Winds Of Change

One often hears of a Chinese curse that states the cursed one should be destined to live in interesting times. This is intended to imply times of historical interest generally were not very idyllic for the people alive at that time. Many of whom did not survive to enjoy a later peaceful and quiet time historians considered of little or no interest. Prior to the 20th century, times of much interest tended to be confined to limited regions. However WWI and more so WWII have changed this. Since then, periodic waves of change have swept across the global scene, enough to keep historians very happy. Yet, the changes of the past 10 years are like a tsunami broiling up across the world.

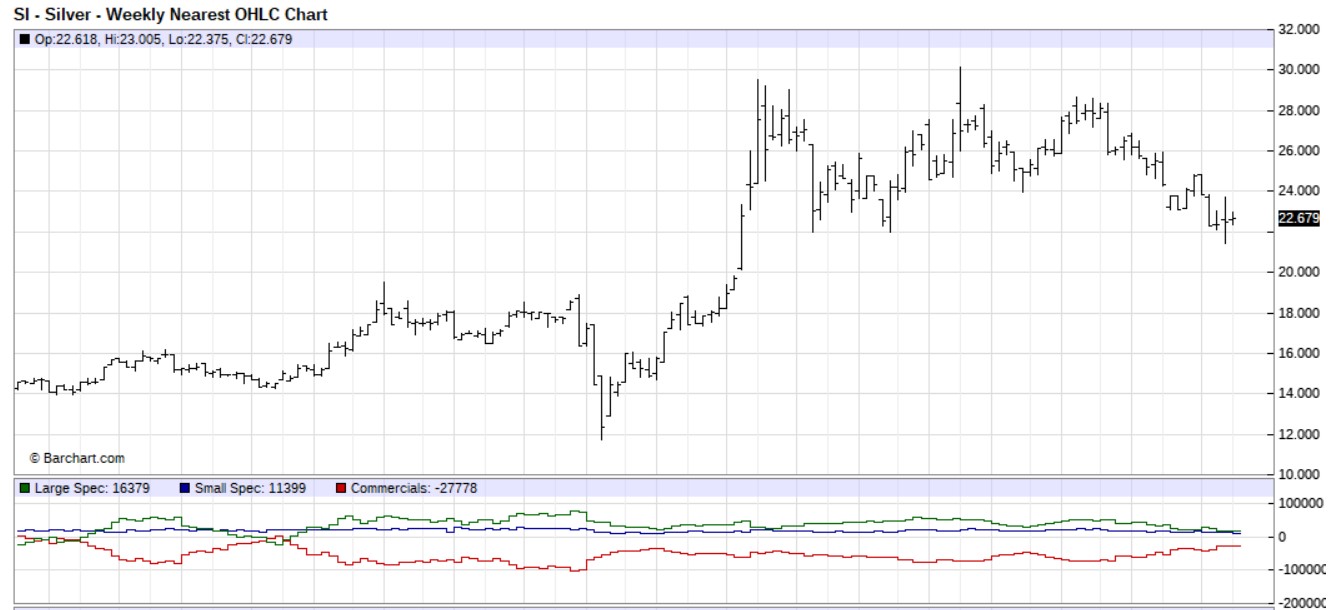

Last week it was speculated here that the Big Banks, eager to reduce the risk of a short squeeze should something set off a major new rally in gold and silver, would continue to pressure the metal prices lower, with the price of silver being the primary target. This did not materialise, since both prices ended last week on an uptrend.

The CoT chart from Barchart.com is as usual a week behind, with the latest price and net short positions dated 4 October. The week on week change in the Commercial net short position is from -28 648 to -27 778. The minimal 70 contract decrease in their net short position could have compelled them to re-evaluate their strategy. The net long position of the Large specs changed from 16 705 to 16 379 – a more significant change by 309 contracts, the Small specs being responsible for the difference.

The Big Banks must have realised that a lower price for silver has the desired effect to have the Large specs go more short. However, the Small specs get excited by the new low price and they buy almost as many contracts as the Large specs go more short. By pushing prices even lower, they are on a win-lose situation, being snookered by the Small specs. That realisation might be why the price of silver bounced last week.

Since the gold price was also used to create a negative sentiment among the PM bulls, it made sense to also let gold enjoy a breather. This is not good news for the PM bulls, however. With the Commercials still close to being net short by 30k contracts and not standing to gain much from a lower silver price, they have to revert to their old game of letting the price run higher and then performing the usual month end ritual.

