Top 10 Gold And Silver Mining Stocks

Intended Audience

This article is for investors who already own a gold/silver mining stock and are considering adding more. Or, perhaps a savvy investor who is comfortable with risk tolerance and has a general understanding of the gold/silver mining sector.

GSD Top 10

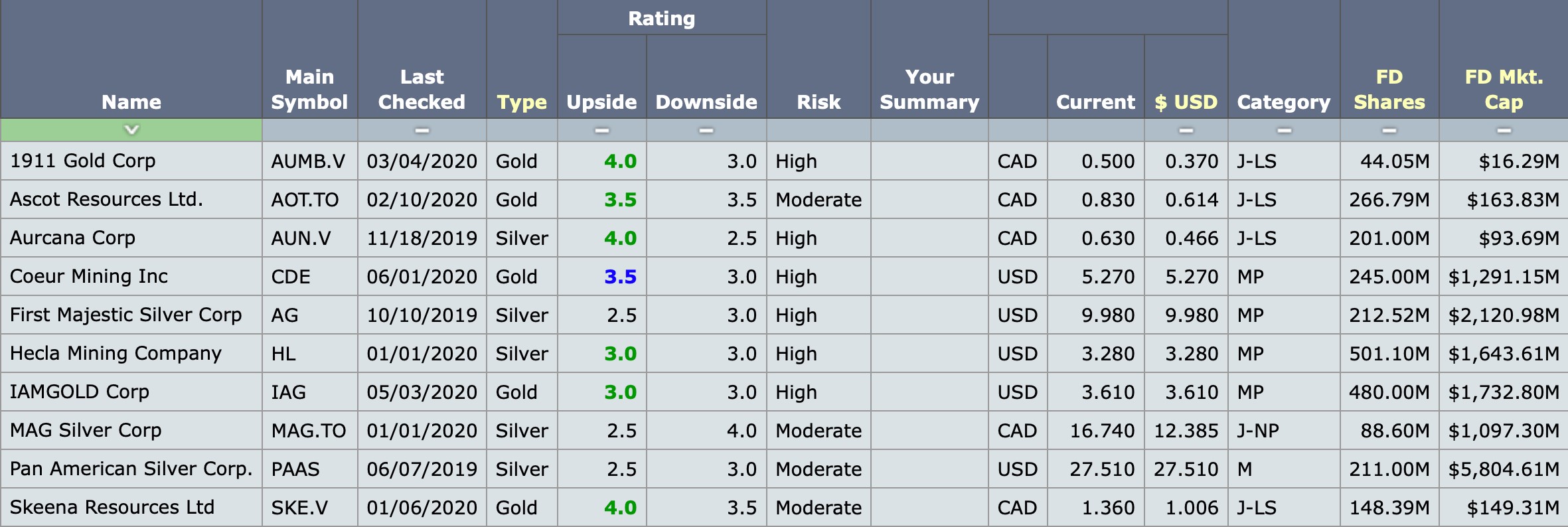

Below is the GSD (GoldStockData) Top 10, which are my current favorite gold/silver mining stocks. There are six with a market cap above $1 billion and four under $200 million. Most of them have 5 bagger potential, although there are three stocks with upside ratings of 2.5, which is a likely 3 bagger.

At the bottom of the article, I will include column descriptions for the Upside, Downside, and Category columns.

1911 Gold (analyzed 3/4/2020)

1911 Gold is a new company that was able to consolidate the Rice Lake properties (125,000 acres). It includes the True North mine (1 million oz at 5.8 gpt) and 1200 tpd mill. This was owned by San Gold, which was valued at over $1 billion in 2011, when it was producing 75,000 oz. Plus, the Ogama-Rockland property has 300,000 oz at 8 gpt.

The new owners have to be excited. They acquired it for a bargain price. They have no debt and only 44 million FD shares with a small FD market cap of $10 million. I'm not sure why investors dislike it so much. The mill alone is worth close to their FD market cap.

Investors seem to be valuing it as an exploration company. However, I think it is a development company. The CEO was the CEO of Tahoe Resources and knows how to build and operate gold mines.

In addition to True North, they have two properties in Ontario (Tully and Denton-Keefer), both of which are early exploration. And they have significant exploration potential on their large Rice Lake property.

