A Country Of 2 Minds

share

share

share

share

share

share

share

share

share

share

Cognitive dissonance is the uncomfortable feeling one gets when, for example, one is in a new place and one ‘knows’ instinctively where east and west is, but then the sun the next morning rises in what one ‘knows’ is ‘west.’ It disorientates one and creates a lasting niggling feeling that something is not right. In most cases, when the dissonant situation lasts long enough, the brain automatically adjusts and finds resonance, which it does by accepting the ‘reality’ that is more important for one’s mental well-being at the exclusion of the other. At the moment there are two conditions in the US that promote cognitive dissonance for many Americans.

On Friday, usually a day of high COVID numbers, the new infections were just short of a quarter of a million and the daily deaths were again above 3000. The flurry of commentaries and texts about the pandemic has increased again since the news of successful vaccines – both pro and the few con that slipped past the “fact checkers” – and almost as many people who claim that there is no pandemic, only a scam that is promoted by the NWO to get control of the US and ultimately the world. It is a bit of surprise, though, that some pro-vaccine authors also appear to favour the pro-scam argument, as if this did not present a paradox.

There is a lack of logic – or is it little understanding of maths? – among those that claim the pandemic is a farce because the “great majority” of positive tests happen to be false positives. To illustrate this, assume there are a million positive cases of which 22 350 – approximating the current global ratio – happen to die; a figure that is higher than that for the usual flu by a wide margin. Now assume a ‘great majority’ of 600 000 of the million that did measure positive actually were false positives, then the true CFR, adjusted for only 400 000 real positives is of 5.59%.

In the 1918 pandemic an estimated 500 million people were infected – equal to about 1/3rd of the global population. The 1918 R0, equal to the number of people infected by the same person, was in the similar range – 2 to 4 as that of COVID-19 to make this one equally as infectious as the 1918 pandemic. In 1918 the pandemic was largely spread by returning servicemen of WWI, but surely the ability of the new virus to spread should be greater than in 1918 because we live in a world where there is widespread general travel within countries and also internationally.

Granted, modern medical treatment is much better than in 1918, to greatly reduce the fatality rate compared to that time. In 1918 the death rate peaked at 25 per 1000 people, compared to the current rate in the US of fewer than a 1000 per million of its population, with Italy and Spain a little above 1000/million. However, the 1918 pandemic lasted more than 2 years. If no measures had been instituted to restrict the spread of COVID-19, would there have been a repeat of 1918 to end up with a third of the global population – say 2+ billion being infected, compared to a barely 70 million at the moment, for an increase of more than 30 times? Could the medical system in any country have coped with the number of sick people?

Back to cognitive dissonance. A good example of this condition arises from a clash between the premises on which popular ideologies are based and the evidence of reality as presented by the real world. A common example of this is the stereotypes of people of different nationality or ethnicity to one’s own that are held as valid by nearly all people. Whatever these stereotypes dictate, when we meet and get to know people who do not exhibit the expected stereotypical traits, we are compelled to reconsider. Usually, we retain the stereotype as dominant, but we downplay the cognitive dissonance by mostly subconsciously rationalising our reaction. This we do by accepting that there are exceptions to the stereotype and we happened to have met the proverbial exception that proves the rule.

The stereotype remains intact to simplify our customary world view while we are happy that we can accept and live the exception. That is much easier than having to spend much deep thought in re-evaluating our acceptance of the stereotype in order to modify it to fit closer to a new reality.

In the US, a widely held perception of reality contained a positive view of authority – of government – at least since the revolution, which broke the link with Britain. A strong sentiment of patriotism and trust that the government overall is governing the country for the benefit of all its people. Of course there would always have been dissenters who held a different and opposite view, but they were a minority.

This started to change with the war in Vietnam. The action in Korea may have been a trigger, but the questioning of government did not become nearly as widespread as it did in the 1960s, at least partly influenced by the draft. After the Vietnam war came to a close, with what amounted to victory for North Vietnam, there remained a large contingent who had become suspicious of the motives of government.

During this period, the March for Civil rights also polarised the American people. It so happened that to a great extent, the emotions about the Vietnam war and the civil rights question reinforced each other in the developing split in the ideology of the two contingents. Conservative and liberal became the major difference between the two camps in the minds of many people and this was reflected in the membership of the two main political parties.