The decade behind us is one of major global change. A few of the developments that are both a break from past trends and set to effect significant change on the current new decade are:

* The shell-shocked US and other western economies failed to recover following the financial crisis of 2007/8. Despite the record low interest rates for all of the decade, economies of Europe and the USA had to receive financial life support and still do

* China extended its growth that had a slow start in the 1990s, but was speeding up when the last decade started. It soon became the second largest economy in dollar terms, yet achieved superiority in PPP terms. This progress enabled China to launch new initiatives; economically with development such as the new silk road, the effects of which are still accumulating, and an interesting triangular geopolitical stance with Russia and the US that has a bipolar friend-enemy relationship with both

* Woke Europe had its own interesting historical experience when the destabilisation of the Middle East and terror activities in Africa saw a wave of mostly Muslim refugees using all means of transport to get into Europe. Initially, they were welcomed with open arms, being received as young and vitally important additions to the labour force in an aging Europe. Perhaps, within a decade or two – shorter even should the many young refugees, once they have joined the labour force, import a wife or two from the Old Country to begin a family – most of Europe will find itself under Shariah law and no longer allowed to be woke.

* Since the early 1990s and through the past decade, the US have had four presidents of different political affiliation. Yet the first three of the four, all with double terms in office, mostly remained within the same policy envelope set during the Clinton years. It took Trump’s election to break the mold, but his reign came to an abrupt and still disputed end late in 2019. The changes since then have set the US on a very different new path, in part because of the polarisation of American society – a condition that has been simmering for quite a long time. This division exploded onto the headlines with the run-up to and results of the November elections and its aftermath.

Then, as the decade rolled to a close and after being brewed in the virology labs for nearly two decades, the Covid-19 virus became the most talked about, contentious and devastating event since WWII – with potentially greater effect on the future of the world than was wrought by that conflict of 75 years ago.

A “perfect storm” has become the term of choice, drawn from the rare occasions when different weather system collide, for when different factors that have adverse effects on an economy or society come together to amplify their individual disruptive powers into a near cataclysmic event. Events and developments during the previous decade, culminating in Covid-19 appear to be setting up the new decade for a global perfect storm.

Given persistence in trends that have been developing and with due allowance being made for welcome or more disruptive surprises, the next nearly 8 years should see major changes taking place on the global scene. The so far considered to be mostly woke concerns about climate change and water scarcity and the environment can be expected to migrate to higher on the main “necessary to take action” list.

China’s aspiration to be The Global leader is likely to succeed, unless the exceptional weather they have experienced recently persists to create havoc with their major river systems and perhaps disrupt industry even more so than what has recently happened. Wages are increasing so that the new decade could see some cheaper Asian countries obtaining a greater share of new manufacturing opportunities. As the export oriented growth in China slows, a greater emphasis has to be placed on internal growth. This in turn will begin to suffer as Chinese demographics begin to change, becoming an older population as is already happening in Europe and in Japan.

Europe will find it increasingly difficult to reconcile greater productivity in the north of the Union with the more laid back and migrant saturated south. Although Germany in the north will have her own problems trying to assimilate the Muslim migrants without them inciting a conservative backlash as the migrants cause more problems.

The US seems set to follow an anti-climate change route into the future, but doing so in a manner that is impulsive and with too little regard for the consequences of the new policy. This is one effect of the change to a more woke mind-set among a large section of the population situated mostly along the two coasts.

Unfortunately, wokeness seems have too much of a sense of entitlement in its make-up, where diversity is promoted provided this does not conflict with the desire for uniformity. The apparent paradox of this statement becomes clear when diversity is promoted in appearance and individual social and gender freedom. Conformity on the other hand, is essential for politics and solidarity with the prescribed social dogma of the left. Tolerance is good within the fold; intolerance for those who are considered to be reactionary or old-fashioned is justified and expected to be expressed openly.

For 2000 years and more, people of Caucasian extraction, building on the older Greek metaphysics and culture, dominated accepted history, largely because of growth in technology and an expansionist nature. Since the mid 20th century the tide has been turning against the so-called “Europeans” – the dominant people who live in Europe, North America and various outposts of the British empire. They are being swamped by numbers, no longer have their earlier superior control of technology and weaponry. They are losing their self-confidence and trust in the leadership role they have played on the global stage for such a long time. We are losing our vision and mission.

As all these changes continue to develop and take place, the next few years are going to be very interesting for those lucky enough to survive largely unscathed. 2020 with Covid rampant, the US under pressure from migrants, as was happening in Europe –initially one tried to press back the tide while the other felt obligated to open the gates, but both to feel the effects of this invasion before too much time has passed.

China remained dominant in global trade, the Afghan war still being fought and the economy still was suffering the effects of 2007/8. This must have been very different from what most people could envisage in 2010.

