Winning A Battle Is Not Winning The War

My optimism last week that the gold and silver longs would mostly ride through the attack on the metal prices holding onto their positions, perhaps buying even more, was a little too rosy. What surprised me was that while we are used to the waterfall attacks in New York, the price suppression this time was more of the old sustained selling and selling that forces the price gradually lower over an extended period. It surely has to be more expensive than the flash crashes in terms of the number of new short positions needed to achieve the objective. More amazing was when the consistent bear trend was also present in Shanghai. I would guess that there is a big vault full of gold and/or silver that appeared as a large overhand on the market there to frighten off potential buyers.

Just a guess, but doing it in that way, having large sales orders at or just above the lowest offer coupled with small and judicious sales at the bids, can send prices lower without having to deliver too much of the metal. That is the only tactic that makes any sense, because actually selling the metal in Shanghai when it is going to be needed in New York at some point in time is just plain foolish. Delivering metal in New York so that the buyers pay the transport to Hong Kong and China is much more sensible! Of course, if they had enough supply to sell into demand in Asia, it would be safer to do that. As it stands, consider the reaction should this speculation be true, and some large buyer comes into the market and takes out the whole offer stack. Just like flash crashes on Comex have done to the stacks on the bid side!

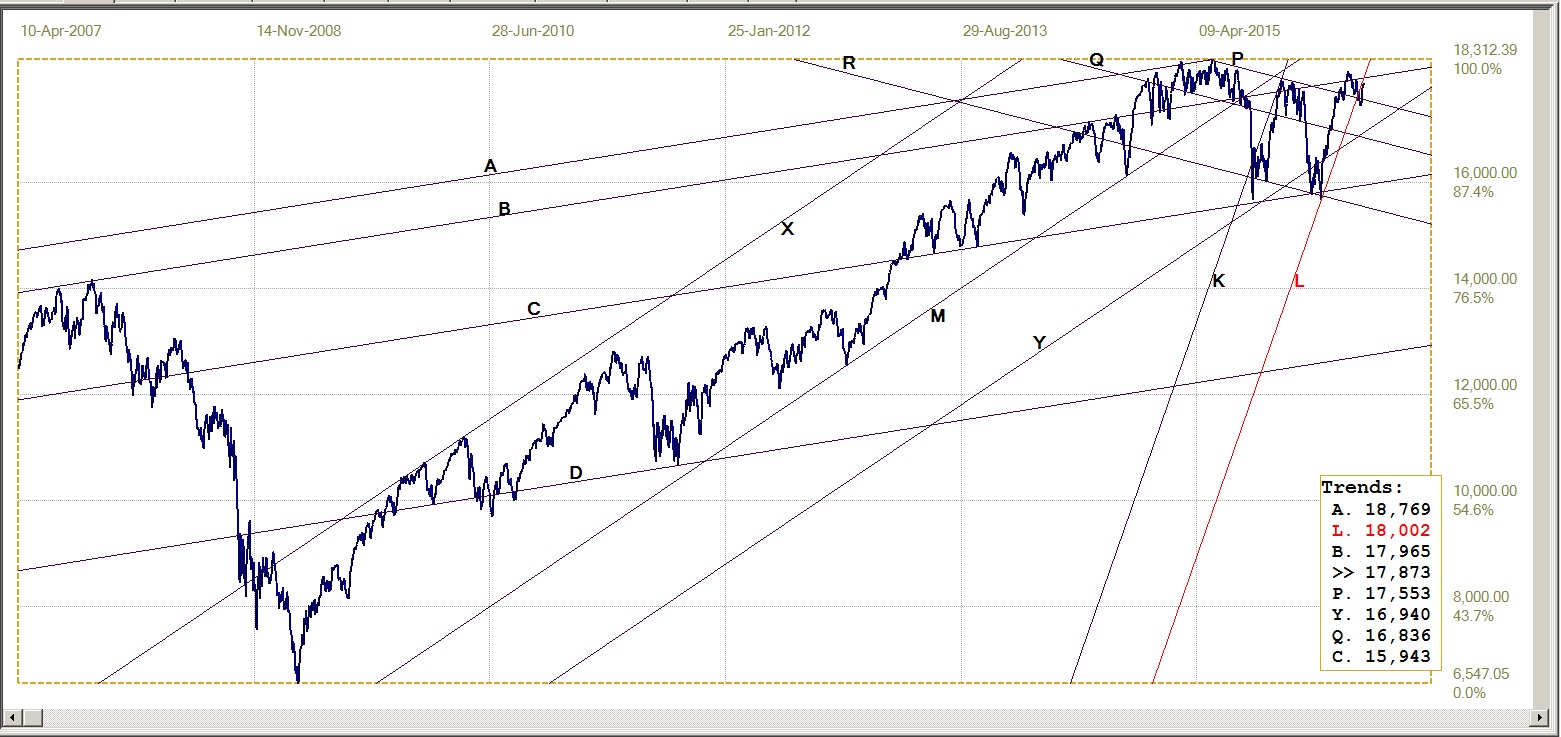