Ascot Resources (Analyzed 2/10/2020)

Ascot Resources has a large high-grade gold project in Canada (British Columbia). They have four deposits (Premier, Silver Coin, Big Missouri, and Red Mountain) with 3.5 million oz (7 gpt). Plus, they have a mill that needs to be refurbished that can fed by all four. They have done extensive drilling and are now ready to move forward with development. A feasibility study is due in Q2 2020.

It's a past producing mine and they think it will be easy to permit. The EIS is already approved, which takes the longest to permit. The location is the golden triangle, where infrastructure is always a challenge. However, they claim to have good infrastructure in place from past mining.

We won't know the capex until the feasibility is released. However, I expect it to be around $100 million, which is low for their expected 200,000 oz annual production (if Red Mountain is included). Plus, they are not expecting high costs. My guess is that it will be around $700 per oz for cash costs and $1,100 per oz for all-in costs (free cash flow).

Premier also has a large open pit deposit. Recent drill results (572 meters at 1 gpt) point to a large open pit mine. All four deposit areas have extensive exploration potential on 25,000 acres and 15 target areas. They expect to find a lot more high-grade underground and low-grade surface gold.

Their other project is Mt Margaret in the US (Washington). It has 500 million tons of mineralized ore. It is primarily a copper project but will also produce around 1.5 million oz of gold (.25 gpt with perhaps 60% recovery rates). They are drilling it and have a target of 4 billion lbs of copper and 4 million oz of gold. I expect them to sell Mt Margaret if they get a good offer.

The red flag for Ascot is that they are a takeover target. My experience is that once large projects get de-risked and are near production, they get taken out for a small premium. Thus, likely you aren't buying Ascot, but some unknown larger company. One of these days, companies will realize that gold is going to $2,000 per oz. and they will stop giving their companies away.

Aurcana Corp (Analyzed 11/14/2020)

Aurcana Corp had a market cap of $545 million in 2011 and everything looked great. Then silver prices collapsed from 2011 to 2015. They lost their La Negra mine in 2015 (which was producing 3 million oz per year) to pay off their outstanding debt. Since then their share price has crashed and they have been waiting for silver prices to rise. However, they recently acquired Ouray Silver and their 30 million oz (700 gpt) RV mine.

RV is permitted with a feasibility study. They need to raise $37 million to begin production at RV at 2 million oz annual production. It is economic at $16 silver, with all-in costs (free cash flow) around $13 to $14 per oz. Once RV begins production, they will use the cash flow to return their Shafter mine to production.

Shafter (18 million oz at 240 gpt) is on care and maintenance. They can resume production at around 1.5 million oz per year. The capex to resume production is $20 million. They will need about $20 silver to restart the mine.

They recently did a 5 to 1 reverse split, which is usually the precursor to a financing. I think they will raise $20 million in debt and another $15 million in equity financing to build RV. If they succeed in raising $35 million, they will be in an excellent position to become a silver producer. As a speculation stock, it looks pretty good. When you do the math, their potential annual future cash flow at $100 silver is around $150 million, and they currently have a small FD market cap of $35 million.

Coeur Mining (Analyzed 6/1/2020)

Coeur Mining has underperformed since 2006. They have to reach $70 per share just to get back to where the share price traded in 2006. However, they have been aggressive, purchasing Orko Silver, Paramount Gold, and a mine from Gold Corp. Plus, they tend to have a weak balance sheet, which is currently $450 in debt and only $150 million in cash.

If they can clean up their balance sheet, their share price should take off. But they tend to be spenders and not shareholder friendly. Also, they like to hedge, with almost a third of gold production hedged in 2020. Even with these negatives, it’s a stock you probably have to own because their leverage to higher gold/silver prices.

In 2020, they will produce about 12 million ounces of silver and 350,000 ounces of gold. That is substantial and with rising gold and silver prices, cash flow could reach $1 billion annually at higher gold/silver prices. At 10x cash flow, they could reach a $10 billion market cap. That would make them a potential 5+ bagger from their current $1.5 billion FD market cap. The stock had been surging, rising from $2.48 to $14.94 in 2016, but is now down to $5.95 because of high costs and not a great balance sheet.

They are currently producing about 35 million oz of silver equivalent (including gold), with all-in costs (free cash flow) around $16 per oz. So, they are a high-risk investment at low gold and silver prices. However, if gold and silver prices take off, they will benefit big-time.