2030 probably is going to be even more strange than we could have imagined from a time before Covid-19 had been named and when the US military still controlled much of Afghanistan and while Biden was still pondering how many of Trump’s changes to turn back and which new changes to make and how soon. But by 2030 the changes would have accumulated to make the world much changed from what we knew early in 2020. Time flies and the road ahead is going to be interesting to observe and also to experience!

Euro–Dollar

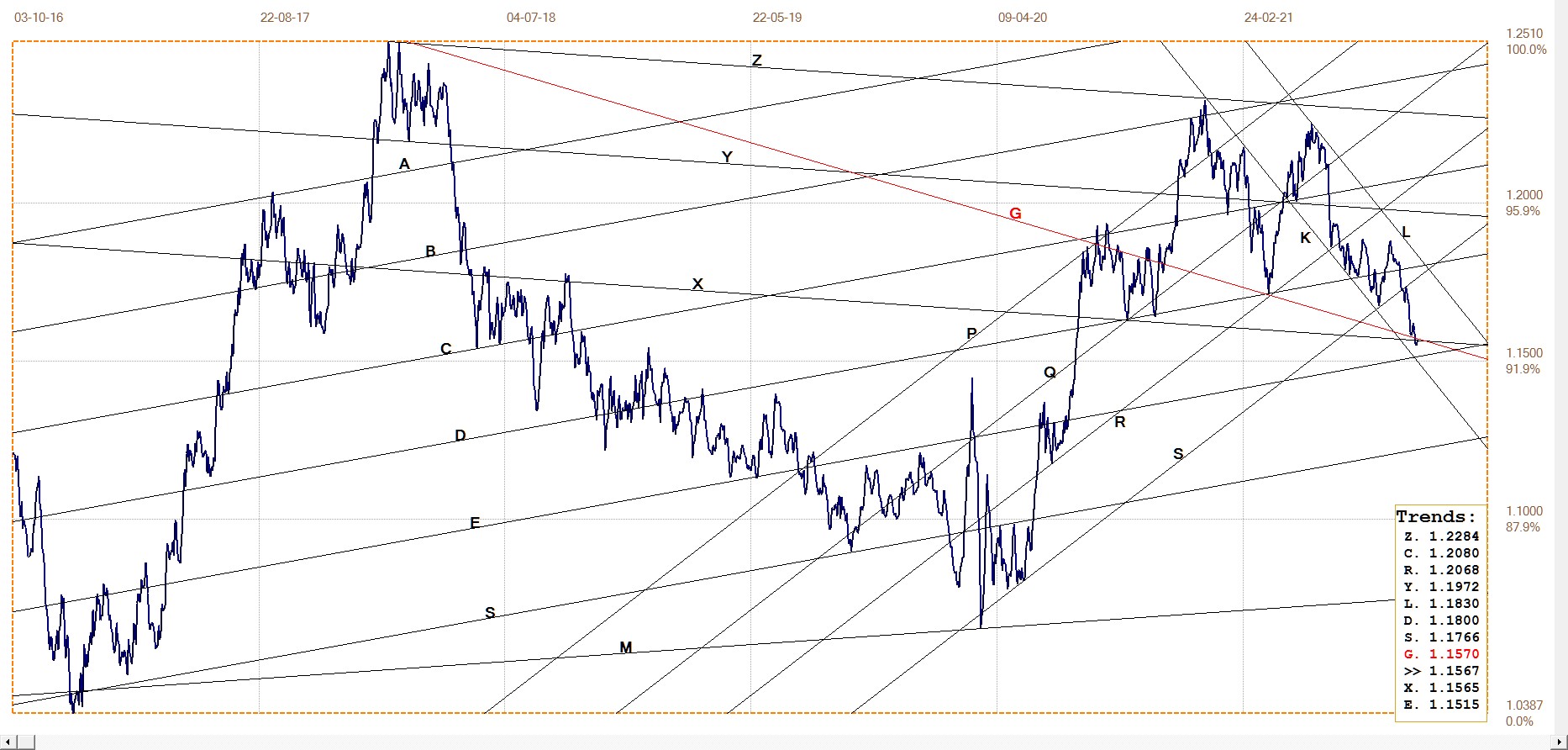

Euro–dollar, last = $1.1567 (www.investing.com)

The dollar index strengthened to above 94 on two occasions during the past ten days, taking the euro lower in channel KL to test its support along lines G and X. Last week the euro marginally overshot its support, but managed to close the week back in touch with it. This week will prove whether the support is going to hold, or whether the dollar is going to remain bullish to see the euro testing lower support along line F. Technically, the trend for the euro remains bearish as long as channel KL holds.

