Long-Term View Of Gold And Silver

So the end of April came and is now gone and we have entered the merrie month of May, with good memories of what had happened at this time last year. The question whether the short squeeze of silver is coming in to play is still open, but there should be a few indications quite soon on whether this is imminent or would require a longer time to build up. If, of course, such a squeeze on the metal could materialise at all, as seems doubtful to some commentators.

Increasing expectations expressed in the media of substantially higher official inflation are providing a boost to safe havens, among which precious metals feature prominently. With the crypto currencies also on a roll, it might be that they too have acquired safe haven status – that is, unless their good price performance is merely a modern digital form of tulip-mania. The current administration’s intentions of massive spending, partially funded by tax increases on the wealthy, to get the economy going and improving infra-structure, are likely to boost Federal debt above the $30 trillion level. Much of this spending is intended to filter down to worker households in the hope that there will be a strong showing of support at the voting booths.

There are commentators who expect to see greater than $2 trillion deficits for the next few years, at least. The Fed has undertaken to keep interest rates low for the foreseeable future, but can that commitment hold should inflation creep much higher than the ‘ideal’ 3%? Can any inflation be a ‘good thing’ from the perspective of people who are retired and have to live off their savings and their shrinking Social Security? Retired Americans are forming a growing proportion of the population and with better health care are living longer than previous generations. A self-made problem for the government that will develop in the near to medium term future?

May is not a gold month and only 450 May futures contracts (45 000 ozz or 1.5 tons) are standing for delivery. The number of silver May contracts also decreased rapidly from a high number, leaving just short of 1800 contracts waiting for delivery. That is about 9 million ounces, which is not a negligible number, but not as much as silver bulls had hoped for. It is nevertheless interesting that there was no all-out attack on the metal prices as April ran out last week.

Even so, the net short position of the Commercials is trending lower again, while the Large Specs are going more net long again. It looks as if rather than an attack, the Big Banks were content to conduct a delaying action, working away to keep the price of silver from rising too fast. Perhaps there is a sense of nervousness, if no longer an outright panic, among the shorts; they do not want to tempt fate by giving the gold and silver bulls an opportunity to go long(er) at much lower prices. This hesitancy is a good sign for what the month of May could bring.

