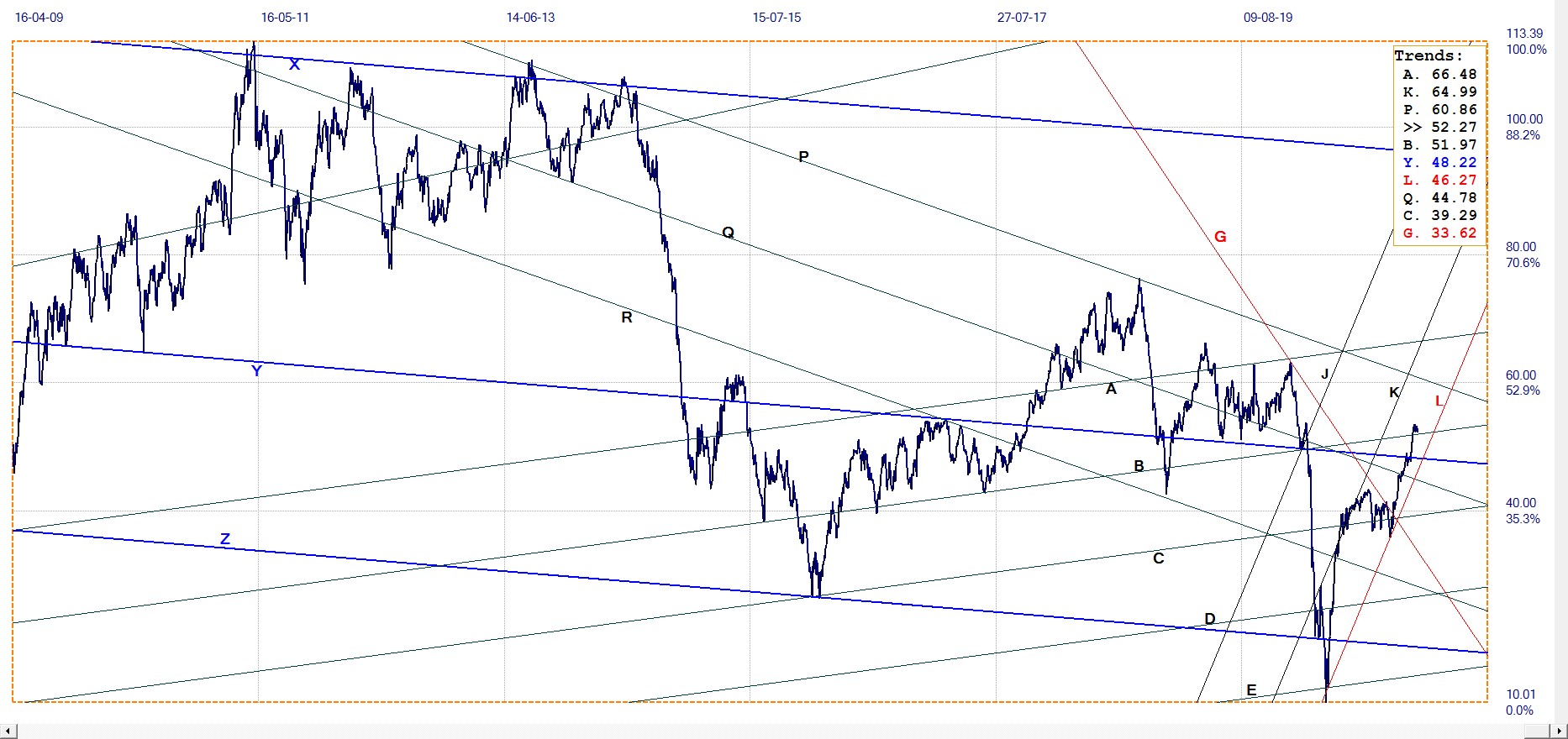

U.S. 10–year Treasury Note

U.S. 10–year Treasury note, last = 1.080% (www.investing.com )

Little really to add to previous comments: The yield managed to break above the psychological 1% level to hold closely to line Q, probably with some in direct or even covert direct assistance from the Fed – it was reported of being in the habit of passing funds under the table to favoured institutions, probably with expectations that these will consult crystal ball readers to be informed of what the Fed would like to see them do with the funds. Some of it surely finds its way into the bond market.

West Texas Intermediate crude. Daily close

WTI crude – Daily close, last = $52.27 (www.investing.com )

The price of crude has also found a level where the forces of supply and demand have found stability – the economic ideal of equilibrium, which is rather rare in most markets, where volatility makes equilibrium a fleeting concept. It looks as if the pipe line decision has left the market blindsided and it needs time to figure out the real implications for the energy market going forward. Or is the market waiting for any other decisions that might affect the energy situation to first be announced before deciding on a new direction for the price?

********