DJIA daily close

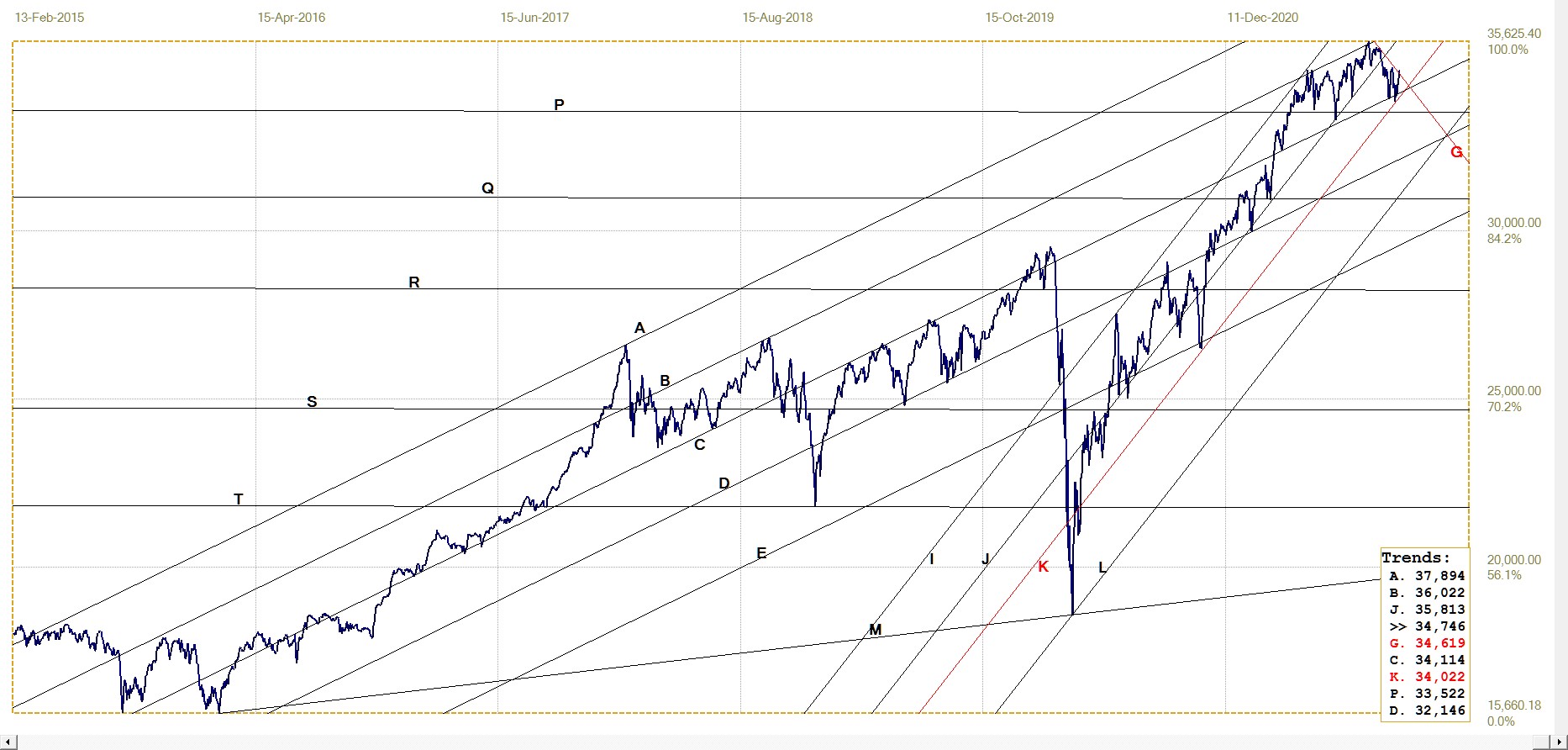

DJIA. last = 34746.25 (money.cnn.com)

The volatility on Wall Street is nevertheless keeping the DJIA between the resistance of line G and the rising support of channel JK. The close on Friday is a fraction above line G, as if to give a bullish signal. Line G is quite steep and its value in the Table is the value of line G on Monday, one day ahead of the actual price data. Recently, the start of the week on Wall Street required much boosting to close the day in the green and this Monday may not be an exception – unless the sellers gain control of the stock market for a change.

The volume of the Dow 30 stocks recently has exceeded the 5 month average on a few occasions to reveal that profit taking – or is it fleeing the market? – is building momentum. So far there is no panic, but the poor NFP number on Friday did put a stop to the preceding three-day rally. Many investors are certain to spend time over the weekend to ponder the question whether it is wise to remain invested.

At the same time, Bitcoin and other crypto currencies are showing signs of coming out of the China-induced slump and many non-institutional investors, including the many RobinHooders, must feel tempted to change from a market struggling to hold its level to one that, so all the crypto videos on YouTube have it, will go to the moon.