As time passed, this split became reflected more and more on a geographical basis, in the generational spectrum and of course on ethnic grounds. The two camps also consolidated their stereotypes of their opposition to the extent that they came near, if not for many actually so, to viewing the other camp as traitors to their view of the American ideal.

The cognitive dissonance that typically exists between people of different countries with respect to mostly unknown foreigners, has come home to be as prevalent in the US as between Americans and Chinese or people in Europe and the people of India, irrespective whether the stereotypes are quite accurate or exaggerated. It is a situation fraught with risk. Close and lasting contact between Americans/Chinese or people in Europe with people in India is rare and presents few problems compared to the US, where for the most part the different and now becoming opposing camps live intermingled and are exposed to each daily. The obvious result is heightened tension, increased frustration at the failure of the other camp to listen to and accept ‘reason’ and therefore increased risk of confrontation escalating into violence.

This is not the place or time to speculate about the next four years and after – and definitely not before the final result of the presidential election and its immediate impact are known. From recent history, one can hazard the guess that if Trump is to move into the White House for a new term, the destabilisation of the recent past will resume and probably increase. On the other hand, if Biden is to be the new president, the conservative camp might consider beginning a similar campaign of civil disorder that was experienced during the past four years.

Given the increasing width of the divide between those Americans on the left of the political spectrum and those to the right, it is not easy to think of what steps could be taken to bring the two camps closer together. Anecdotal evidence to be found on YouTube about the vehemence of the anti-Trump sentiment among young liberals in particular illustrates that that it will be difficult to reduce the differences.

It is, however, clear that any efforts to do so will have little positive results unless the media – including in particular the social media – fully partake in such efforts. The chances for this to happen appear to be very slim, at least for the foreseeable future. Instead, the opposite appears much more likely. This is not a good position for the US to be in; worse than after the Vietnam war. The historical remedy for a wide split of opinion in a country is to begin a nationalist war to invoke patriotism across all divisions of public opinion and even loyalty. Hopefully it is not a remedy that will be sought soon.

The aftermath of the price collapse of gold and silver during the past four months and culminating on 30 November should last for much or all of December to keep buyers wondering whether to commit the full purchase amount to obtain a foot in the December contracts. Most would probably shift their attention to later months. So let us set our sight on 2021!

