Why O’Leary And Holmes Are Both Right On Gold And Gold Stocks

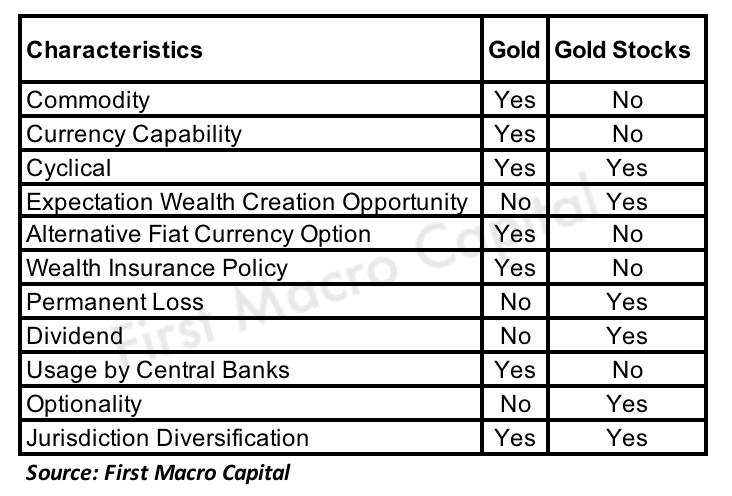

Mr. Wonderful, Kevin O’Leary and Frank Holmes recently took different side the gold(bullion) vs. gold stocks. Gold and gold stocks are two different asset classes and saying which one is better. One is a commodity (Gold) and the other is equity (Gold Stocks). It’s like comparing multiple championships winning athletes, Sydney Crosby (NHL), Lebron James (NBA), and Tom Brady (Football) and saying one of these players is the best athlete of all-time. Gold and gold stocks offer two different purposes for an investor’s portfolio.

WHY OWN GOLD BULLION?

You own gold in bullion form and keep it in storage as an insurance policy for your other financial assets. It acts as a counterbalance against other assets in your portfolio. Investors flock to gold as a “safe-haven” asset, just like cash because they aren’t willing to take on risk. Gold is like a cash position in your portfolio, you don’t get paid to own it. Think of Gold as another currency (cash position) that you have exposure too, and you can use it as a counterbalance against your riskier assets. If gold isn’t important, then why do Central Banks own it on their balance sheet? For investors, it’s a way of being your own Central Bank.

“I have a 5% weighting in gold. The GLD and physical bullion. Which I store and pay for the storage. The value of the commodity is whatever it is every day. Kevin O’Leary (Kitco)

Kevin O’Leary isn’t the only one who has gold as a counterbalance in their portfolio. Here is what Ray Dalio of Bridgewater thinks about gold:

“We can also say that if… things go badly, it would seem that gold (more than other safe haven assets like the dollar, yen, and treasuries) would benefit, so if you don’t have 5% - 10% of your assets in gold as a hedge, we’d suggest that you relook at this.” – Ray Dalio

Egyptian billionaire Naguib Sawiris investing half his net worth in gold

“And people also tend to go to gold during crises and we are full of crises right now. Look at the Middle East and the rest of the world and Mr. Trump doesn’t help.” (Marketwatch)

JP Morgan

“Underweight equities, long duration, long gold, and long the yen as Fed policy slows the economy and real rates collapse.” JP Morgan via ZH

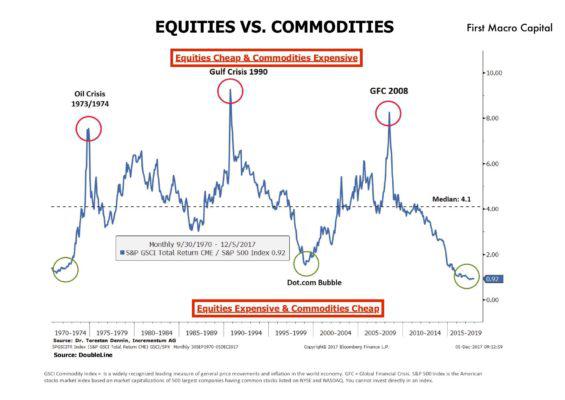

GOLD TRADING LIKE A COMMODITY

After the dollar-gold window was broken in the 1970’s gold trades more like a commodity because it isn’t pegged to the US dollar. That is why gold, has better matched the cycle of the commodity booms since that time. Will it be treated again like before? We think that “Yes, gold will more than likely be pegged in some form to a currency at some point in the future”. Will it be more like past gold standards? Maybe, history repeats, just not exactly the same as before. It could be in a digital format because that is the way the world is going. We aren’t sure. But we follow the worldview that there are cycles and history repeats. We think that the mantra, “This could never happen” means it can happen again and probably will happen, just in a different twist. Everything has a time when it gets center stage. Gold standards will come, and then they will go. For now gold trades more like a commodity.