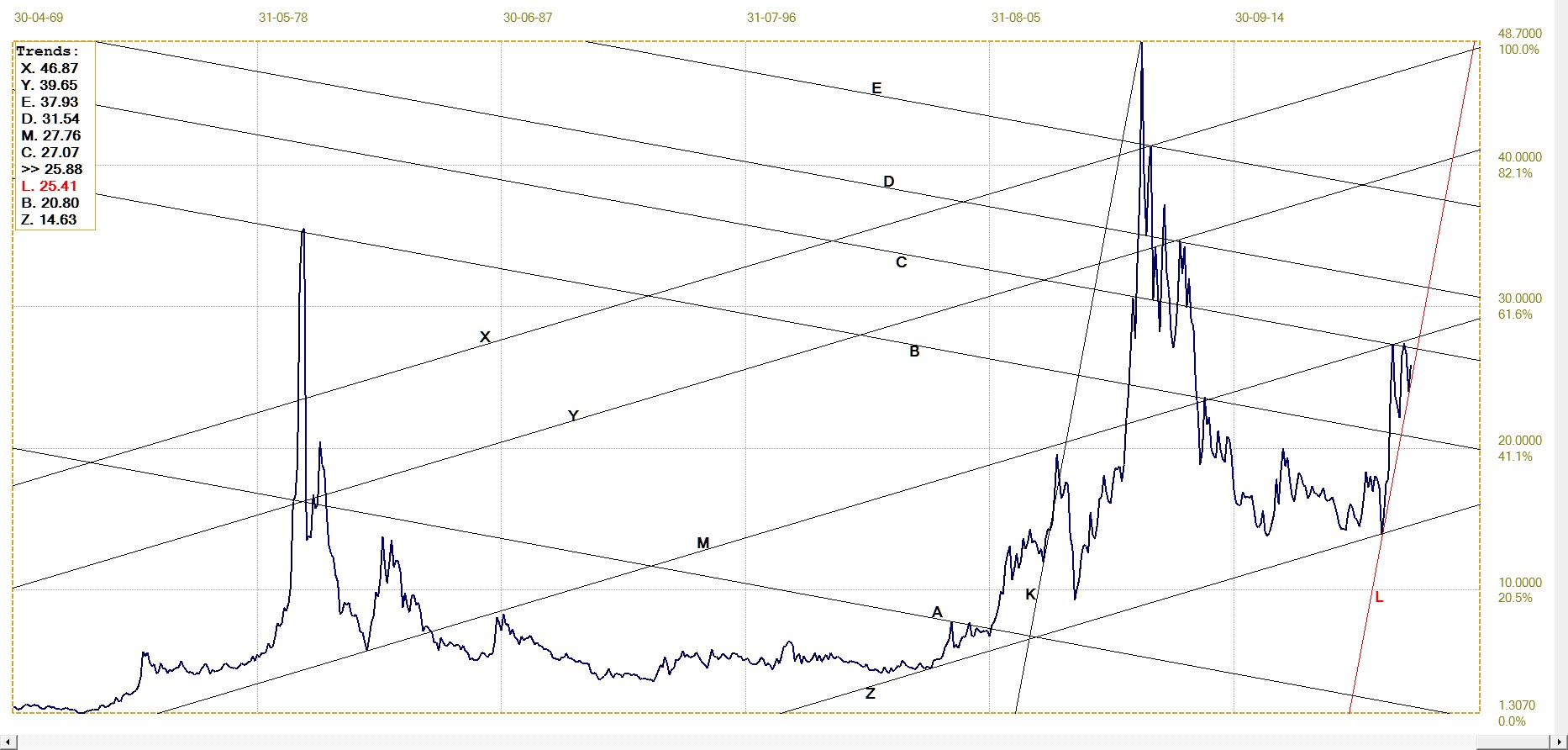

The two charts below are the monthly closing London fixes of silver and gold, showing their full history since the late 1960s.