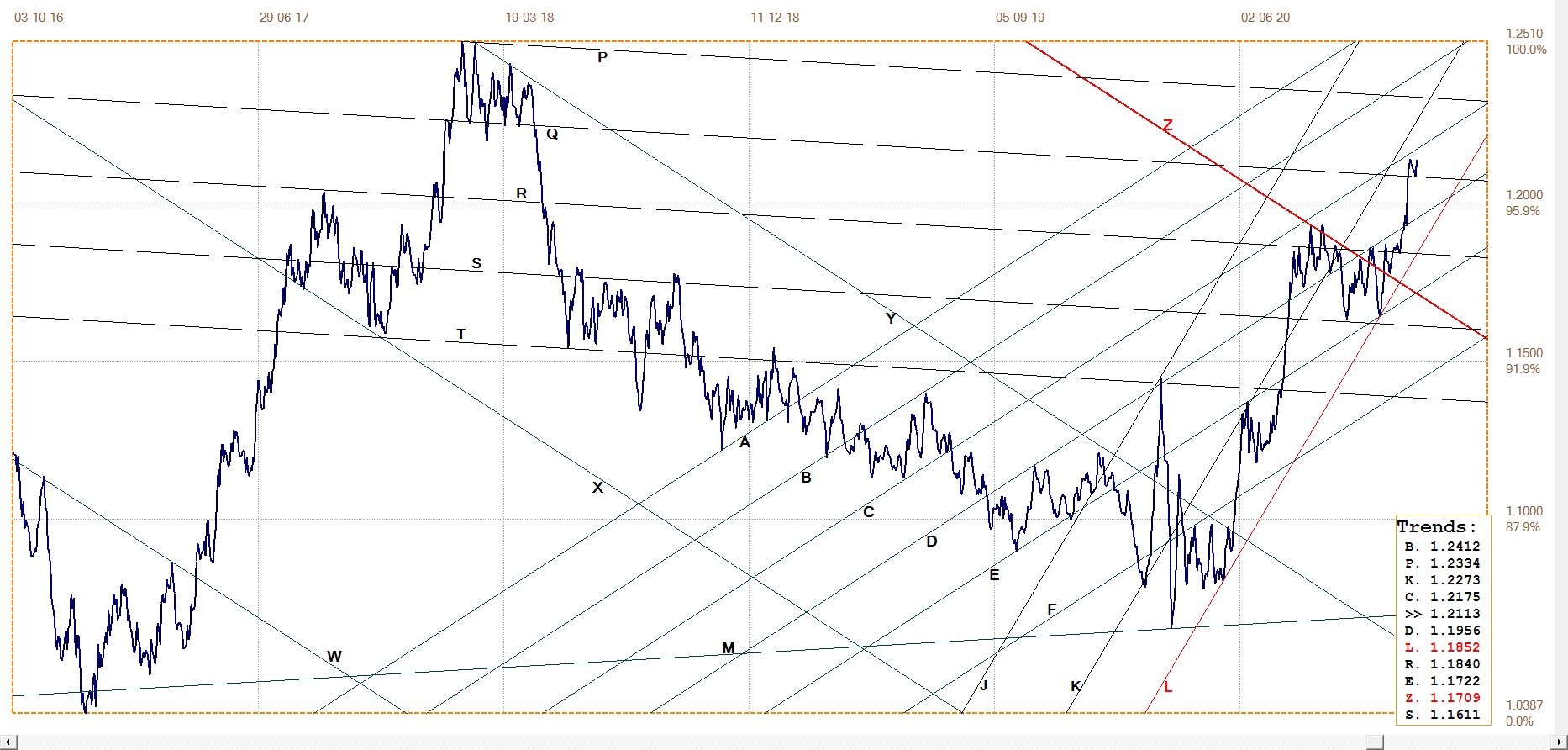

Euro–Dollar

The euro is keeping well within bull channel JKL and has broken above line Q, then returned to the trend line and bounced again. This kind of event is called a goodbye kiss and usually signals a resumption of the initial trend. Another and usually less frequent possibility is that the price reverses direction again and breaks below line Q, to leave a bifurcated top above the trend line to act as a top reversal pattern.

Whichever it is to be, we should know within a few days whether the euro bull trend is intact or whether a top has formed. The odds favour a stronger euro; therefore a weaker dollar, which should be positive for the precious metals – perhaps later.

Euro–dollar, last = $1.2113 (www.investing.com)