And beyond.

Gold London PM fix – Dollars

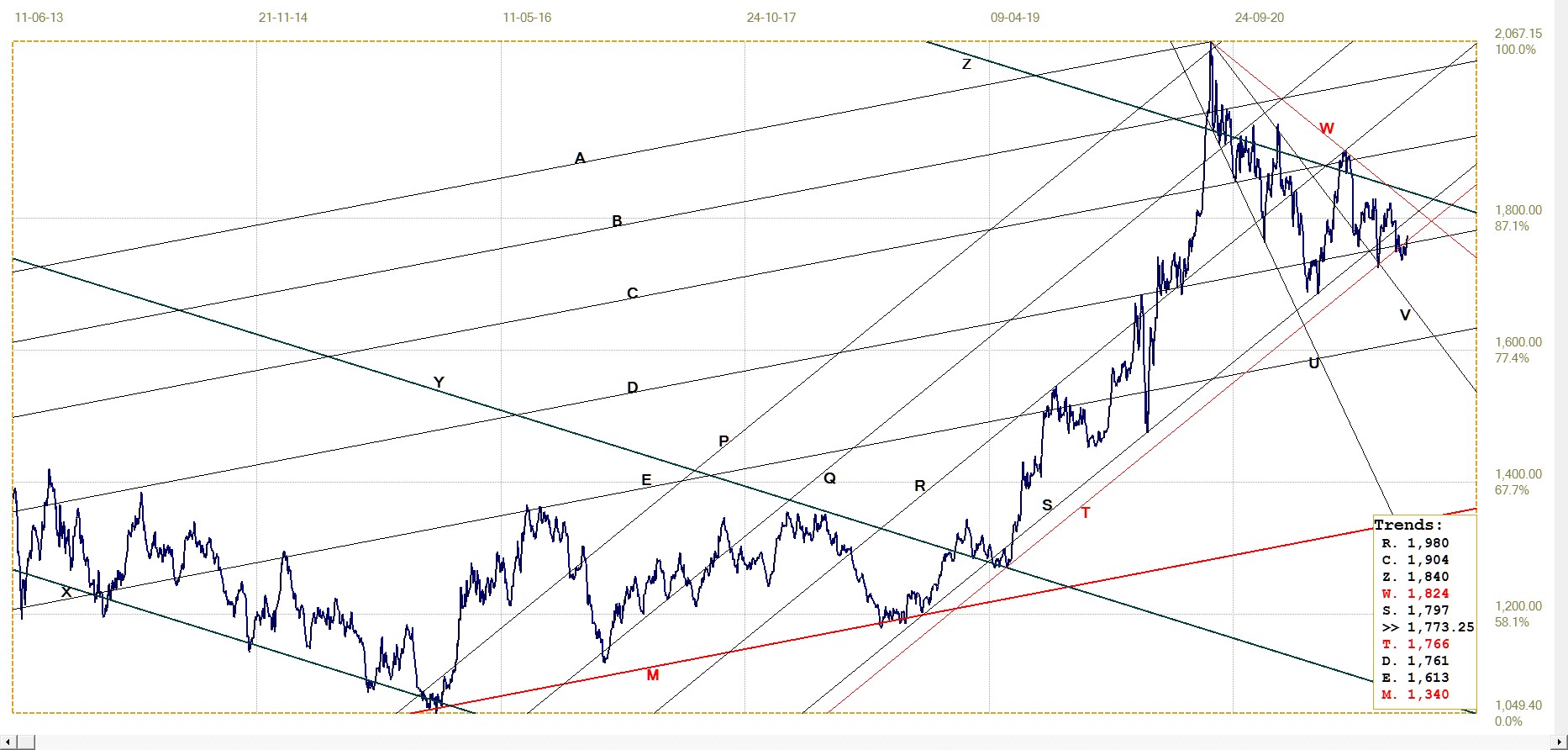

Gold price – London PM fix, last = $1773.25 (www.kitco.com)

The stronger dollar index also took its toll on the price of gold, which for almost three weeks has dropped below line T, the extended support of channel PQRS. Last week the price posted a bit of a recovery, enough to break higher above line T and also back into channel CD. As discussed earlier, this still minor recovery might be the sign that the Commercials have discovered they have been feeding the silver Small specs with cheap contracts at the recent low prices of silver, which is counter-productive for their net short position.

They also had to let go of the price of gold to allow the small recovery back into safe technical territory – yet that might be as far as they will be willing to relent.