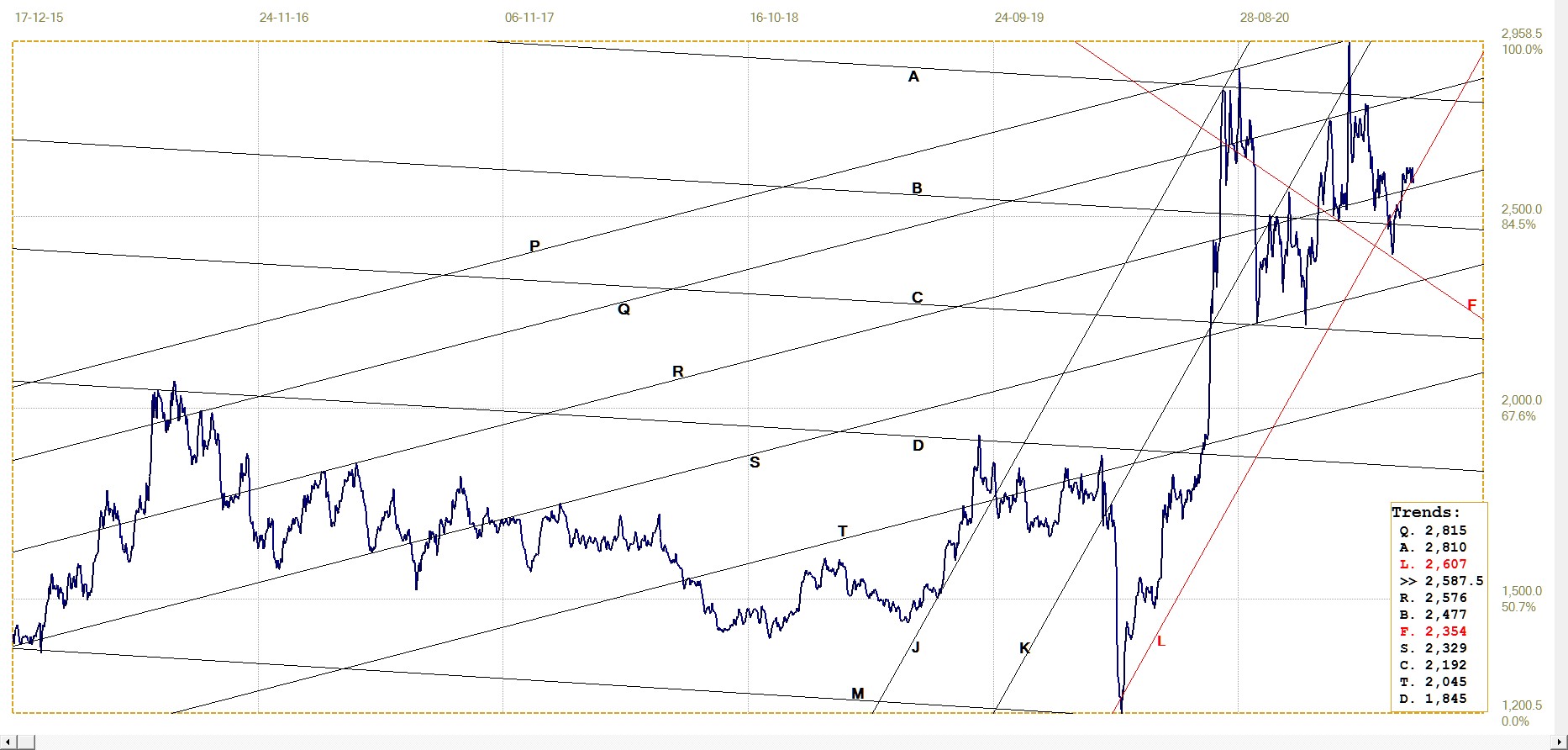

London Silver fix. Monthly close. Last = $25.875

The above analysis shows that the silver rally of May-July last year ran into resistance of lines M and C in August; it then completed a double top in January this year, when the price again failed to break higher. A new rally has just started, barely in time to keep the price within the steep channel KL. Should there be a repeat of the May rally of last year, this time off a higher base, the odds favour a break above lines M and C, hopefully to remain in the steep bull channel.

Compared to the chart below of the price of gold, which shows a new high well above the 2011 top, the silver price has hardly moved off from its low at line X, which is only a little above the extended sideways drift from 1987 to 2002. It still has a long way to go before setting a new all time high. Much will depend on the next few months, if the price of silver can hold in the steep channel.