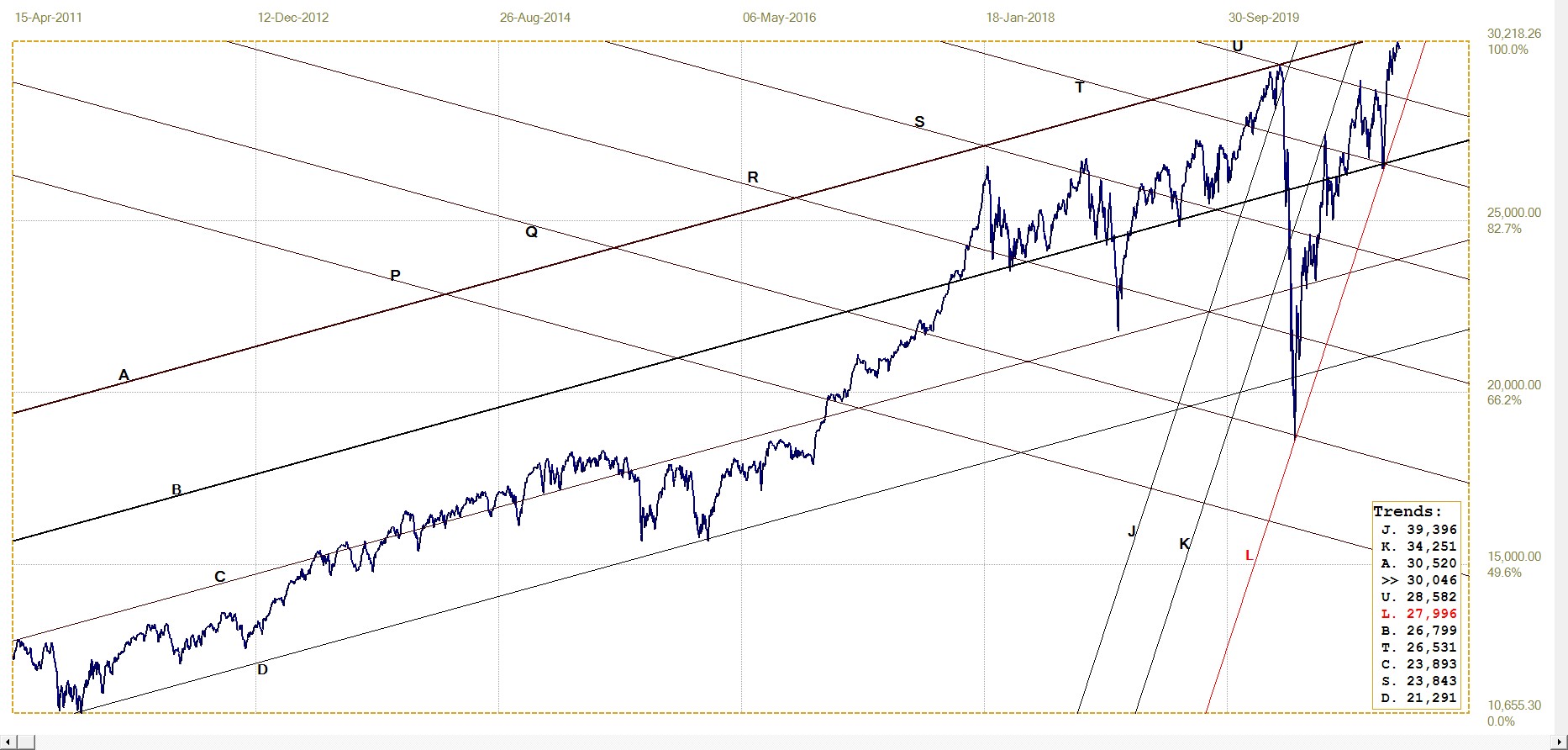

DJIA Daily close

DJIA, last = 30218.26 (money.cnn.com)

The DJIA achieved a new all-time high at the end of November, but since then has kept quite close to the new top to set December off on a firm footing. There have been days of early weakness, but the support soon manifested on those days to either limit the loss or to achieve relatively small gains.

Triple Witch is coming up this week and then the market moves on to year-end; in both cases important dates for investors and speculators, including fund managers who will be jockeying to achieve the best performance ratings they can engineer. An interesting time ahead, but not for making medium to longer term decisions – these have to wait for 2021.