The dollar and Wall Street were also victorious in the major rear guard battle of the past few weeks. After coming close to testing the 92 level early this month, the US dollar index was getting close to challenging the 96 level. Japan apparently received a message not to intervene in the strong yen, implying that a weaker dollar is now on Washington’s wish list. So is a DJIA above 18000, but that target remains just out of reach despite repeatedly starting intra-day rallies the past few weeks. They seem to fade right when it looks as if 18000 could be reached within 2-3 days. A DJIA close near 17700 on Wednesday could set up an interesting monthly chart.

Unless there is a wish to upset the financial apple cart, the new rising trend in the yield of the 10-year Treasury is not the direction of choice for those in favour of a status quo in US markets. The 2.0% level still stands as a psychological Rubicon in the bond market. On two occasions since the steep bull market that ended in mid February, the yield shot up as steeply, breaking clear of the 1.9% level, but it then reversed lower as steeply, as if someone had switched on a purchasing algorithm. Now the yield is again above 1.8%, but is now holding there. Perhaps to prevent a third and this time an unlucky break clear above 1.9%.

This is the umpteenth major battle in the drawn out intensive phase of the war that must preserve the shine on the US economy and the US dollar that was launched in 2011 after the gold price had reached a new post bear market high. The dollar was strong into late 2015, while Wall Street had a number of near miraculous recoveries since 2011 before also peaking in late 2015; and is now trying to do it again. So far the results in these battles have been consistent. But as the recoveries in the prices of gold and silver during 2016 has shown – and the battle for DJIA 18000 raging – the war is not yet over and the outcomes not nearly as certain as people may think.