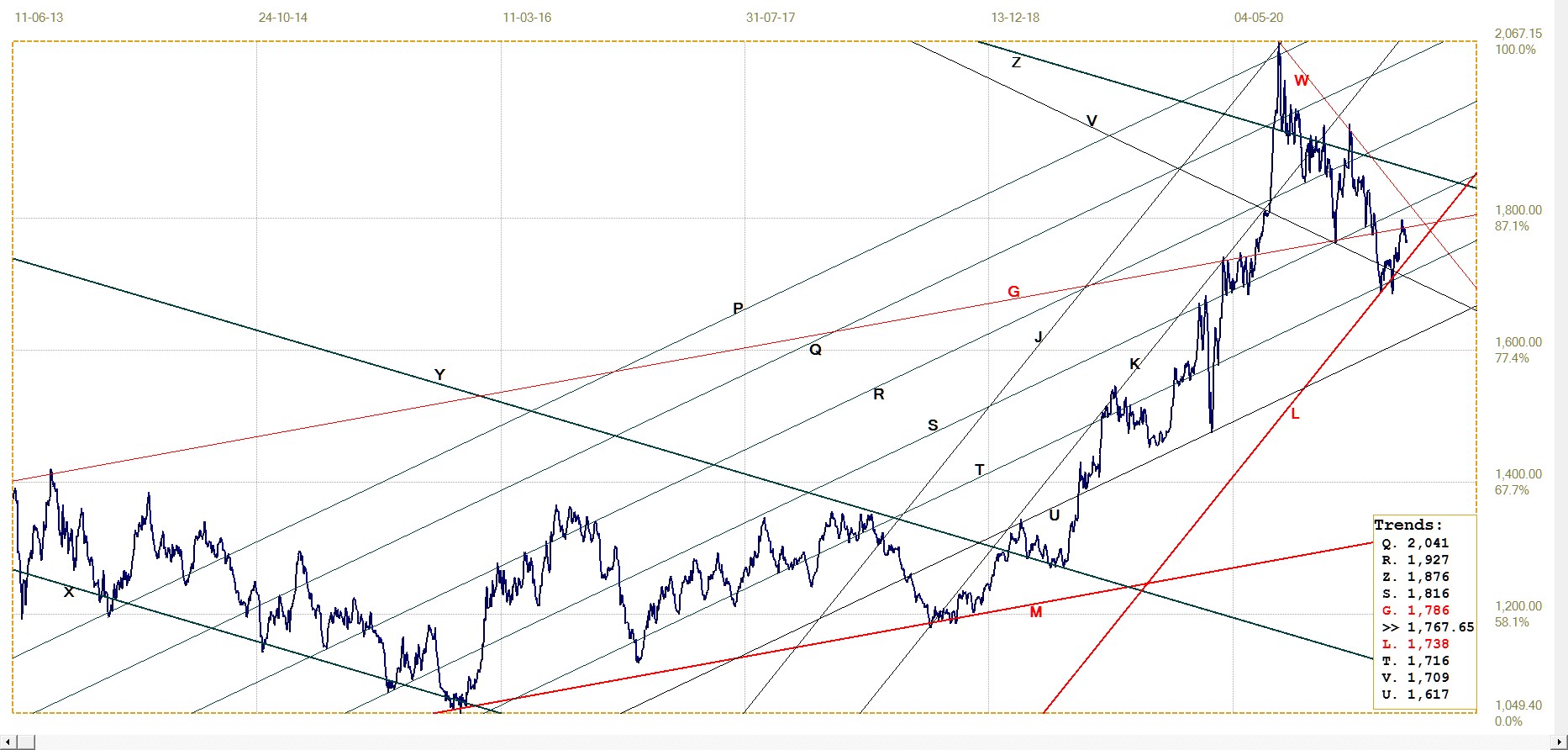

The post August 2020 attacks on the price of gold brought the price down to support at lines B and Y, just in time to hold to the steep channel KL. As for the similar steep channel on the silver chart, these trend lines were not fitted to the chart, but had their gradients derived from the respective master gradients, M, on the two charts. The fit of the steep channels therefore is an integral feature of the price behaviour.

As for silver, the gold chart also holds promise that there would be a rally due to begin during May. The technical evidence of good support for gold that has held so far as well as the two steep channels, hold promise that we could have a repeat of the good performance of last year. Given the changing circumstances if the precious metals market, including the popularisation of a silver short squeeze by the REDDIT Apes, the fundamentals concur.