I look for this stock to do well, although they need to find some production growth. They have become mostly a gold producer, with more revenue from gold than silver. However, that could even out if silver outperforms gold. The best thing about this company is that 96% of their revenue is from gold and silver, and very little from base metals.

First Majestic Silver (Analyzed 10/10/2020)

First Majestic Silver is a large silver producer in Mexico. Until recently they were a very strong company with a clean balance sheet and low costs. Now they have $150 million in debt and lost money last quarter (June 30th), although they do have $94 million in cash. Their all-in costs are around $17 per oz (silver equivalent). Hopefully, that will drop when their next quarter financials are released.

They will produce 25 million oz of silver equivalent in 2019 (93% of their revenue comes from silver and gold). With this much production, they have huge leverage for higher silver and gold prices. They have 6 producing mines in Mexico.

They have the potential to create over $1 billion in free cash flow at $100 silver prices. At a 10x free cash flow valuation, FM should be worth at least $10 billion at $100 silver. That is my expectation as long as Mexico doesn't increase taxes and royalties, and FM hits their production and cost targets.

The red flag for this stock is their high all-in costs, but they have one of the best management teams in the business and should survive a downturn. Their other red flag is their resource total. They only have about 170 million oz (silver equivalent) of reserves. That seems like a lot, but they plan to increase production beyond their current 25 million oz (silver equivalent) per year. That is only 7 years of current reserves. Thus, maintaining production could be an issue down the road and could hurt their share price. After all, there are not very many large silver mines left to develop.

The good news is they want to become the world's largest silver miner. That is an aggressive goal. They have will need to get lucky with exploration and acquire a few projects. With that aggressiveness, I would expect this company to do well. If they can grow their resources and production, then my future valuation for them (around $10 billion) is too low.

1/4/2020: I was informed that FM has a large potential tax liability from their Primero acquisition and the way the silver stream is taxed (from 2010 until current). On their most recent MDA on Sedar.com, they list a potential $185 million tax liability and that it does not include interest and penalties. Ouch. I doubt they will have to pay the entire amount, but the liability appears to be growing because they have not changed their accounting to match what the Mexican tax authority deems appropriate. Currently, they are in negotiations with the Mexican tax authority regarding this liability and it appears they have refused to pay it.

Hecla Mining (Analyzed 1/1/2020)

Hecla Mining is a silver and gold mining company (about 50/50). They used to be a low-cost silver producer, but they have been losing money. Now they have a poor balance sheet with $584 million in debt and only $33 million in cash. A lot of that debt is due in 2021, so there is very high-risk with this stock if they can't roll it over. To matters worse, their large Lucky Friday mine (6 million oz producer) has been down for more than a year due to a labor strike.

2018 and 2019 were terrible years for Hecla. In fact, they almost went bankrupt. Their share price crashed to $1.31 in 2019. If it went under $1, they might not have recovered. Hopefully, their fortunes will turn in 2020. Their Greens Creek mine in Alaska is world-class. That mine alone is probably worth their current market cap. They have huge resources (10 million oz of gold, and 450 million oz of silver). But their all-in costs and balance sheet have been hurting their share price.

This is a company with huge leverage to higher silver prices. They have several development projects. In the long term, they could easily double silver production. They have two large silver projects in Montana that are being permitted. And they recently acquired Klondex Mines that has big potential in Nevada for increasing gold production. For some odd reason, they don't even include their Montana projects (Montanore and Rock Creek) in their current presentation.

They just need to survive these low precious metals prices. I'm concerned with more share dilution. If gold and silver prices don't rise in 2020, they could have trouble rolling over their debt that is due in 2021. If they get their debt under control, they have significant upside potential. In 2020, they will produce about 10 to 11 million oz of silver and 250,000 oz of gold. If Lucky Friday resumes production, that would increase silver production another 4 to 5 million oz. Until they can show some free cash flow, we won't know their all-in costs. My guess is they might make a small profit in Q4 2019. The first two quarters of 2020 will be important for their performance, along with the price of silver.

They have debt issues, so they are on a tight leash. If their share price drops below $2, then they are losing their top pick status. But if silver price remain above $17, they should be okay. They have huge resources and excellent long-life mines. This should be a 5 bagger if silver prices trend. They have two large silver projects to build in Montana.