GOLD STOCKS AND CYCLE

When O’Leary says gold miners are horrible investments is a bit of hype and bluster.

O’Leary: “The history of mining has been abysmal… I don’t need to have a manager in the middle screwing up his capital cost allowance, not controlling his costs. (Kitco)

This is like saying all technology stocks are profitable like Apple.

The gold sector has one major commonality with every other sector. They are all cyclical! The question is, what cycle do they follow? Gold mining stocks and gold are part of the larger commodity cycle. If you understand the cycle, you understand that there is a time to buy and a time to sell. Gold miners generate an incredible amount of free cash flow once the sector has bottomed. Why? Management teams are forced to really look at their costs and focus on generating profits because investors demand it. Just like after the Dotcom bust, investors started to demand revenue, not just user growth. Let me say that again…Revenue! Profits were demanded as well.

Kevin O’Leary is right when he says “More and more investors are thinking the way I do. They are thinking about return of capital.”

But you are seeing it some darling tech stocks right now, focusing exclusively on growth with disregard for profits.

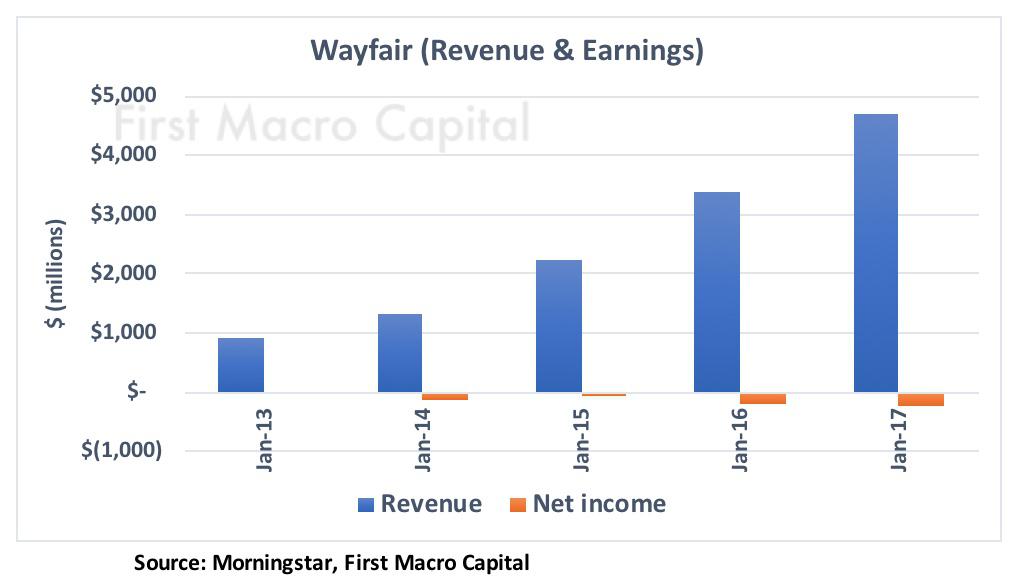

Look at Wayfair, an e-commerce company sells home goods online. Revenues have increased by more than 4X, yet $0 in profits over the past three years.

During the last gold peak, investors demanded growth in terms of ounces at all cost from management, and in the bottom, investors reversed course and realized profits are essential for survival. You know its approaching a top when its ounces at all costs. The technology sector has recently been like this, companies like Tesla(TSLA), Wayfair (W), where it has been growth at all costs. As the tech cycle turns, investors will demand profits from these companies, not just customer growth on Wayfair and auto deliveries from Tesla. This is a 100% guarantee because investors will get spooked when the cycle turns and expect profits. Right now, investors have been rewarding gold miners for delivering on production and showing profitability. In 2017, gold miners delivered record dividends. Gold miners are set to show strong revenues in 2018 because of the continued elevated gold price above $1,300.