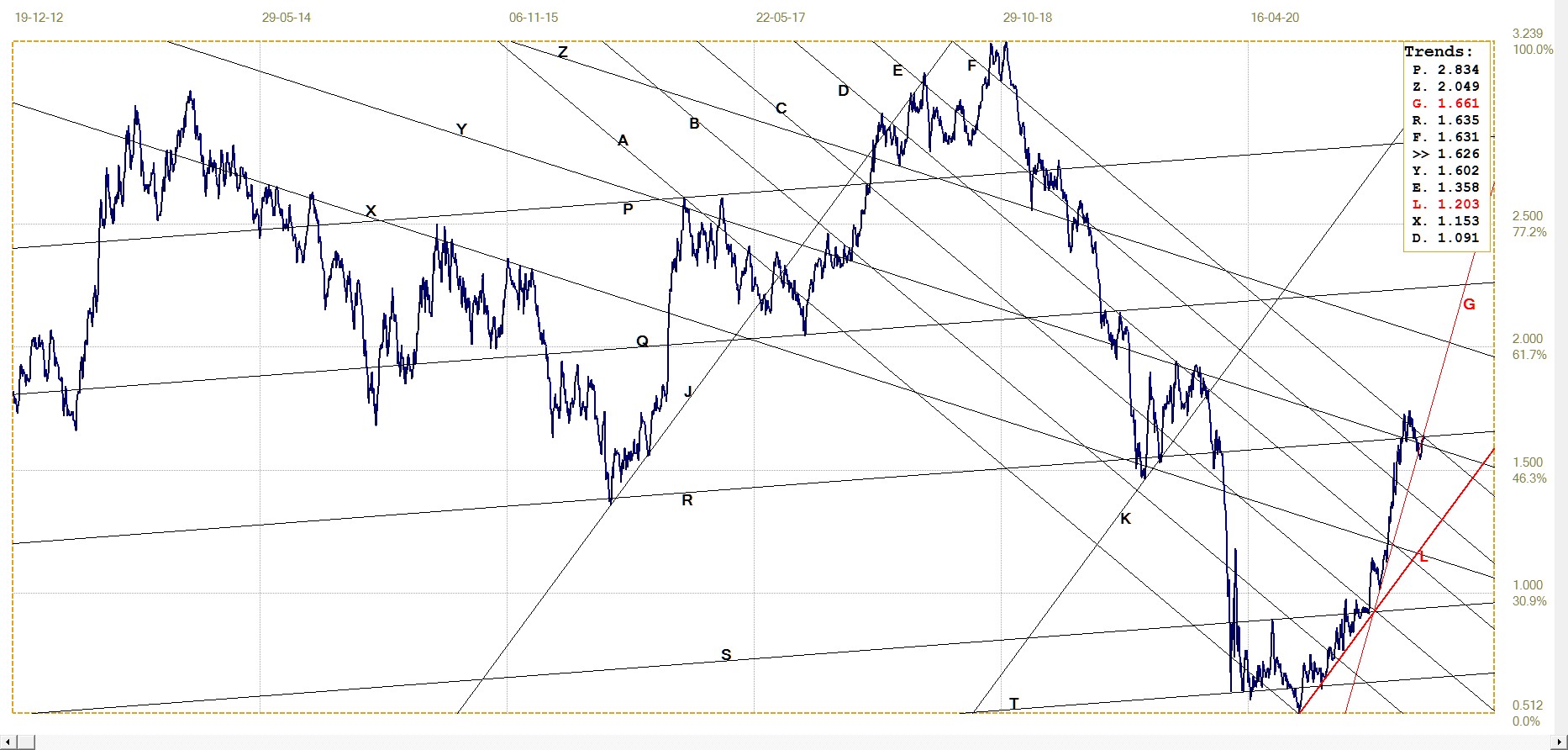

London Gold PM fix. Monthly close. Last = $1767.65

The Big Banks have nevertheless shown in the past that they can pull a suppression rabbit out of the hat when desperately needed.