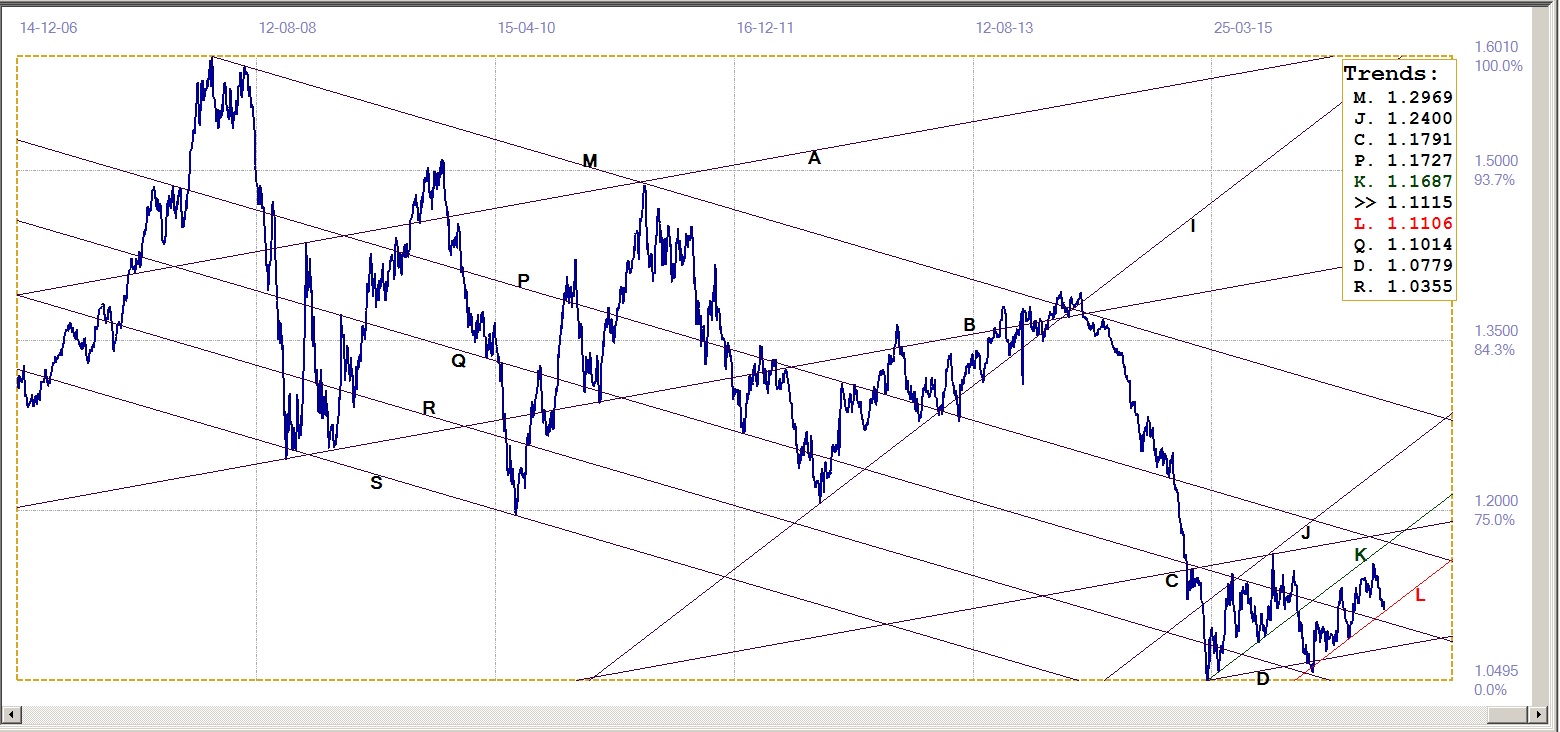

Euro-Dollar

The euro is continuing its ‘zig-zag’ rising trend, having again extended the ‘Zag’ to close lower than the previous week. The weaker euro is not good news for people who wish for a weaker dollar, but perhaps next week could favour them now that the euro has reached the bottom of bull channel KL ($1.1106). A break lower could imply the euro is in a sustained bear trend, unless a recovery happens very soon.

It is difficult to say in which direction fundamentals in the respective economies are likely to send the two currencies; using all manner of subterfuge to present pictures of economic health downplaying the amount for visible debt, Europe and the US are both trying to gain the economic upper hand on the ratings, yet keep increasing the money supply of dollars and euros in an attempt to stimulate some growth. How it will play out in this game could be revealed by what happens next at line L.

Euro-dollar, last = $1.1115 (www.investing.com)

Dow Jones Industrial Average (DJIA)

The recent marginal break below steep bull channel KL (18002) has now increased as the DJIA failed to hold pace with the steeply rising channel. The DJIA is also still below the resistance at line B (17945). Technically though, the way is almost clear for another attempt on the 18 000 level and perhaps a recovery back into channel KL. The market now has a definite bearish bias after failing to hold the recent break above line B – a significant trend line passing through the top formation – and also the failure of the latest rally to recover back into channel KL.