There are few mid-tier producers with their resources and pipeline of projects. As a high-risk speculation bet on higher silver prices, it looks pretty good. However, management has been a poor performer. Let me explain why I give them such a poor grade:

1) Their current company presentation is from October and it is now January. Quality companies keep their presentations up to date.

2) On page 4 of their current presentation, they give their performance for 2018! Who cares about 2018? I want to know about 2019.

3) The current presentation claims that they are a low-cost producer with high margins. In fact, they lost money for the first three quarters of 2019.

4) The current presentation does not mention their two large Montana projects, which are both worth $1 billion in my opinion at higher silver prices. Plus, the resources for these two projects are excluded from the presentation. Why?

5) If they are a low-cost producer, then why are the hedging production using a put option?

6) How did they allow debt to reach $584 million, and a large debt payment in 2021 to become due?

7) They say that their objective is to reduce the Debt to EBITDA Ratio to 2.5. However, why don't they have an objective to reduce debt to zero, and use it only to build mines, and pay back the debt quickly?

8) They want to pay a dividend, yet they have a huge debt. Why even have a dividend policy until the debt is paid off?

9) Hecla has acquired a lot of companies in recent years, including Mines Management, Revett Mining, and Klondex Mines. Instead of growing production methodically and accretively, they have blown up their balance sheet.

10) My only conclusion after following this company for 15 years is that they are not shareholder focused. That said, this is one of my largest holdings.

IAMGold (Analyzed 5/3/2020)

IAMGold Corp is a large mid-tier producer, with production at 750,000 oz. They have 4 operating mines in Suriname (northern South America), Canada (Quebec), Mali, and Burkina Faso. They are currently building a large gold mine in Ontario (Cote with 7 million oz), and are spending millions on exploration and advancing properties. I consider this a growth stock. Their cash costs are currently about $900 per oz (forecasted to go down), with all-in costs (free cash flow) around $1300 per oz. That gives them around $200 million in free cash flow at $1500 gold.

They also have two additional development stocks in West Africa. Boto (Senegal) is 1.5 million oz at 1.8 gpt and Sribanye (Mali) is 1 million oz at 1.7 gpt. Plus, they have a few more exploration plays that could become mines. They are giving guidance to reach 1.2 million oz of production in 2022, with all-in costs (free cash flow) of $1100 per oz. These numbers seem optimistic. I'm expecting 1 million oz at $1200 per oz.

Their balance sheet is okay with $864 million in cash and $404 million in debt. With an FD market cap of $1.7 billion, this stock is undervalued. It’s a good income investment for future dividends. In fact, this stock has 5 bagger potential in the long term at higher gold prices. If that happens, your dividend could be around 5% in the future if you invest today. They were valued at $23 a share in 2011. I expect them to be a highflyer again.

Their only red flag is the location of some of their producing mines in West Africa (Mali and Burkina Faso). While both of these countries are safe today, they do have long term political risk. You could consider their debt a red flag, but as long as they do not add any more debt, their balance sheet is pretty strong for the size of the company. Plus, with their cash flow they should clean up their debt.

MAG Silver (Analyzed 11/14/2020)

MAG Silver has an excellent silver project in Mexico. Their Juanicipio project is a JV with Fresnillo and they have a 44% interest. Production should begin in Q4 2020 and it has a 19-year mine life (likely to be increased). Mag's share will be about 5 million oz of annual silver production (more the first 5 years) at close to zero cash costs.

At $16 silver, they will have about $70 million in free cash flow. At $50 silver they will have $200 million in cash flow. The zero costs are from offsets in gold, zinc, and lead. Juanicipio is very high grade (10 to 15 opt) and a high silver recovery rate (94%). The capex is only $300 million and Fresnillo will pay for 56% and is the operator. Mag's remaining share of the capex in 2020 is $126 million and they have $94 million in cash. So, there will be a little bit of dilution in 2020.

Juanicipio is growing in size and they already have several additional discoveries. This mine is going to grow in size. They also have an extensive pipeline of projects and are drilling several: Salamandra, Cinco de Mayo, Pozo Seco, Jose Manto, Mojina, and La Esperanza. The odds are good they will build a few more mines. Mag Silver has the potential to be a very large company.