Euro–gold PM fix

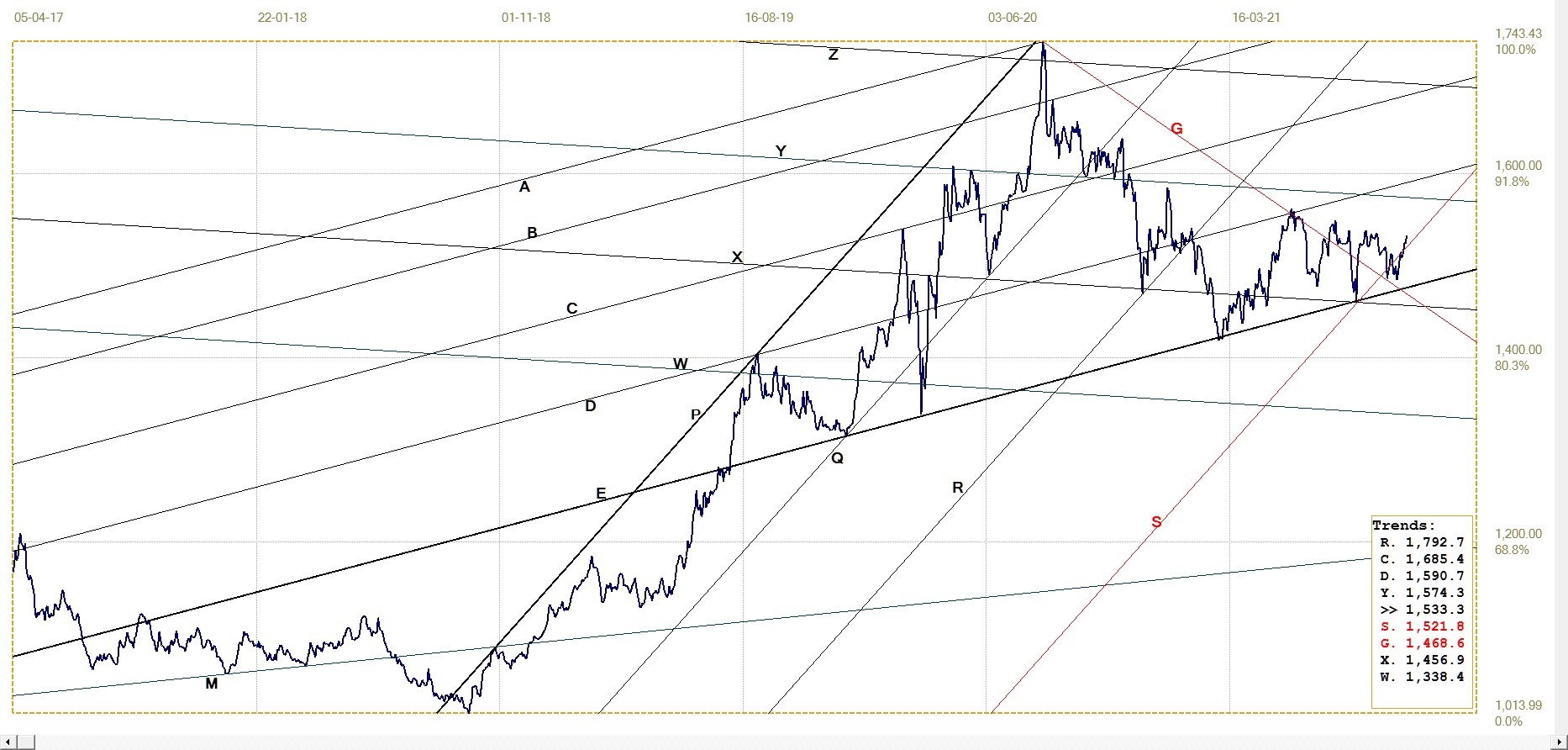

The euro-price of gold has again recovered into its main bull channel, being boosted by the cheaper euro and the small bounce in the price of gold. Technically this looks quite bullish again; still, much will hinge on what the dollar will do now.

It looks as if the price of gold will have some freedom to regain a bit of glitter, but not so much that it inspires even a mild bull run. The Cartel has recently held the ceiling at $1800 and that is likely to remain in place to also put a cap on the euro price of gold, at least for the time being.