Should the bear now return to Wall Street, a clean break below support at line P is needed to confirm what is as yet no more than early suspicion. As mentioned in the introduction, a DJIA monthly close near 17700 on Wednesday would be a significant event on its monthly long term chart.

Dow Jones Industrial Index, last = 17873 (money.cnn.com)

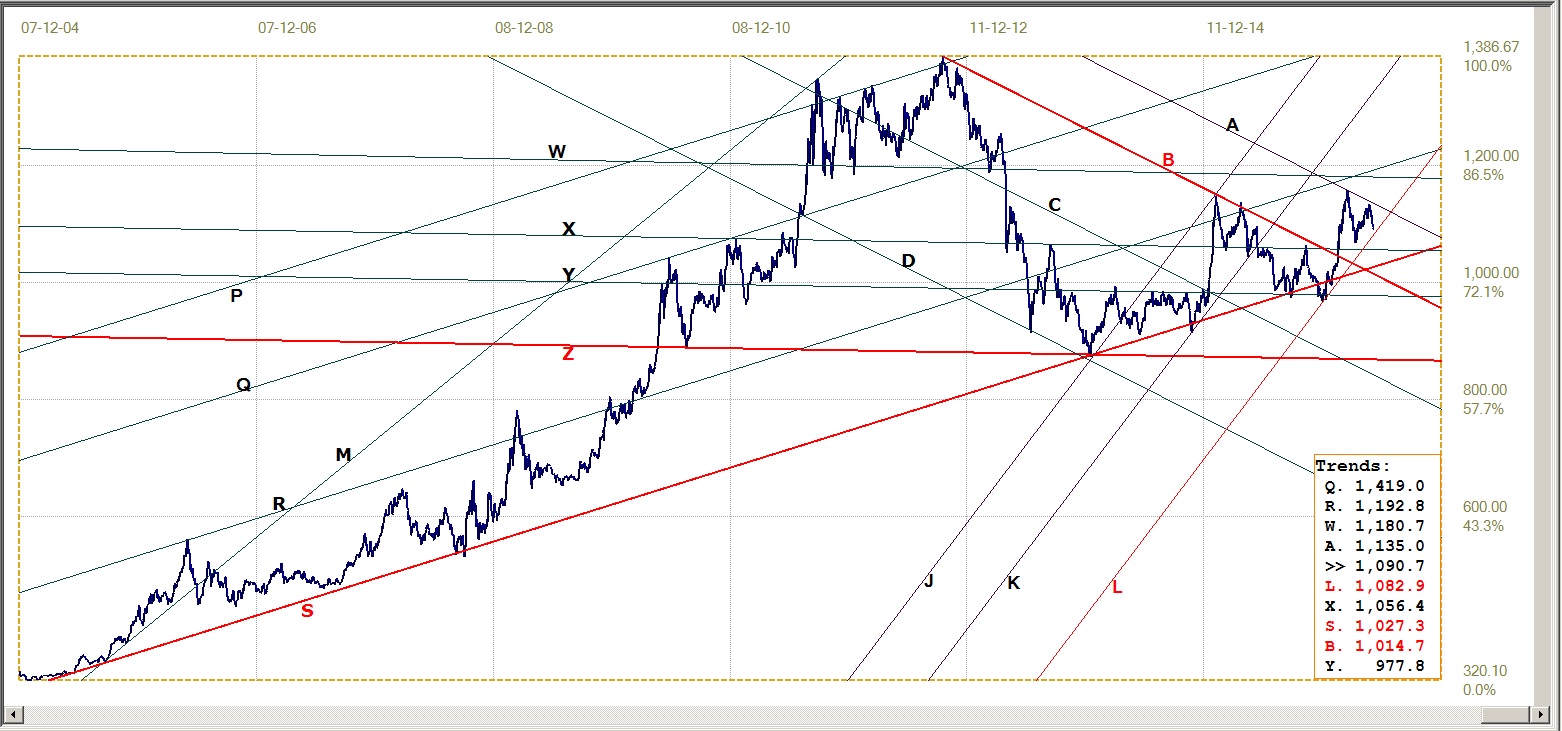

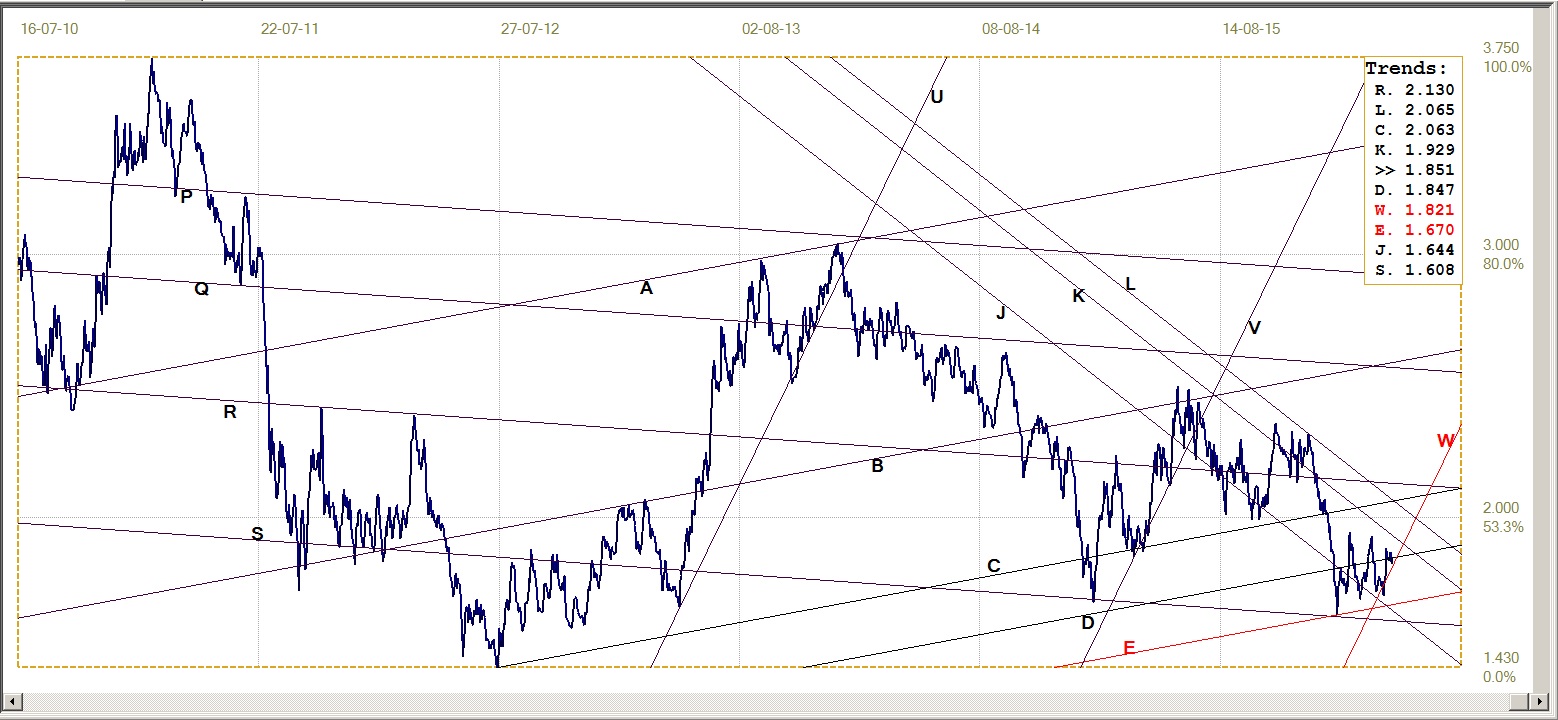

Gold PM fix - Dollars

The past week was even worse for gold than the week before. Psychological support at $1200 was somewhat threatened more than once, but it has held; so far. Steep support from the bull channel shown last week – line V ($1301) – was trashed and a new bull channel KL ($1211) at a shallower gradient had to be generated. Gold is behaving like competitors do in a long distance athletic event; a fast sprint after the start for a good position and then setting a slower pace more suited to the distance.

In the run up to the 2011 high in the price, line J acted as support during the later, steeper part of the rally, before the blow-off into the high. Perhaps this time line L, parallel to line J, might offer long term support for an overall steeper rally than the previous one, from 2008 to 2011. Fundamentals are better than they were in those earlier years. Global debt is much higher and economic growth more of a shadow of what it had been. The risk to the markets as well as risk on the international scene must also prime serious investors to the desirability of seeking the traditional safe havens for their funds in the precious metals.

This week should reveal whether that is a possibility. The markets are precariously poised and any unforeseen event could be a trigger for a new crisis that would send the prices of gold and silver into a steeply higher trend.

Gold price – London PM fix, last = $1216.25 (www.kitco.com)