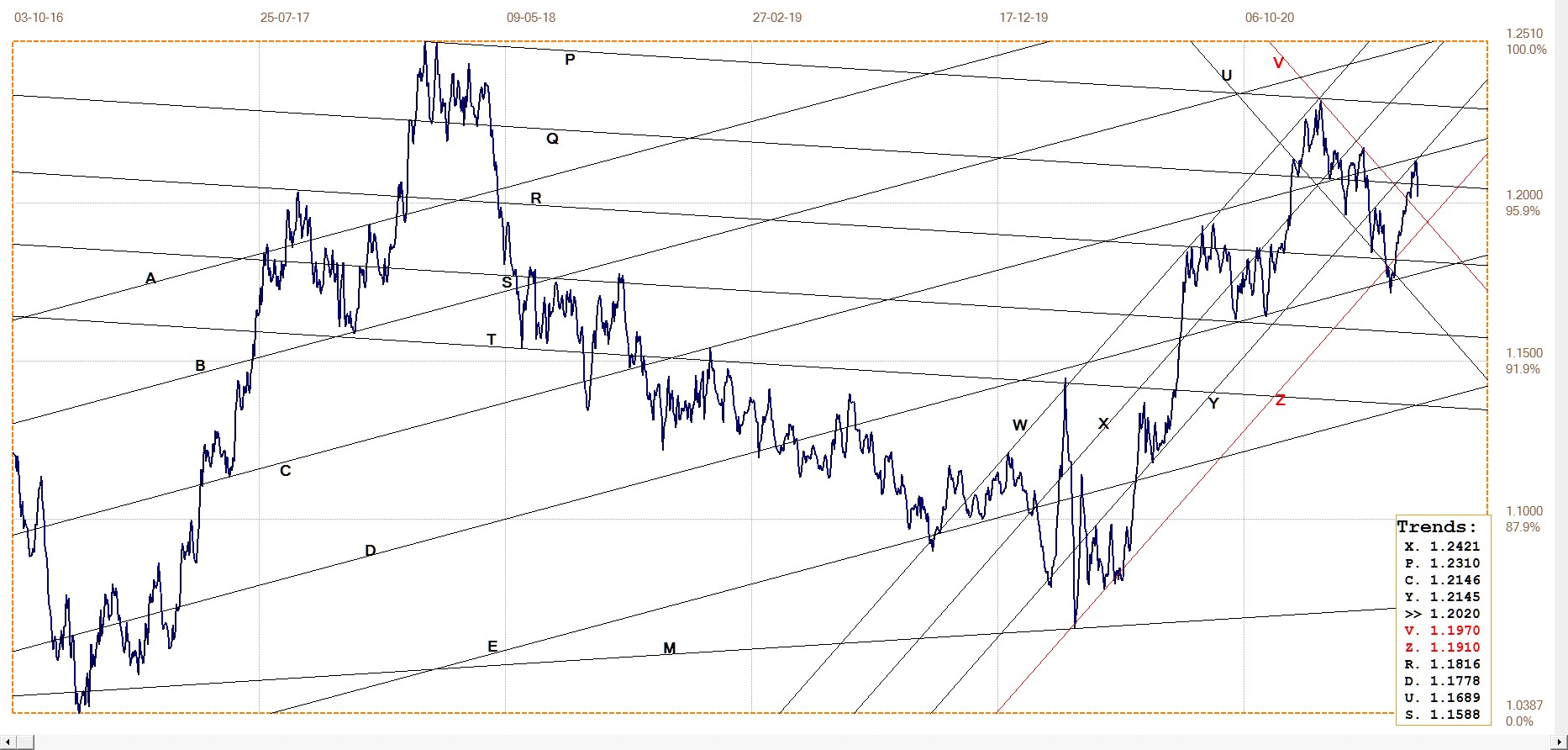

Euro–Dollar

The recovery in the value of the euro hit resistance at line C and then reversed back to below line Q to hold in channel YZ after failing to break higher. The outlook remains bullish as long as channel YZ can hold, which implies that there is ample time for the euro to consolidate sideways before there can be a break below the bull channel.

Euro–dollar, last = $1.2020 (www.investing.com)

DJIA daily close

DJIA. last = 33874.85 (money.cnn.com)

The DJIA is still holding to its period of consolidation near the all time high of the DJIA – oscillating between small daily gains and similar losses, without identifying a specific direction. While intuitively the new direction should be bearish, given a very high PE for the S&P500, one should keep in mind that with the government spending hand over fist, putting trillions of dollars into the economy, a good deal of this ‘helicopter’ money could find its way to Wall Street, to extend the long term bull market.

Gold London PM fix – Dollars

Gold price – London PM fix, last = $1767.65 (www.kitco.com)

The reversal off the recent low, to return to bull channel KL and also the pennant VW, failed to hold the break above line G. This failure was not unexpected at the time it happened – gold never performs well near the end of a month when Comex options expire and futures have to stand for delivery.

Now that the end of April is behind us and with last year’s May rally still fresh in our memories, we look ahead to a resumption of the new rally once the labour number on Friday has been announced. This resonates with the monthly long term chart where the price of gold has also reversed off firm support.