"Tesla will be profitable & cash flow+ in Q3 & Q4, so obv no need to raise money," tweeted Musk

OTHER WAYS TO INVEST THAN ROYALTY STOCKS & GOLD MINERS?

But there is more than one way to play the gold sector. I am always amazed, when I speak with portfolio managers and receive emails, they always bring up explorers, producers, and royalty stocks to invest in stocks. Seek where the profits are, and you will find the gold. Look at Apple, it generates the most profits in the cell-phone industry over the past 8 years, its revenue grew incredibly over that same time-period. So why not repeat the same process in the gold sector?

We think there is a better way to think about investing in gold & silver stocks, and commodity stocks in general. Does the company generate a percentage of their sales related to gold and silver? It opens you up to many different companies with exposure to other commodities or other industries. Seek companies that are growing revenue, but still, give you exposure to gold and silver.

We can see the day when companies that derive a percentage of their revenue from precious metals will be added to ETFs.

-

Mining Services

-

Major Drilling

-

KGHM

-

Swick Services

-

-

Financial Services

-

Sprott

-

GoldMoney

-

Canaccord Genuity

-

CME Group

-

Glencore

-

Johnson Matthey

-

Umicore SA

-

Commodities Trading

-

Refining & Distribution

Some of these companies are directly involved in operating mines, by providing useful services to the mining industry. While still being able to get exposure to the gold and silver. The additional value is you may be getting exposure to multiple commodities and in some case entirely different industries outside of mining that are growing.

YOU NEED REVENUE GROWTH

Frank Holmes taking a more factor-based approach, with one-factor, focused on revenue growth. This factor is important because revenue growth attracts investor money.

“The royalty companies have done well and those stocks that basically show better revenue per share, reserves per share, production per share, they far outperform.” Holmes.

And if the company can grow revenue per share and/or cash flow per share this help share prices higher. Would you invest in a company that isn’t growing its revenue? This is why royalty stocks attract investors because they are able to grow revenue consistently over longer periods than the miners. The ability to add cash flowing royalties every year is like adding a new mine but a lot faster than a miner can.

Gold miners’ revenues are tied primarily to two items: 1. Production and 2. Gold Price. Investors are willing to pay up for anticipated growth in production because a new mine is starting up or an existing mine is ramping up for further production. Investors are not willing to pay up for growth, they will sell. The higher the expected growth potential, the higher the anticipated returns. But, watch out if the company slips up. Investors will punish the share price like we recently saw with Pretium Resources and New Gold. When the commodity price is falling faster than the production growth, this will take down all stocks in the sectors. This is why it’s important to focus on higher quality companies, with low AISC or have high operating margins. It minimizes your risks on the downside because they can maintain dividends, and their revenue is less impacted.