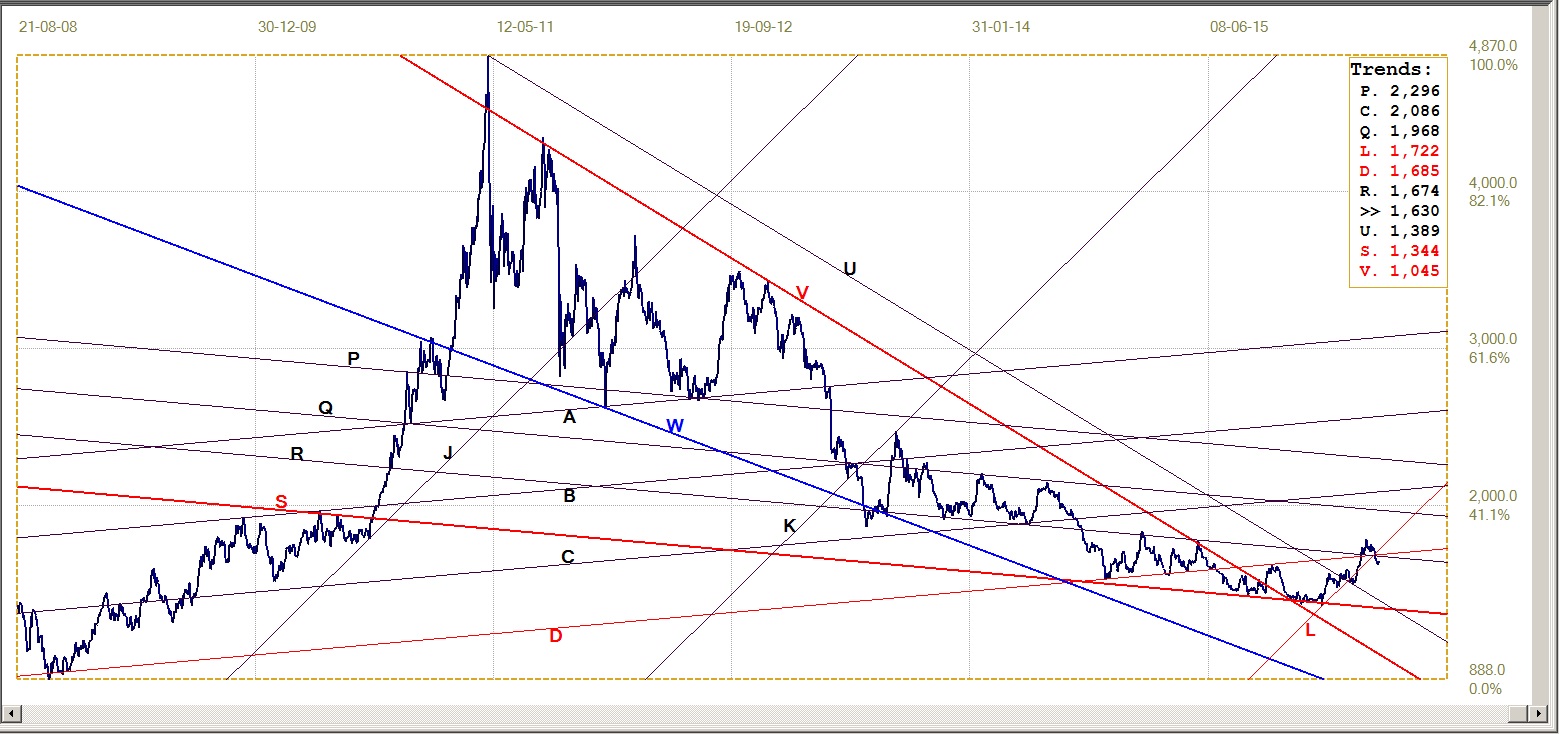

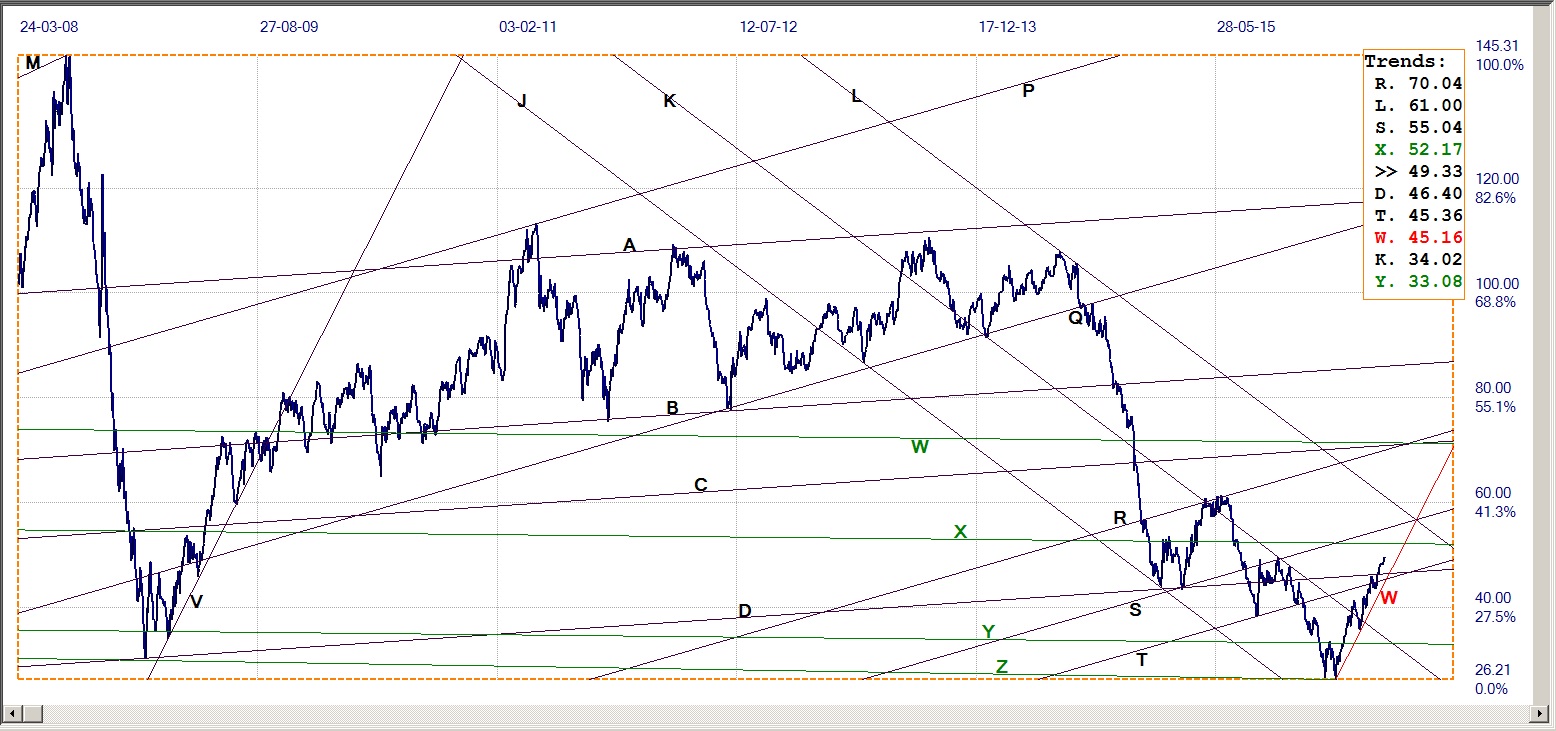

Gold PM Fix - Euro

The euro slipping to a recent low against the US dollar was the saving grace for the euro price of gold. With assistance form the euro, the price managed to remain in the steep bull channel, KL (€1082), even if not by a wide margin.

In remaining with that bull channel, the euro gold price has broken cleanly above triangle BS (€1027) and – as important technically – higher above the broad bear channel, DB (€1015). However, it has now failed twice to achieve success at line A (€1135), the next resistance within the channel set DCBA.

The euro price it seems can no longer rely on a weaker euro to be of assistance to move higher off the support at line L; the dollar price of gold now has to carrY the responsibility to do that despite any handicap a stronger euro can impose.

Euro gold price – PM fix in Euro, last = €1090.7 (www.kitco.com)

Silver Daily Fix Chart

Silver daily fix, last = $16.30 (www.kitco.com)