Euro gold price – PM fix in Euro. Last = €1533.3 (www.kitco.com)

Silver Daily London Fix

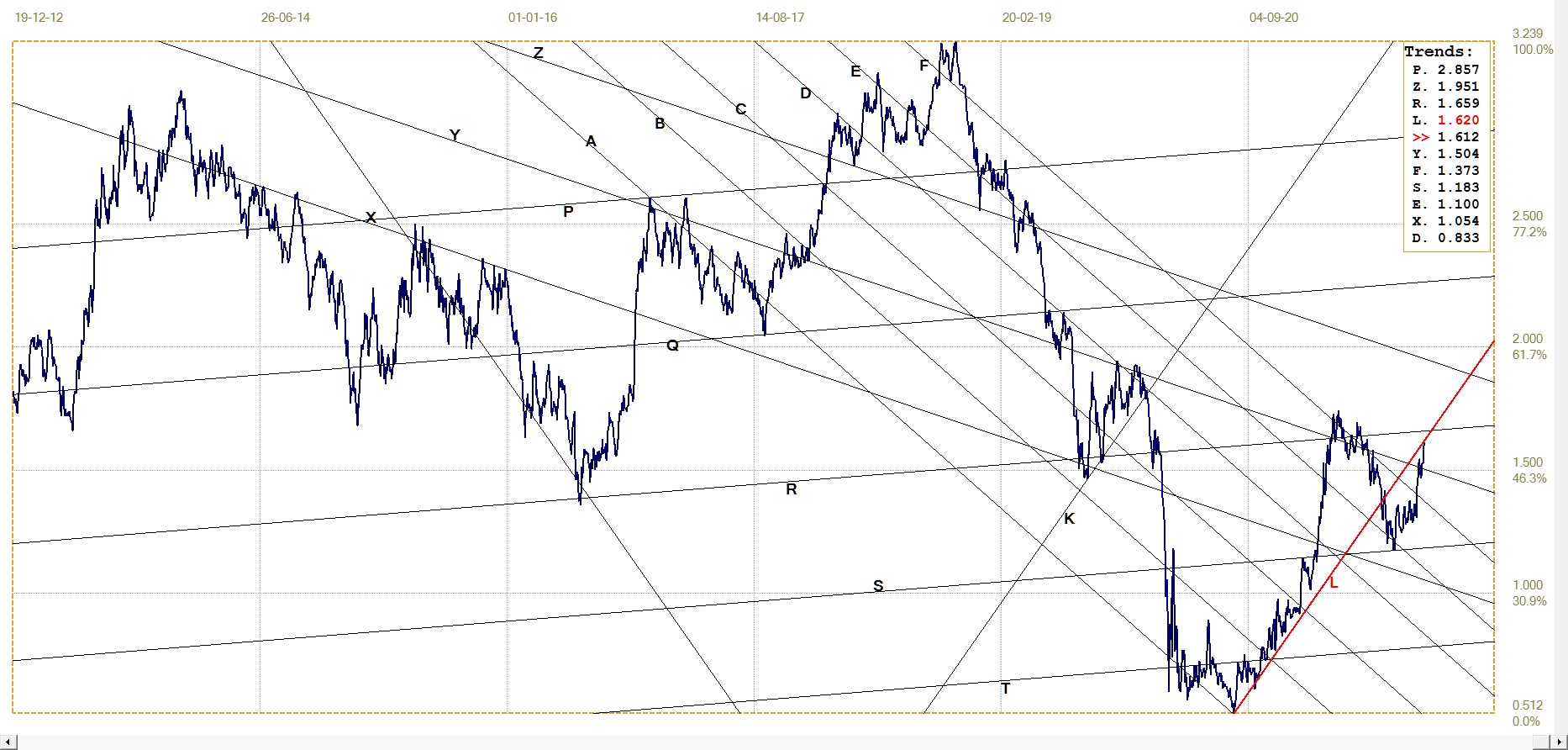

Silver daily London fix, last = $22.53 (www.kitco.com)

The daily chart of silver better displays the presumed change in the mindset of the Commercials during the week ending on 1 October. Last Monday’s CoT showed that the Small specs had bought more than 300 new contracts the week before, while the Large specs had only shed 70 contracts. The sudden and steep rebound from near the horizontal divided on the chart along line H is too abrupt not to be a change of mind by the forces that really control the silver futures market.

Whether the price will be allowed to go much higher soon remains to be seen. A test will be to see if the price of silver contracts remain in bear channel XY or not. It is a steep and quite narrow channel and we should know by the end of the month whether it will hold or not. For the time being, and with line Q also acting as level of resistance, it looks as if a challenge on $24 is not on. Even $23 is likely to be held as a ceiling so as not to get the silver bulls too excited.