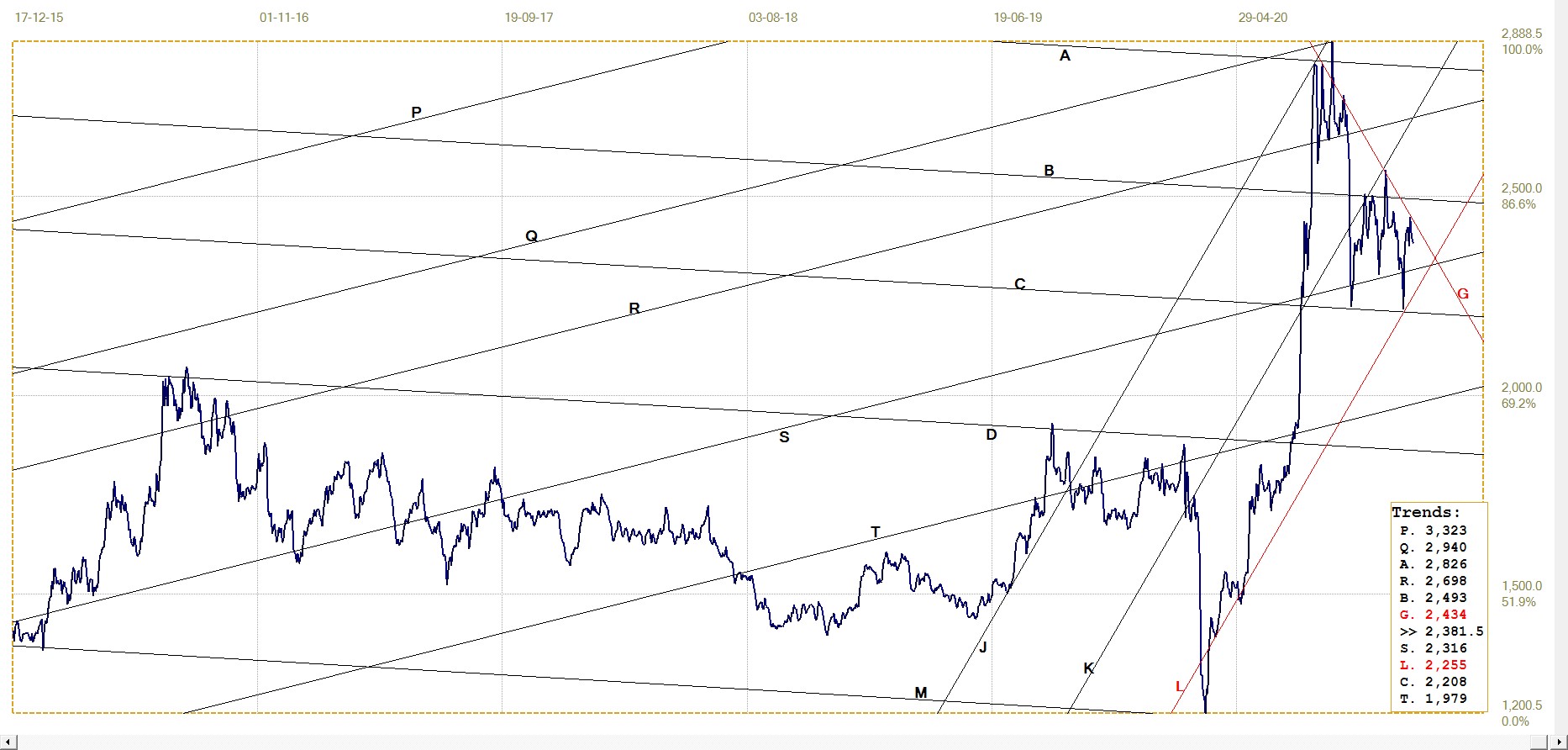

Gold London PM fix – Dollars

Now that the expiration of the December options is past and December has become the active month, the biggest threats to the Big Banks are past, to leave them with wide smiles and counting the premiums they could pocket after the four month long attack on the gold price.

The price rebounded quite rapidly off the November 30 low, probably to leave any keen buyers with deep pockets little opportunity to get into the market at low prices to make a profit by month end probable and a good bet. If they desired delivery. All other interested buyers had to switch positions to a later month, be it in options or in futures. The increase from 20 November to 4 December in the number of Feb21 gold contracts is fewer than 400 contracts, so the scramble to later dates has not yet commenced. By last Friday about another 5000 contracts had been bought, still at a good price to what gold had achieved earlier. These purchases place renewed pressure on the Banks to let the silver price rise further before too many new cheap contracts are sold to become a liability when the metal resumes its bull market.

Gold price – London PM fix, last = $1842.00 (www.kitco.com)