This stock has exploded to an FD market cap of $1 billion. That's one of the highest market caps for a non-producer. It seems pricey, but I like it as a combination of an income and growth stock. What are they going to do with all of that cash flow? They likely will have a high dividend. Plus, they could acquire additional producing mines and become a growth stock.

The red flag for Mag Silver is they are not building or operating Juanicipio. This means we have no idea if they can build and operate a second mine (or want to). For this reason, my concern (and worst fear) is they will spin-out Juanicipio and remain an exploration company. That would be the easy road for their management team.

Pan American Silver (Analyzed 6/4/2020)

Pan American Silver is one of the largest silver producers. They get about half of their revenue from silver production, about a quarter from gold, and the rest in base metals (zinc, lead, and copper). They recently acquired Tahoe Resources and joined the ranks of silver miners who have diversified into gold.

The combined resources of Pan American and Tahoe are huge. They have about 1.3 billion oz. of silver and 20 million oz. of gold. In 2020, they will produce about 22 million oz. of silver and 500,000 oz of gold. Plus, this does not include their Escobal mine in Guatemala that has had political issues. If Escobal resumes production, that adds 20 million oz of annual silver production at low cash costs.

I tried to inform people that this stock was a bargain under $15 (it was my favorite stock under $15). Now it has broken out to $27 and is not so cheap. I’m still expecting to see it reach triple digits, although that will require much higher gold/silver prices and Escobal back in production.

In addition to being a bit pricey, it has a few other red flags. They mine in Guatemala, Bolivia, Argentina, and Peru. They also have producing mines in Mexico and Canada. Overall, the location risk is significant. But I have confidence that management can find a way to grow. Also, currently, their all-in (break-even) cost per oz for silver is around $15 to $16. That’s not low. But if Escobal comes back online, their overall costs will be much lower.

Gold production is currently giving them a nice cushion. They have solid cash flow from their expected 500,000 oz of production in 2020, with all-in (break-even) costs around $1200 per oz. Plus, they have a pretty good balance sheet, especially for a company of their size. This is because their Chairman (Ross Beaty) is shareholder friendly and understands the value of a good balance sheet.

Looking at potential free cash flow, Pan American is a standout. At $100 silver and $2,500 gold, you could get 45 million oz. (if Escobal is re-started) x $50 per oz free cash flow = $2.3 billion in free cash flow. Plus, 500,000 oz. x $800 = $400 million. That is nearly $2.7 billion in annual free cash flow. If they get valued at 10x free cash flow, that will make them a potential $27 billion market cap. The FD market cap is currently $6 billion.

Skeena Resources (Analyzed 1/6/2020)

Skeena Resources is a development company focused in the Golden Triangle in British Columbia. They obtained the Eskay Creek mine from Barrick Gold in December, 2017. It produced 3.3 million oz of gold and 160 million oz of silver. Amazingly, two years after the acquisition they have already released a PEA.

They plan to produce 300,000 oz annually (including silver). The capex is $233 million, with an after-tax NPV around $500 million. The IRR is very high, around 50% at $1,300 gold. This project is heading to production. It’s a high-grade open pit, with $750 cash costs per oz and a grade of 4 gpt (including silver). They expect the resource to grow from 4 million oz at 4 gpt to 5 million oz at 5 gpt after they complete infill drilling.

They are cashed up, with more than $10 million and will advance the project. The need to complete a feasibility and permitting. I don’t know how much permitting is required since it is a past producing mine. Share dilution will be required, but I expect the share price to rise, making it easier to finance development.

In addition to Eskay Creek, they have two additional projects. Their GJ-Spectrum project (100,000 acres) is a 1 billion lb copper project with about 2 million oz of gold. They released a PEA in 2017 and it isn't quite economic at $1300 gold, with a 20% after-tax IRR to finance a $170 million capex. But this is a pretty good project, with 65,000 oz of annual gold production and very large copper offsets. I would expect it to get built at $1600 gold. They are currently trying to sell GJ to focus on Eskay Creek.

Their last project (Snip) produced 1 million oz at 27 gpt from 1991 to 1999. If they can find another million oz of high-grade gold, this could be their third mine. Hochschild has an option to acquire 60%. They appear to be making good progress identifying new areas to mine.