U.S. 10–year Treasury Note

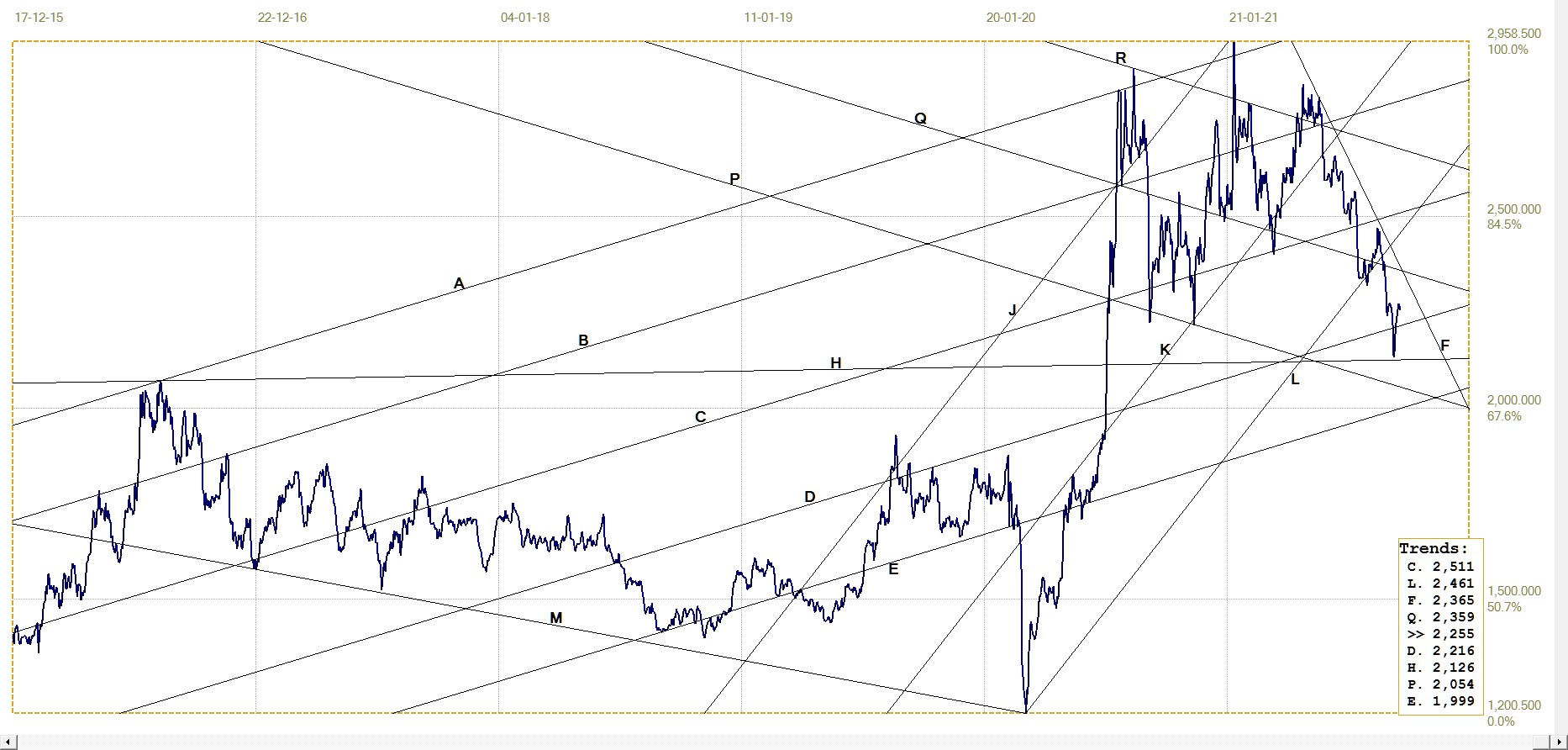

1.10–year Treasury note, last = 1.528% (Investing.com )

The recent break above broad channel AF, first reached and held around line Y. It has now spiked higher to test the bottom of channel KL from which it broke lower at the time when inflation started to rear its head, but was not perceived as a new threat.

The new trend lower did not last very long, yet the reversal higher to signal that the spectre of inflation has not disappeared was contested as the yield moved higher in two small steeps higher followed by one back. The new spike higher suggests that the market is deciding that inflation is not going to be transitory. Confirmation will come with a definite break back into channel Kl.

West Texas Intermediate crude. Daily close

The price of crude oil has suddenly spiked higher off a low below its bull channel JKL, much like the yield on the US 10-year Treasury has done. One could surmise that the reason is similar – a realisation that inflation is here to stay and trend higher. On the other hand, the energy crisis in China might be perceived as a harbinger of what is going to happen in the rest of the world, and perhaps even for the same reason – a shortage of coal.

Coal mines have been reported also to be in Biden’s cross hairs as he pursues a policy of the US doing its bit to ensure that US summers do not get too hot and winters bring enough snow and other precipitation to keep the rivers flowing and the dams full. With China likely to hijack as many foreign sources of energy as possible and US production of oil also under some climate threat, no wonder energy is becoming more expensive and helping to fuel inflation.

*********