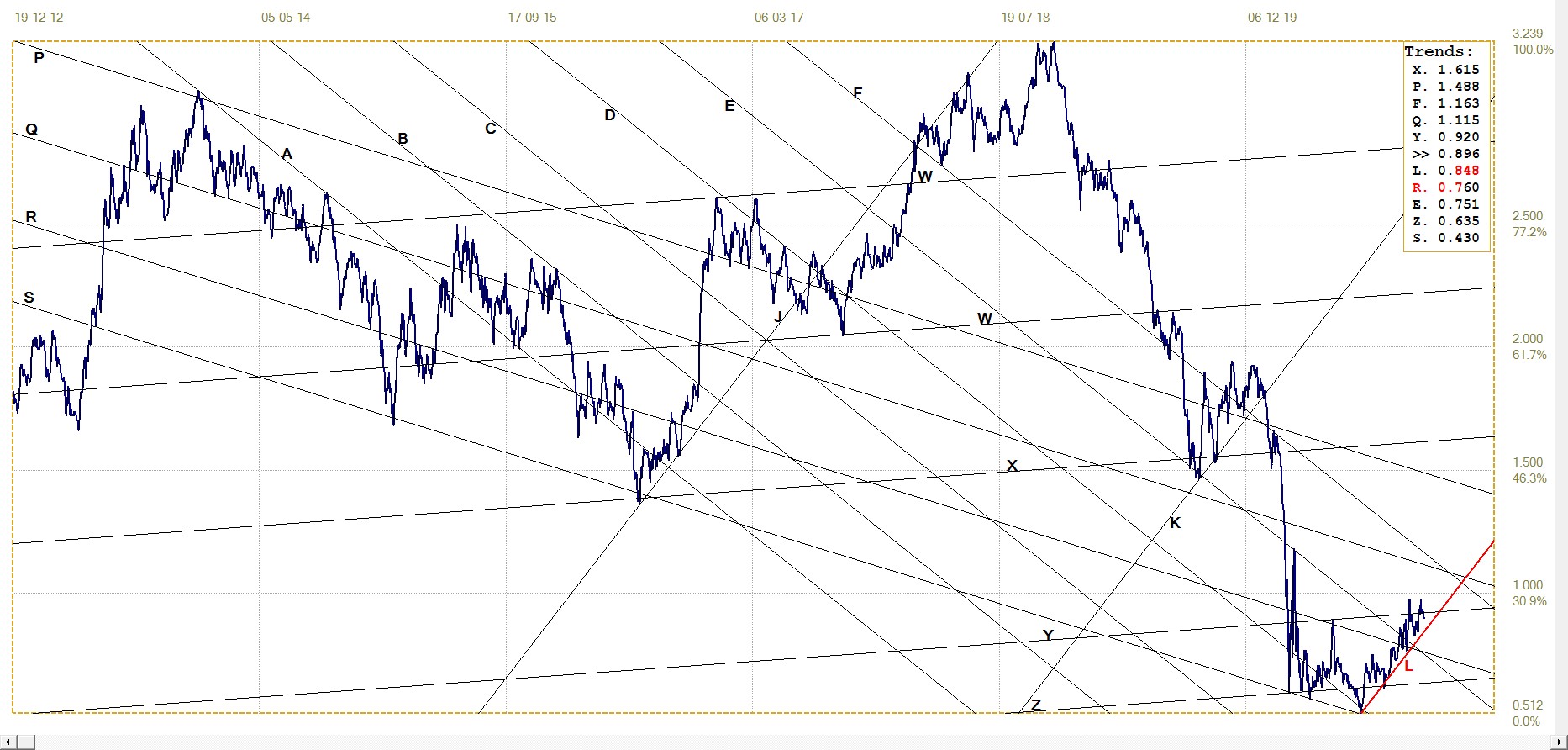

Euro–gold PM fix

The break below the megaphone JF has recovered to re-activate higher volatility associated with that kind of chart formation. Whether an increase in volatility is to be from the euro-dollar rate or from the dollar price of gold or a combination of the two factors remains to be seen; if that should happen.

Perhaps the euro price first has to hold within the megaphone, then work its way to above the resistance along lines Y, B and G before the volatility can commence. It would not surprise if this too has to wait for 2021 to bring new excitement to the market.

Euro gold price – PM fix in Euro. Last = €1519.7 (www.kitco.com)

Silver Daily London Fix

Silver daily London fix, last = $23.815 (www.kitco.com)

Silver also rebounded after the low of 30 November did so for and probably the same reasons as discussed for the gold price. The March OI for silver contracts were 124 210 on 30 November and have now increased by more than 7 thousand to 131 564 as per the preliminary report for 11 December.

This is a hefty jump and should motivate the Banks to let the price rise faster. That is, unless there are major OTC contracts waiting for them at year end, a little more than two weeks from now. Of course the same applies to any exposure the Banks have to gold contracts in the OTC market – which are likely to be for large volumes. There are intricate times ahead for buyers to consider before they decide to take on new positions in silver and gold.