I expect this stock to go up in value significantly because of Eskay Creek. I’m not sure why it is so cheap. Part of the reason is the CEO has not built a mine before and investors are skeptical that they will build and operate the mine. Plus, because Barrick has a 51% option, which will reduce their upside potential if they take the option. Barrick has until December 2020 to acquire the 51% option. They will have to pay Skeena 3x their costs to date, which will be around $75 million.

2/4/2020: Sold their GJ property for $6 million. They kept their Spectrum property (next to GJ) which has 1.4 million oz (about .7 gpt)

2/19/2020: Spoke to their Investment Relations person. She said they do not believe they have any environmental issues and plan to permit the project while they do infill drilling and the feasibility study in 2021. If all goes well, they could complete infill drilling, the feasibility study, and permitting in 2021.

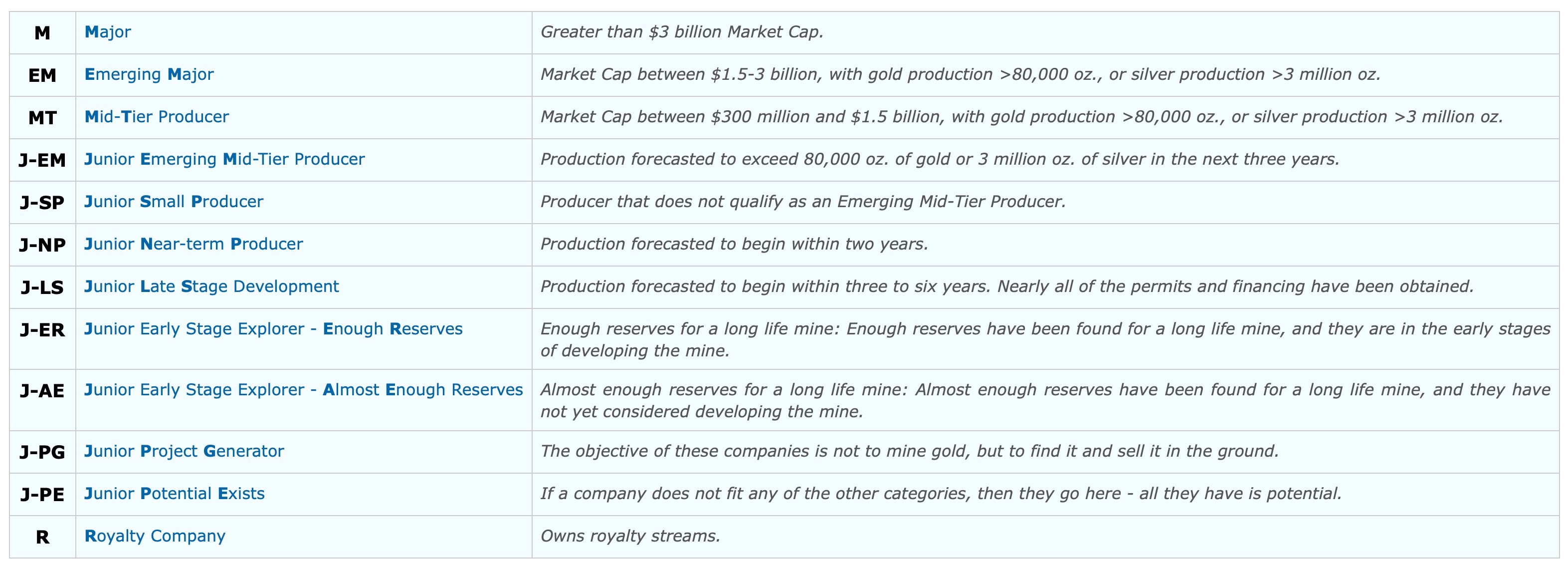

Column Definitions

Categories

If you want a two-week free trial to GSD, please send me an email with a request…and I will set you up to login. Use the Contact Us link from GSD.

Don is an expert gold and silver mining stock analyst, author, and founder/owner of GoldStockData.com – a website for gold and silver mining stock data. He is the author of How to Invest in Gold and Silver: A Complete Guide with a Focus on Mining Stocks. He is a contributing analyst on SeekingAlpha.com and a frequent guest on internet financial podcasts.