Silver also failed to hold to its steep bull channel, KL ($17.22). However, the break lower appears less extreme than for dollar gold and the chart is not – yet! – being updated to accommodate a shallower bull channel.

The hit on the silver price has also broken below support from lines D ($16.85) and R ($16.74) to add insult to injury. However, despite this technical weakness, open interest on Comex shows that the silver longs are more determined than those who have gone for gold to hold onto their futures positions – but this could be a result of different delivery months. Because silver seems the more important for people who are short of the metals, gold could remain under pressure this week and later to try and get the longs in silver to wilt as well.

US 10-year Treasury Note

US 10-year Treasury note, last = 1.851% (www.investing.com)

Channel UVW had to be slightly adjusted to keep the yield within the bear channel, also trying to set that channel ratio as close to the Fibonacci ratio of 382:618 – an important ratio in this kind of analysis. The ratio is now 379:621, with still a little room to shift line L to the right. This is nevertheless close enough to the ideal ratio and good enough to keep the yield within the bear channel.

As mentioned in the introduction, this is the third such sustained bear move since the rally earlier this year. Both previous steep rallies carried the yield higher above 1.90% before as sudden a bullish reverse lower corrected again. While bear channel KL can hold, the 1.90% level as well as the psychological 2.0% support is at risk.

West Texas Intermediate crude. Daily close

The new bull trend in WTI crude is still holding well clear of the steep support along line W ($45.16). The true state of the supply demand relationship is murky. Some news from different places about problems with production of crude gets the price moving, but uncertainty about a possible freeze and news of increased production, is not pulling the price back – almost as if good news is very good and bad news also is good enough. There are commentators who believe this sounds very much like a few other markets that are in and out of the alternative spotlights.

WTI crude – Daily close, last = $49.33 (Investing.com)

©2016 daan joubert, Rights Reserved

chartsym (at) gmail(dot)com