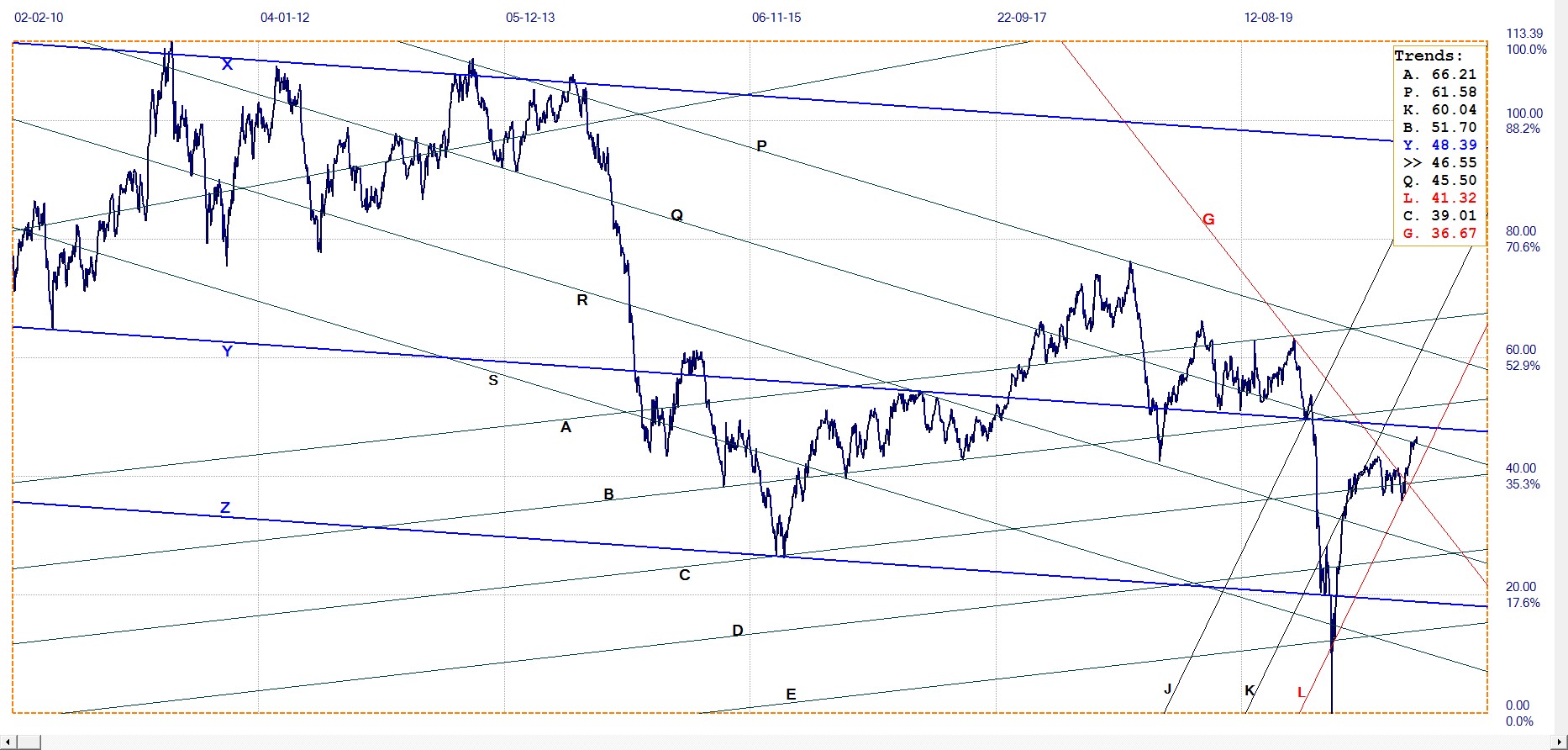

U.S. 10–year Treasury Note

U.S. 10–year Treasury note, last = 0.896% (www.investing.com )

The yield on the US 19-year Treasury note is clearly in an uptrend as long as it remains above line L. Yet it cannot make up its mind whether to be above line Y at 0.920% or below it – but above line L at 0.848.

Perhaps the market is hesitant to even challenge, let alone breach, the 1% level on the US 10-year note, for the psychological impact this might have on investors – or perhaps that could be the opinion of the Fed et al who prefer the yield to remain a little below the 1% level in case a break higher spooks the market.

West Texas Intermediate crude. Daily close

The past week has seen little change in the price of crude. It is still hovering around line Q and could increase to test resistance at line Y before it could extend higher in bull channel JKL. This market, too, could be waiting for a resolution of the election dilemma before seeking out new ground.

********

share

share

share

share

share