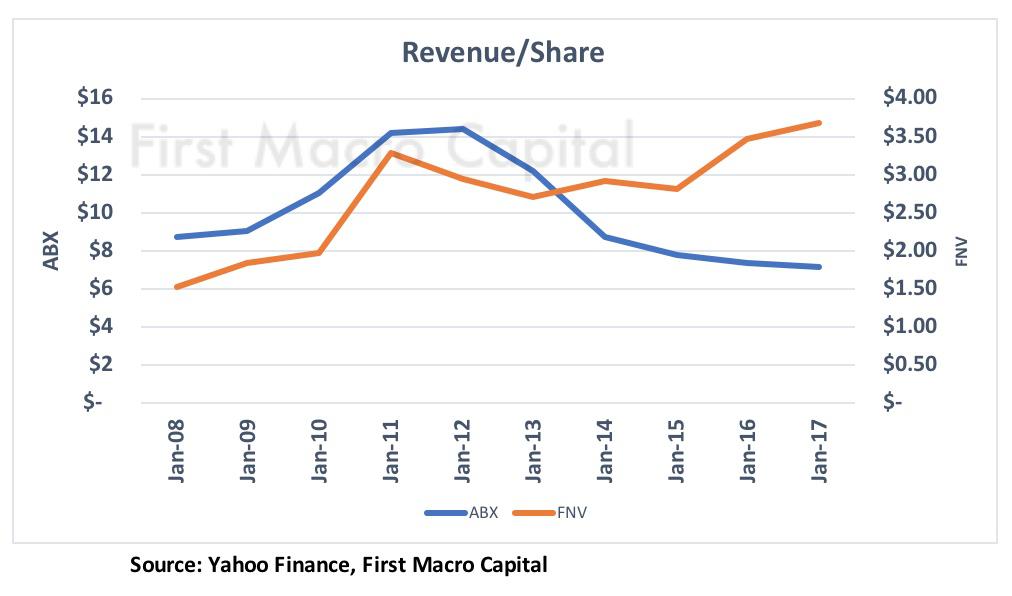

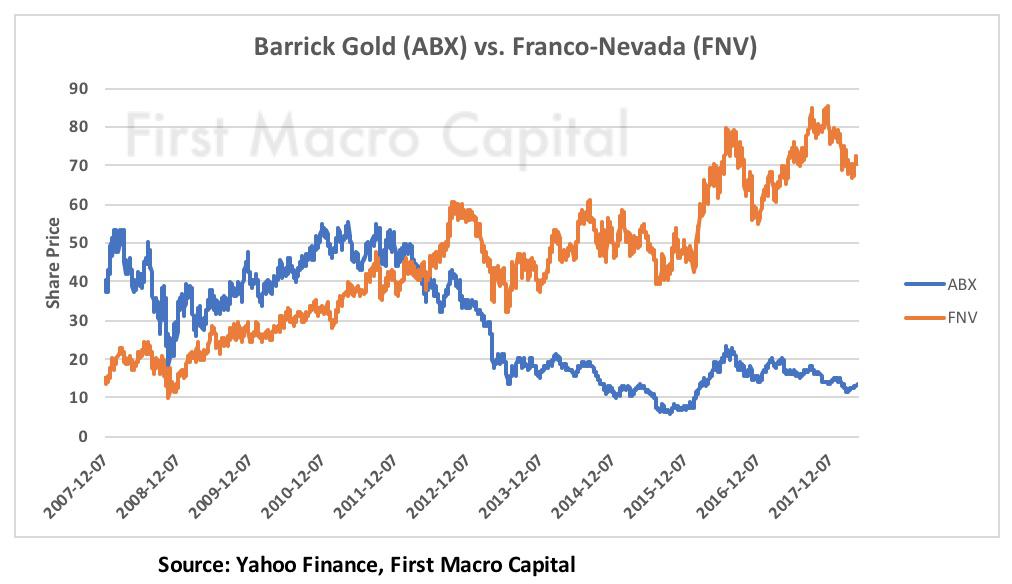

You can see why royalty and streaming companies like Franco-Nevada and Royal Gold are so popular because they offer fairly consistent revenue per share and cashflow per share growth relative to gold miners.

PROTECTION & GROWTH

Gold and gold stocks provide investors with two very different sets of risks and opportunities to protect and grow their wealth. You own gold primarily as an insurance policy against your portfolio and the financial system. You own gold stocks as a way to potentially increase your wealth by focusing on growth, management ownership and catalysts. Two different asset classes that are part of the overall portfolio. By understanding the cycle that they both follow, you can enjoy the ups and take money off the table when the crowd is all in.

Written by Paul Farrugia, BCom. Paul is the President & CEO of First Macro Capital. He helps his readers identify mining stocks to hold for the long-term. He provides a checklist to find winning gold and silver miner stocks and any commodity producer.

Disclaimer:

The information contained herein is obtained from sources believed to be reliable, but its accuracy cannot be guaranteed. It is not designed to meet your financial situation – we are not investment advisors, nor do we give personalized investment advice. The opinions expressed herein are those of the publisher and are subject to change without notice. It may become outdated, and there is no obligation to update any such information.

Investments recommended in our publications, blog posts, emails, online communications, or any online contents published by any party of First Macro Capital and its affiliated companies should be made only after consulting with your investment advisor and only after reviewing the prospectus or financial statements of the company in question. You should not make any decision based solely on what you read here.

First Macro Capital writers and publications do not take compensation in any form for covering those securities or commodities. First Macro Capital employees and agents of First Macro Capital and its affiliated companies own some of the stocks mentioned in this article, prior to the writing of this article.

*********