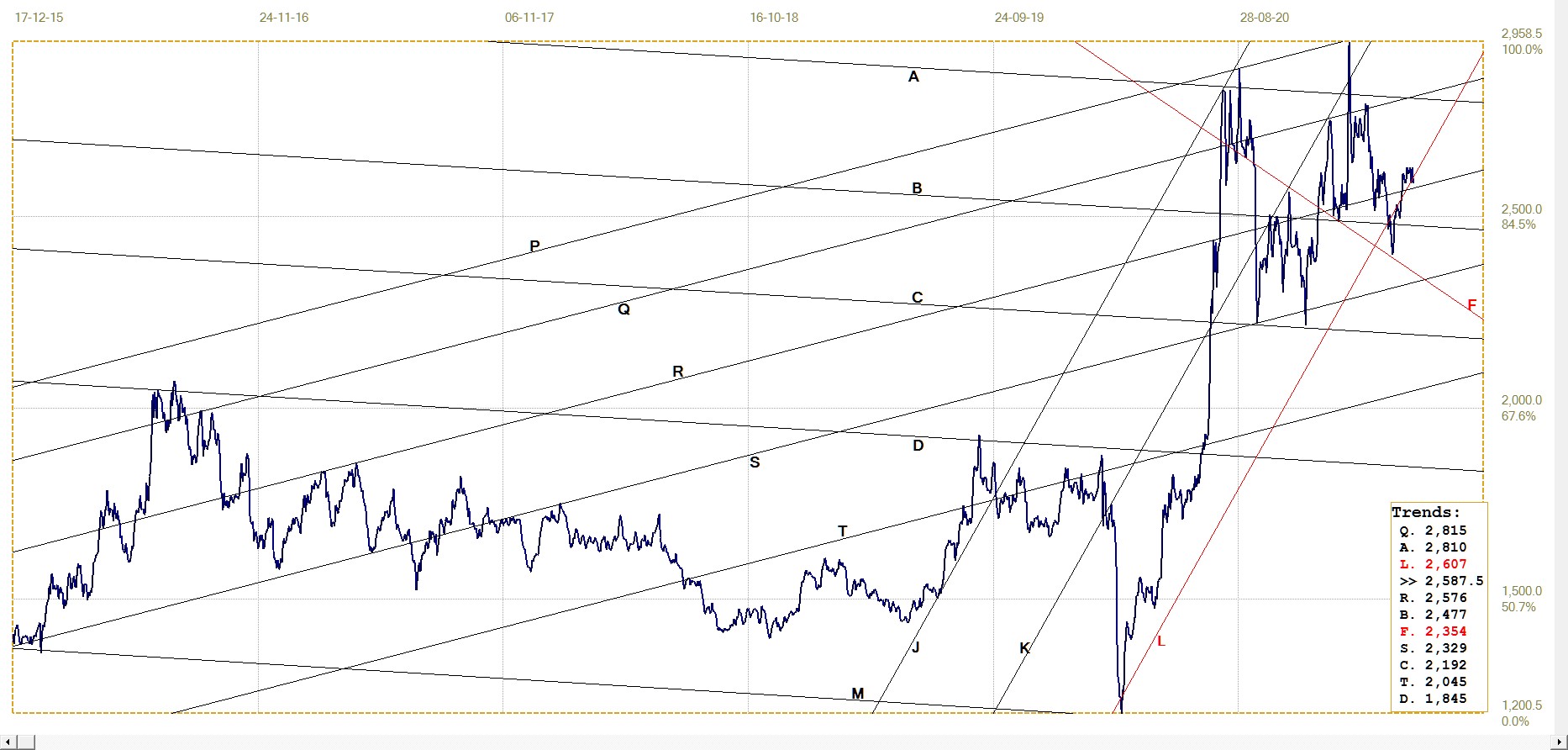

Euro–gold PM fix

The euro price of gold is also holding in its steep bull channel, KL, and above line R. The recent combination of an improving gold price and stronger euro meant that the euro price has become static and is consolidating barely within channel KL. Now, with the euro likely to firm further, the price of gold has to perform to keep the euro price within channel KL.

Euro gold price – PM fix in Euro. Last = €1463.97 (www.kitco.com)

Silver Daily London Fix

Silver daily London fix, last = $25.875 (www.kitco.com)

The silver chart is another example of the price barely holding to a steep bull channel, or in this case, just failing by a small margin to hold within the bull channel. Seeing that this has happened more than once recently, each time with a recovery back into the channel quite soon, one can expect – or hope! – that this now will happen again.

Here, too, stage of the Comex market favours a recovery at the beginning of a new month, with only the non-farm payroll number ahead on Friday this week to hamper a recovery for silver. Much will now also depend on how the attempted short squeeze is progressing, as perceived by the market and the Big Banks. If the sweeping of metal silver out of the retail market is having an effect on the availability of the metal and the number of contracts standing for delivery is depleting the Comex vaults, it is near certain that the price will react higher.

U.S. 10–year Treasury Note

U.S. 10–year Treasury note, last = 1.626% (www.investing.com )

There has again been little change in the market for the 10-year Treasury note during the past week. The yield has settled near the confluence of bull channels EF and XYs, bear channel RS and the steep line G. It is as if the yield is loath to break above the broad bull channel AF and not looking forward to the inflation driven break higher.

A break below line G will not cancel the bearish bias – that would require a break to below bear channel KL, which is not at risk for some time. A definite break higher will offer confirmation that the talk of higher inflation is a reflection of what is now actually happening, not only based on the amount of money flowing into the financial system.

West Texas Intermediate crude. Daily close

WTI crude – Daily close, last = $63.4814 (www.investing.com )

With the price of crude still solidly in place within steep bull channel KL, the failure to hold the second break above line C shows that the rising trend is still consolidating. If the market reacts as could be expected from all the talk of higher inflation, one can assume that channel KL will hold and there will be a definite break above line C soon.

©2021 daan joubert.

********